Oil continues to shrug off macro-dampeners

Trying to run a carefree bullish or bearish attitude in oil is the stuff of halcyon dreams. Much of yesterday’s performance had the feel of a corrective process with Heating Oil and Gasoil testing down to some very important technical levels. The trouble being for those of an oil-persuasion, and a sign of the times, is working out if the move was a reaction to a market that was arguably a little frothy in terms of late-comer length or that it was the general malaise set in around the world’s investment suites. The ridiculous shenanigans taking place in Washington, where a group of hard-line Republicans in the House of Representatives are voting against the party’s wishes, forcing the government into a shutdown brings back memories of the recent debt ceiling tangle and the US downgrade. Late last night the Senate tried to step in with legislative procedures to halt what the House was attempting, but it seems too little, too late and only served to highlight the rift between the two governing bodies. There have been 14 shutdowns in recent history and although they tend to last only a few days, the damage to confidence is adding to global economic woe. This is highlighted by the rating agency Moody’s monitoring of the situation and the credit worthiness of the United States. These shut downs have been a political football for a while and ordinarily do little damage, but in current climes the world does not need the only shining light of economic activity being dimmed.

The general backdrop for markets is fraught with ever-increasing yields and the subsequent poor performance of bond and stock markets lay testimony to the slow digestion by markets of the ‘higher for longer’ interest rate alignment by the likes of the Federal Reserve and the European Central Bank. Outside of the US, nation industrial performances continue to run in counter to a tightening oil market as China in particular continues to vex those that seek evidence of any increased activity. Although an improvement is shown on today’s data, China industrial profits still shrank by 11.7% for August year-on-year and there seems no getting away from the intense scrutiny of the property giant Evergrande that has not only missed bond payments, and restructuring but, and according to Bloomberg, has had the ignominy of its Chairman being placed under surveillance by Hong Kong police.

