Operation Epic Failure

Perhaps the US was emboldened by its sensationally nimble military action against the former Venezuelan president at the beginning of 2026 and grew confident that quick strikes on Iran would suffice to remove the country’s oppressive and autocratic regime for the benefit of its people. Two weeks into the conflict, now undeniably a quagmire, it is hard to avoid the conclusion that launching military operations against Iran may have been a massive miscalculation, reminiscent of Putin’s misreading of Ukrainian resilience. Misinformation and disinformation (such as claims that the US Navy escorted ships through the Strait of Hormuz), together with contradictory and outlandish statements, chiefly from the US president, who says the war is both practically won and yet unfinished, reinforce that perception.

One lesson of the past two weeks is that the understandable desire to remove an autocratic regime can have severe unintended consequences when pursued by force. This is a war of choice, not necessity, and the exit is nowhere in sight. Ending it is not solely Washington’s decision, but also that of Israel and Iran. The consequences for oil markets are profound. Prices will continue to dance to the rhythm of headlines, volatility will remain extreme, and any corrections, however sharp, are likely to prove brief unless the unlikely happens: a ceasefire and the complete reopening of the Strait of Hormuz.

Despite mounting evidence that the costs far outweigh any benefits, the weekend’s developments resemble medieval bloodletters doubling down on their action, even as the health of the patient deteriorates. On Saturday, the US attacked the critical Kharg Island, home to Iran’s largest oil export terminal. With roughly 90% of Iranian crude exports passing through it, the terminal is indispensable to the country’s economy. Washington claims only military facilities were targeted, yet the response was swift and severe. Iran sustained, and in some cases intensified, its missile and drone attacks across the region, including against Saudi Arabia, Qatar, and the UAE. In the UAE, a fire broke out at the Fujairah bunkering hub, briefly suspending oil loading before operations resumed. Qatar and Saudi Arabia both reported ballistic missile attacks, while the Iranian Revolutionary Guard Corps declared any US interests in the region legitimate targets.

Meanwhile, Israel’s offensive against Hezbollah in Lebanon continued, and Iran itself has come under intense Israeli assault. The US president urged China, France, Japan, South Korea and others to deploy naval vessels to help reopen the Strait of Hormuz. Yet it is difficult to see how that could happen without Iranian concessions. President Trump insists the terms for ending the war are still inadequate and claims Iran is willing to negotiate, swiftly denied by Tehran. He has not ruled out further strikes on oil infrastructure at Kharg Island, remarking that the US could “hit it a few more times just for fun.”

Whether such statements are viewed as bravado or as insecurity cloaked in machismo depends on political taste. Either way, if this is the major inspiration behind foreign policy, then oil prices of $150 or even $200 must not be discounted, unless domestic pressure, from Congress or within the administration, forces a retreat. Neither Iran nor Israel appears inclined to back down. Is there rest for the wicked and such a reversal possible? In a Trump world, little is certain. Yet US foreign interventions are ultimately judged by two domestic metrics: American casualties and gasoline prices. At present, both are rising.

Shut-ins Widen, Mitigation Fails

Against this backdrop, it is worth assessing the damage already inflicted on the region’s energy infrastructure and the limits of mitigation. Temporary refinery closures are becoming routine. Qatar has suspended LNG production, and energy installations across the Middle East have been struck. Energy Intelligence estimates Gulf producers will pump 8.44 mbpd less in March than in February. Around 4.3 mbpd of refinery throughput has been halted in the past two weeks, including 2.2 mbpd of downstream capacity in the Middle East alone. Attacks on energy infrastructure are now almost as disruptive to oil flows as the closure of the Strait itself.

The UAE and Saudi Arabia can reroute some exports through pipelines, but only partially. The IEA has coordinated a release of 400 million barrels from strategic petroleum reserves, out of 1.2 billion barrels of total stocks, over 90 days, equivalent to roughly 4.5 mbpd. The US Treasury has also issued a 30-day sanctions waiver for Russian crude and products held in floating storage, reportedly amounting to 124 million barrels. Iran, for its part, is deploying its shadow fleet across the Strait of Hormuz. Estimates suggest global floating storage has already declined by 20–40 million barrels over the past two weeks (1.3–2.6 mbpd).

Washington is also considering a Jones Act waiver and naval escorts in the Gulf to restore shipping. We incorrectly stated last week that such escorts were not legally permitted. They are. Whether they are practical is another matter: US or allied naval vessels would become sitting ducks for Iranian forces. It is hardly surprising that Australia and Japan have outright rejected Donald Trump’s demand to reopen the Strait by sending ships.

Collectively, these measures are significant, yet the market appears largely unmoved. Investors seem to recognise that if just two weeks of disruption at Hormuz have inflicted this level of damage on production, exports, and refining, the consequences of a prolonged conflict, one with no visible end, would be severe, especially as inventories are steadily depleted. The loss of 8–10 million barrels per day quickly compounds to extraordinary levels. Given the Strait’s strategic importance, surplus capacity, largely located in the Middle East and recently downgraded by the EIA by 700,000 bpd for the second and third quarters, offers little real relief.

Peace looks distant, and even a ceasefire appears unlikely in the near term. For the Iranian regime, the Strait of Hormuz remains the most powerful lever in its existential confrontation with the US and Israel. Washington, meanwhile, shows little willingness to compromise short of Iranian capitulation. Even if normalisation eventually arrives, markets will remember that the Middle East has anew become a barrel filled not with oil but with gunpowder, where a single spark could ignite the entire region. Ships may sail again, but the risk premium will endure, and a return to pre-crisis price levels looks improbable.

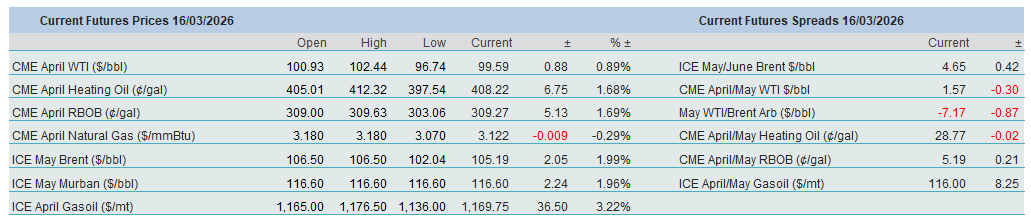

Overnight Pricing

16 Mar 2026