Our War, Your Problem

Allegedly, the war has been won, yet there are no signs of de-escalation. If anything, tensions and tempers are running higher than before. Israel’s killing of the Iranian security chief and the head of the Basij militia has made the country’s leadership more defiant in continuing the war against its adversaries. Thus, it comes as no surprise that the supreme leader has reportedly rejected indirect offers to negotiate, while Tel Aviv has been targeted overnight with missiles carrying cluster warheads.

The war rages on. Loading operations at the port of Fujairah in the UAE have been disrupted once again, and operations at the Shah gas field remain suspended. The UAE’s oil production has halved. Monday’s sell-off proved to be merely a correction, as oil regained most of the previous day’s losses.

Amid the prevailing nervousness, sellers re-emerged this morning. In an attempt to alleviate the supply deficit, the US eased sanctions on Venezuela. More importantly, Baghdad and the Kurdish Regional Government agreed to resume oil exports via the Kirkuk–Ceyhan pipeline. The central government aims to initially pump 100,000 bpd through this alternative route, which has a usable capacity of around 300,000 bpd. While the agreement brings much-needed supply relief, even full compliance will not meaningfully offset the disruption caused by the closure of the Strait of Hormuz.

As the US continues relentlessly tilting at Iranian windmills, or more accurately, drones and mines, the president has opened another front in his broader Middle East campaign. After his calls for NATO, a defensive alliance, to support the US offensive on Iran fell on deaf ears, he warned of “a very bad future,” only to execute a characteristic U-turn, claiming that “we no longer need… assistance—WE NEVER DID.” Making sense of these demands, threats, and bullying has long proved futile. What this suggests, however, is that any reassuring resolution to the ongoing Middle East war remains a distant prospect; uncertainty and volatile trading conditions are likely to persist.

It’s the Strait, Stupid

As the conflict between Iran and the US/Israel enters its third week, the impact on oil prices is clear. There are arguments both for and against the idea that hostilities will drag on and keep oil prices elevated, but drawing a firm conclusion would be risky. What is discernible, however, is that the recent rally in oil has had a tangible and adverse impact on equities. There are also regional divergences: the Far East is more dependent on Middle Eastern oil than, say, the US; firstly because the region is a natural source of crude oil and refined products needed to keep the manufacturing sector humming, and secondly because Japan, South Korea, China, and their peers are not members of the global oil-producing club.

Stock market performance reflects these regional differences. The US S&P 500 index has shed less than 2.5% of its value since February 27, whereas the South Korean stock market has fallen by around 5% over the same period, including today’s rally of 5%. Different countries suffer to varying degrees, but the suffering itself is collective. One unit of the MSCI All-Country Index bought 14.5 barrels of Brent at the end of February, compared with just 10 barrels at last night’s close. While it remains unpredictable how long the war will last, the longer it takes to restore stability in the Persian Gulf, and the longer oil remains comparatively expensive, the greater the economic damage and the more painful the eventual recovery.

A comparison with Russia’s invasion of Ukraine may not be entirely appropriate. Although both wars can be characterised as supply shocks, the oil market adapted surprisingly quickly to the new status quo four years ago, and the economic impact was consequently blunted. The current supply shock, given the lack of optionality, is more severe, and its impact on trade, supply chains, and the broader economy is likely to be greater. In an FT op-ed, the author argued that the current crisis is more akin to last year’s “Liberation Day” tariff announcement, from which markets recovered impressively. However, the argument goes, this shock will be graver, as surging energy prices deprive central banks of their ability to support the economy by lowering borrowing costs. Instead, rates may have to remain unchanged or even rise again as concerns about renewed inflationary pressures intensify.

The Bank for International Settlements shares this view. It warns that a prolonged stand-off will cause profound damage to the global economy, lead to higher interest rates, and trigger a sell-off in financial markets. Rising borrowing costs will also have an adverse fiscal effect: higher financing costs could undermine fiscal sustainability at a time when public finances are already stretched. This would likely necessitate either higher taxes, lower spending, or a combination of both, neither of which is conducive to growth.

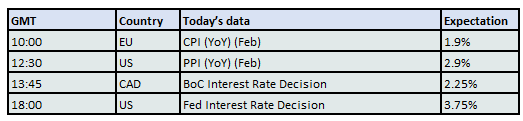

And what about monetary policy? We will find out soon enough. The Australian central bank has remained hawkish, raising interest rates this week for the second time this year. The Fed and the Bank of Canada are set to decide on borrowing costs today, followed by the Bank of Japan, the Swiss National Bank, the Bank of England, and the European Central Bank tomorrow. It is important to recall that central banks once labelled the post-pandemic surge in consumer and producer prices “transitory” and were slow to raise rates between March and November 2021, only to embark on an aggressively restrictive policy in 2022. They are unlikely to repeat that mistake; if there is any sign of persistent inflation, rates will remain elevated or rise further.

Finally, the deteriorating relationship between the US and its allies may also weigh on economic prospects. Few countries have avoided being alienated by the US/Israeli attack on Iran. Middle Eastern allies that host US military bases must now contend not only with the loss of petrodollar revenues but also with setbacks to their efforts to diversify their economies away from oil. Their pledges of large-scale investment in the US may be reassessed. Japan and South Korea, heavily dependent on Middle Eastern oil, may also reconsider their compliant trade stance towards the US. Friction with China is also plausible, as the world’s second-most populous country has lost access to heavily discounted oil. Europe, reliant on Middle Eastern gas, is likely to intensify its efforts to reduce dependence on the US. The seeds of a broader trade conflict between the US and the rest of the world are being sown.

The immediate impact of a potential closure of the Strait of Hormuz, something the US administration may have significantly underestimated, is higher energy prices and, given the emerging fertiliser shortage, rising food inflation. If the conflict persists, the medium-term consequences are likely to include slower economic growth and increasing US isolation. The initial damage has already been done, and the window to limit further harm is closing. Not as rapidly as the Strait of Hormuz itself, perhaps, but the longer the war continues, the greater the pain. Alas, the US’s objectives in Iran remain unclear, and the end of the conflict is nowhere in sight.

Overnight Pricing

18 Mar 2026