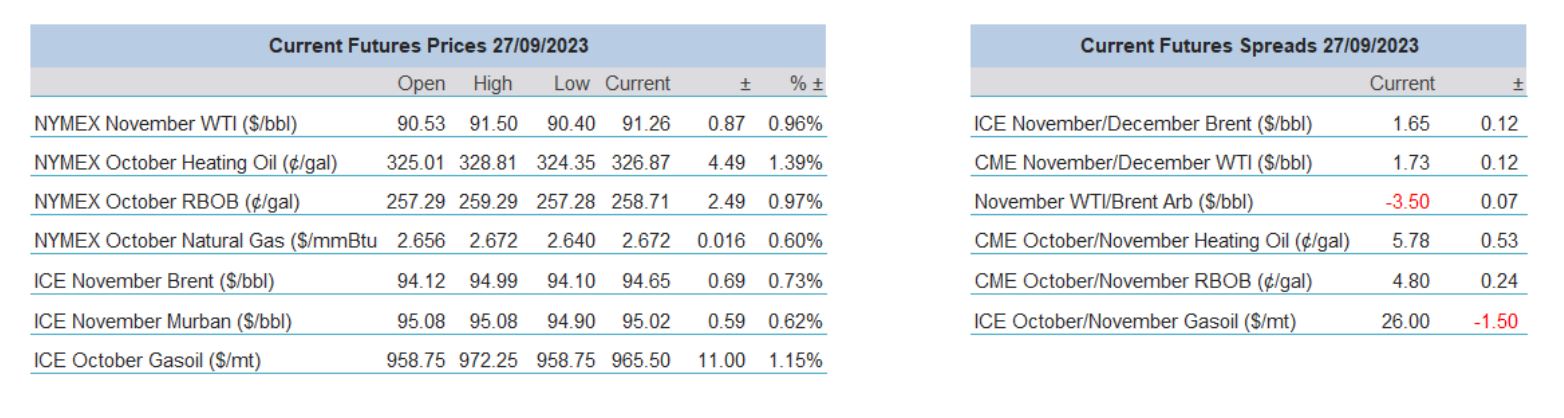

For all the negatives and pontification in the macro-suite that serve bears well, oil’s antidote of tightening structural supply continues to rescue the upward progress even amid a soaring US dollar that almost matches oil rally-for-rally. Yesterday’s API data at first look would seem a little benign. Crude built by 1.6mb against a call of a 0.3mb draw, Gasoline came in on target with a draw of 0.1mb and Distillates drew 1.7mb against a 1.3mb draw call. However, what has the oil market jumping to attention this morning is the draw in Cushing. At -0.8mb, a cursory attitude of ‘so what?’ might be excused, but it belies the now very low situation at the US’s leading oil storage hub. For the case of ease, Cushing’s capacity is pegged at around 100 million barrels according to the likes of TankWatch. Today, the measurement is estimated at 25 million barrels and constitutes a 14-month low. Where this becomes interesting, and a boon for bulls is that operationally, readings approaching 20 million barrels will be considered ‘bottoming’ and that further extraction is increasingly difficult as the remaining oil increases in viscosity, and according to Vortexa and Reuters research, gaps that appear between the top of the oil and the floating lids encourage a build-up of potentially explosive gases. The oil world will await the EIA/DOE data for confirmation later, but a bottoming out of the largest storage hub in the world’s swing producer means oil’s current strength is set to continue.

Not enough ‘green’ for green

One could be forgiven for thinking that the approach to $100/barrel crude oil would give cause for celebration by those in the green lobby and advocates of renewable energy such as offshore wind farms. There has been an assumption, nursed heavily by interested quarters, that accelerated oil prices would bring not only more investment in, but also a quickening of pace in transition to so-called green energies.

In an interesting move and to the chagrin of the green lobby, Rishi Sunak, the United Kingdom Prime Minister, rolled back the targets for fuel driven motor cars. New gasoline and diesel vehicles were to be subjected to a new sale ban from 2030 but this has been eased to 2035. In a lengthy U-turn, Sunak went on to say “[…] at least for now, it should be the consumer that makes that choice, not the government. Because the upfront costs are high. And we have further to go to get the charging infrastructure nationwide.” This action has every right to be charged with political expediency, bearing in mind how unpopular the new Ultra Low Emission Zone in London is proving to be, but there is also pragmatism with what had occurred earlier in the month regarding further offshore licensing.

Part of the UK 2050 zero emission target is the generation of 50 gigawatts from sea-based wind farms by 2030 with the current level estimated at 14 gigawatts. The licensing for generation is put out to auction and disappointingly for all concerned, there was not one bid received. There can be little doubt that Sunak’s car decision was largely influenced by this lack of interest and his language of ‘upfront costs’ chimed with that of potential generators who excused themselves because of supply-line delivery issues and the current state of inflation. Adding to the reluctance of investors/generators is a consideration of any price cap. This price cap is part of the contract for differences (CfD) scheme guaranteeing a fixed price for 15 years if generators successfully bid below the government cap. With the deliverable costs to wind farm projects prohibitive, even with government subsidies, potential profits are clipped well before a turbine blade gets to feel a puff of wind.

This is not peculiar to Europe alone. Last month there was an auction held by President Biden’s administration for offshore wind development in the Gulf of Mexico. Of the 3 partitioned areas up for grabs only 1 received a successful bid. This is not a like-for-like comparison as the problems for wind generation in the Gulf include erratic winds and no legislation forcing abutting States to use wind generated power, but common ground in reluctance can be found in similar excessive costs to development. Even the much more successful rollout of offshore generation in the NE United States comes with quite an environmental scrutiny and any expansion of wind power, ironically, will be threatened by ecological groups.

Just over a week ago, Saudi Arabia barked out at the IEA for moving away from forecasting to political advocacy. Indeed, since 2021 the IEA has been a flag carrier for energy transition after it called for new investments in oil, gas and coal to stop if the global 2050 climate targets were to be met. Therefore, it is unsurprising that yesterday it doubled down by calling for global renewable energy capacity to expand to 11,000 gigawatts by 2030 with investment increasing from the current $1.8 trillion to $4.5 trillion by that year. Such eye-watering amounts of money are not to be had from the private sector because of the discussed costings and which government could persuade voters to take on more substantial national debt after a pandemic and world-altering war?

Rishi Sunak is at present right in his pragmatism, it might be the only time he finds accord with China. “Completely phasing out fossil fuel is unrealistic,” said Xie Zhenhua, China’s climate envoy to the UN (Bloomberg). “We should build the new before discarding the old,” he said, calling for an understanding of the challenges faced by individual countries. The state of world finances and the parochial nature of nation states in protecting their own energy security, means that one-hundred-dollar crude might not yet be the great catalyst and incentive for energy transition.

Overnight Pricing

27 Sep 2023