Obliterate or Communicate

Another morning, another attempt at panning for truth. Yesterday, the US President promised to obliterate Iran’s power stations and desalination plants if Tehran did not shortly agree to the terms of ceasefire proposed in its fifteen-point plan. Such bullishness kept prices propped most of yesterday, but an overnight article in the Wall Street Journal indicates that privately, Donald Trump might just be a little more pliant. It reported White House aides having said that he is willing to end the U.S. military campaign against Iran even if the Strait of Hormuz remains largely closed, but if Iran then refused to open the Strait, operations would resume and this time he hoped European would be persuaded to join in any force that kept the corridor open. However, with the Kuwait Petroleum Corporation tanker Al Salmi hit by missiles or drones while at port in Dubai, the question remains on how willing Iran is ready to back away from conflict or even allow shipping to resume and give away its superpower of holding the world’s economy to ransom. There does seem to be a trigger for Trump appeasement, and it normally involves price. Reuters joins us in tracking GasBuddy, the US real-time website and tracker of US domestic fuels, which reports on how the average US forecourt Gasoline price has risen to levels not seen since the outset of the Ukraine war, a round number of $4/gallon. This is a vote loser in the United States, and while polls should never be relied on, gas pump prices most definitely can. Talking on equities, bonds, inflation and the like are akin to considering the symptoms, the core cause of every market move is the oil price and what headline is the most recent. We will all have to keep on panning until there is a nugget of truth large enough not to disappear through the sieve.

Changeable prospects

Yesterday my learned colleague mentioned ‘prospect theory’ and it really can sum up some of the situations we are witnessing in this sleep-thief of a Middle East situation. In trading markets there is evaluation between losses and gains with negative outcomes building exponentially more fear, odd positional decisions, leading to greater loss aversion. An example might be how holding on to an equity position for too long need then be financed by having to sell commodity length or some equivalent. The current upward spiral in oil prices is about to cause many more instances of odd market behaviour, but it will be broader than just those who might be deemed professionals in risk taking. Consequences abound and will be reflected and widened to nation states as they try to juggle economic exposure.

In the UK, groups of friends will joke, with a sigh of inevitability, on how Diesel will soon be £2/litre, a morning coffee £5/cup and when trying to shake all the gloom off, the pub will see beer being served at £10/pint in central London. These were all pre-Iran war, the prospect of them all happening has gone from a maddening swipe of ridiculousness to one of close reality. This then is when the switch from oil concentration will slowly wander into the retail costs of the everyday and a future studded with inflation. It does not matter whether Brazil or other growers have experienced a frost, the cost of shipping has soared not only with the influence of events inspired by Hormuz but had started from a lofty position as tariff costs had already seen speculative length entering Coffee futures as result of the 40 percent tariff the US had landed Brazil with.

Switching modes of commodity and continent, the soaring price of oil and the flight to the USD has seen the last two years of lust for Gold suddenly undergo scrutiny. The Central Bank of Turkey is in full defensive mode as it faces the prospect of its oil importer status being so much more expensive to finance. Exacerbation comes from the US Dollar being once again designated as the favoured flight instrument for the world’s investment tourism. It was only two weeks ago that the CBT kept rates unchanged and as such tried to walk the awkward path of keeping domestic monies in Lira assets while battling inflation at eyewatering levels of over 30 percent per annum. This decision now looks regretful, the USD/TRY has fallen by over 1% to all-time lows in the last month and as this note suggests, something needs to finance an out-of-date stance. This is why Turkey has sold 60 tons of Gold to support its currency and by doing so has inspired selling from others in what has, up and until now, been a money printing cycle of a rallying Gold price.

This current turn in the millennia of Middle East heartache has now entered a new phase. The damage is irreparable, and it is not just the usual relationship between oil, energy and other assets. It is now accepted from the peoples of the world that oil prices cannot be trusted. If we accept ‘prospect theory’ will hamper the decisions of banks, trade houses and indeed governments; then retail customers, the ultimate arbiter of demand, may well suddenly develop differing forms of economic behaviours, particularly to energy. Those that have been at the forefront of battery technology must be doing a silent dance, and those at automakers and oil companies who have elongated net zero targets (a pseudonym for energy transition), to farther in the future, might now be convening rethink meetings. It is of course all too early, and additionally subject to how long this current soul-draining war lasts to turn a misty crystal ball into insight. However, our market is forever changed and if any of us have been arrogant enough to believe that we have been on the road to understanding oil communication, we are, along with current politicians, lying to ourselves.

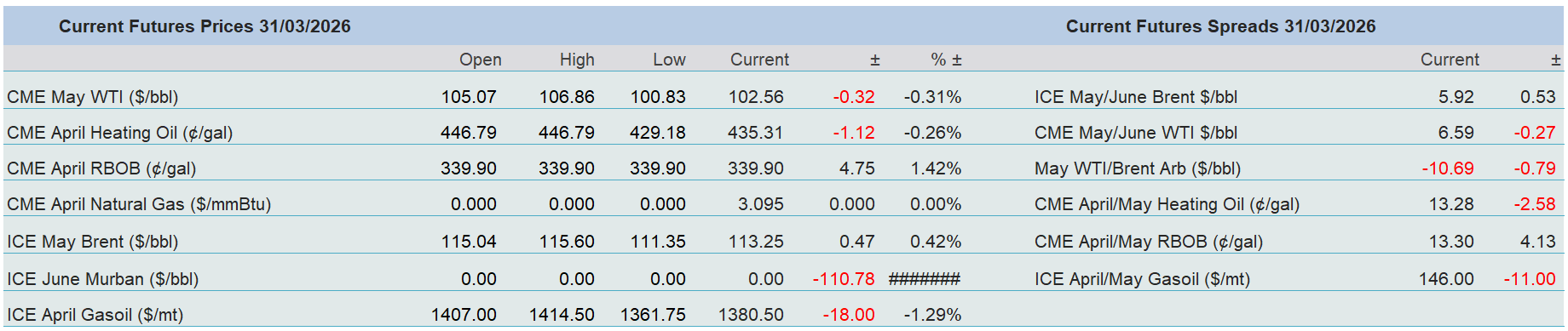

Overnight Pricing

31 Mar 2026