Oops!... He Did It Again

• I expect to be bombing, because I think that’s a better attitude to go in with. But we’re ready to go. I mean, the military is raring to go – President Trump

• I don’t want to do that (extending the ceasefire). We don’t have that much time – President Trump

• Today, all the spare capacity is behind the Strait of Hormuz, so the impact is very direct... The billion barrels of oil is now effectively baked in, because we have probably already lost 600–700 million at this stage. By the time things start moving again, it will take time to restore supply, which will bring the total loss close to one billion barrels. This is manifesting itself predominantly in Asian economies – Vitol CEO at FT Commodities Summit

• I have therefore directed our Military to continue the Blockade and, in all other respects, remain ready and able, and will therefore extend the Ceasefire until such time as their proposal is submitted, and discussions are concluded, one way or the other – President Trump

After another change of heart in less than 24 hours, the picture is no clearer than it was yesterday, yesterweek, or yestermonth. The indefinite extension of the temporary ceasefire will keep the Strait of Hormuz effectively shut by both Iran and the US, making it the most closely guarded shipping route in the world. No oil will flow through it in the foreseeable future.

Investors will remain glued to their screens for clues, especially those tracking the US President’s Truth Social page. Still, it will also be worth paying attention to the latest US inventory reports. The API reported a combined decline of 14.3 million bbls post-settlement last night. If the EIA confirms the draws and US weekly exports of both crude oil and refined products remain robust, this will be taken as confirmation that consumers in Europe and the Far East are scrambling to secure oil supplies wherever, whenever, and however they can.

This shortage is expected to persist well beyond the resumption of normal flows through the Strait, which appears to be the prevailing view expressed at the FT Commodities Summit.

Ebullient Investors

Without any doubt, investors are expecting a swift conclusion to the completely unnecessary conflict between the US/Israel and Iran, which at one point pushed oil prices up to $120, drove equities below 6,400 points on the S&P 500 index, reignited inflationary fears, and brought the issue of national energy security back into focus. There is a puzzling detachment between soft and hard data and the actual performance of different asset classes, such as oil and equities.

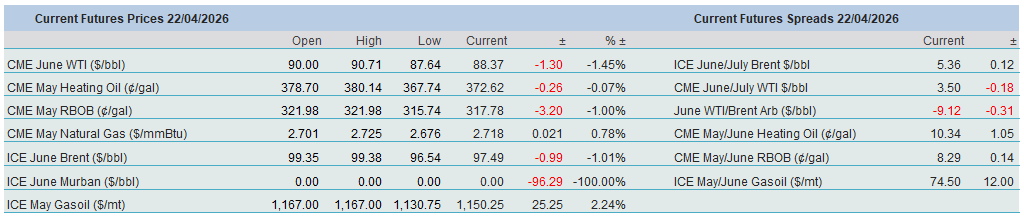

Let us take oil first. For the whole of March, front-month Brent averaged $99.60. For the second half of last month, the mean price was $107.52. This compares with a month-to-date average of $99.19, as the June Brent contract has dropped around $13 from its April peak. All the while, in mid-March, when updated reports on the global oil balance were released, the consensus pointed to a 2Q global stock build, with DoC output estimated at 43.27 mbpd (EIA) or 41.90 mbpd (IEA). The impact of the closure of the Strait of Hormuz was not explicitly apparent. Fast forward one month, and DoC production for the current quarter was revised down to 37.6 mbpd by the EIA and to 36.60 mbpd by the IEA.

As a result, material global stock drawdowns are now anticipated, in contrast to the build forecast in March. Yet oil prices have failed to sustain an upward trajectory. Either the rally well above $100 was the product of unsubstantiated panic, and the current loss of 10–13 mbpd over the past 50 days only justifies a Brent price of around $95, or the prevalent opinion is that the Strait will soon fully reopen and the 600-700 million barrels of crude oil and products stranded behind it will quickly quench the thirst of consumers.

The same thought process, but the opposite trend, is observed in equities. Expensive energy is typically deemed as a hindrance to economic growth because it drives up consumer and producer prices while wage growth lags. Yet, sticking with the S&P 500 index, equities have been remarkably buoyant, shrugging off concerns about inflation, stagflation, or recession. The index fell to 6,344 points by March 30, a loss of 8% after the outbreak of war, only to recover all losses and more by last Friday, setting a fresh record high.

Once again, this impressive performance, alongside persistent optimism about unlimited AI-driven support, is likely due to expectations of a short-lived conflict between the antagonists, after which the economic Canaan will be within reach. This sanguine view is antithetical to how international institutions assess the impact of the conflict. Ahead of this year’s IMF–World Bank Annual Meeting, held last week, the former cut its 2026 global growth forecast to 3.1%, with a downside scenario of 2.5% should the conflict persist. There was broad agreement, almost stating the obvious, that the dominant global risk remains the Middle East conflict and the associated supply shock. The institutional response is limited; a resolution can only come through negotiations between the parties involved. Emerging markets and the poorest nations are bearing a disproportionate and unfair share of the burden, as food, fuel, and fertiliser prices rise. It was also noted that a direct consequence of the ongoing conflict with Iran has been increased global fragmentation and diminishing trust in US political leadership.

The meeting concluded that even in the event of de-escalation, an elevated geopolitical risk premium will remain a feature in oil price formation. While sustained rallies may be less frequent, sudden price spikes should be expected. It also highlighted the divergence between physical and derivatives markets; this gap, characterised by relatively weak futures prices versus elevated physical premiums, could persist for some time. Demand is expected to grow more slowly than previously anticipated, but not collapse. Energy security is being prioritised, although both the IMF and the World Bank warned against excessive stockpiling and hoarding.

Oil is no longer purely a macro asset; it has become a geopolitical one. Contrary to the ubiquitous market view, supply disruptions should provide near-term price support, while demand destruction is likely to cap prices over the longer term. This is a reasonable conclusion; one we wholeheartedly share. However, those who agree with this assessment will also be acutely mindful of the classic observation by John Maynard Keynes: markets can remain irrational longer than you can remain solvent.

Overnight Pricing

22 Apr 2026