Past the Point of No Imminent Return

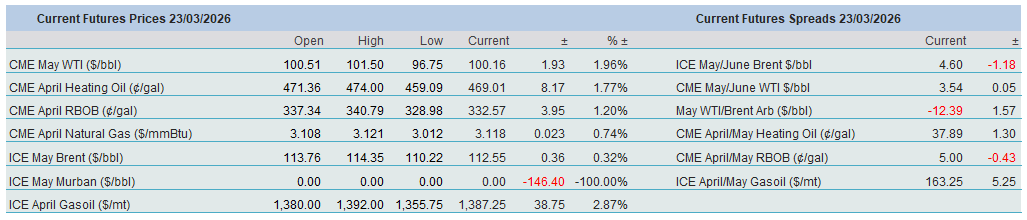

Probably even for oil industry veterans, last week’s events and developments exceeded the definition of “unprecedented.” Geopolitical upheavals or wars around oil-producing regions or major energy hubs have always precipitated wild swings. Yet observing May/June WTI dropping more than a dollar in less than three hours last Wednesday, or the May WTI/Brent arbitrage collapsing by over $10/bbl in less than a day—only to rally by $8/bbl in the ensuing six hours—is beyond what can be explained away by anxiety or fear.

The truth, most probably, is that politics, the economy, and the short- and long-term oil balance have become far too complex for anyone—decision-makers, traders, investors, stakeholders, or the average person—to fully comprehend. Interpretations and assessments of events, therefore, are to a large extent left to algorithms and computer programmes reacting to soundbites and key phrases. And when globalisation is receding, multilateralism is replaced by unilateralism, and international order is ignored, the result is unpredictable and unforeseeable incidents. Conducting domestic and foreign policy through bullying and exploitation rules out constructive criticism. It turns the flow of information into a one-way street, which in turn leads to clouded judgment. The quality and trustworthiness of critical, far-reaching decisions will deteriorate, and markets will become increasingly volatile.

Yet it is what it is, and whilst the Iranian conflict, way ahead in the future, might serve the purpose of realising that cooperation, as opposed to fragmentation and coercion, is the more effective way to organise our world, the more pressing questions are how and when the latest chapter in the unnecessarily rich history of the Middle East will be amicably closed, and how energy markets and prices will be impacted in the interim.

Ambiguity prevailed over the weekend. The US President, in the same breath, ruled out a ceasefire with Iran and considered winding down the military operation against the Persian Gulf country, whilst deploying thousands of Marines to the conflict zone. The way the war is being masterminded from Washington, DC, is the political equivalent of the “Random Walk” theory, as future movements cannot be foreseen. The goals of the other two actors in the war are much clearer. Israel appears to see an unmissable opportunity to remove the current Iranian regime, which has sought to destroy the Jewish state for decades. The Israeli Prime Minister may also believe that the longer the war lasts, the higher the odds of him winning another war, this year’s election and avoiding indictment for bribery and fraud. For the Iranian leadership, the conflict is existential. A US military withdrawal, whatever form it takes, will not end the war unless there are mutual guarantees on reopening the Strait of Hormuz and preventing future attacks, including reparations for destruction. Such assurances are implausible, to say the least.

It is becoming a cliché that a protracted conflict will cause severe damage, both politically and economically. Central banks adopted the most pragmatic approach last week by leaving interest rates unchanged amid growing and palpable anxiety over rising inflation. And it is not just skyrocketing energy prices that could drive consumer prices higher and, consequently, increase rates. The severe disruption to fertiliser exports will trigger food inflation, while the emerging scarcity of helium is threatening the global tech supply chain, the single biggest supporter of the pre-war stock market rally. After holding interest rates steady, the ECB raised its inflation outlook for the next three years (from 1.9% to 2.6% in 2026) and cut this year’s growth forecast for the euro area from 1.2% in December to 0.9% last week.

Central banks are in the enviable position of being able to print money when liquidity must be ensured. As astutely put by the Financial Times, oil producers, especially the central bank of the oil market, OPEC, cannot emulate this strategy; it is impossible to print molecules if a shortage looms. The damage caused by the closure of the Strait of Hormuz and continued attacks on the region’s energy infrastructure has already been substantial. It could worsen considerably if the war persists, even though Iranian-approved ships are still transiting the narrow passageway. Crude oil and condensate exports from the region have declined by around 12 mbpd, according to consultancy Petro-Logistics. Energy Intelligence estimates that the loss of global refining capacity stands at 5 mbpd, with utilisation rates at a four-year low.

Saudi Arabia has cut production by 2 mbpd, output from the UAE has halved, and Iraqi production has fallen from 4.3 mbpd to 1.3 mbpd. Kuwait declared force majeure on its crude oil exports on March 7. Consultancy IIR estimates that Middle Eastern refiners have reduced capacity by 1.9 mbpd. Qatar also declared force majeure on its LNG shipments on March 4. Most alarmingly, the damage caused by Iran’s retaliatory strike on the Gulf nation’s Ras Laffan LNG plant at the end of last week has worsened the global LNG outlook beyond imagination. If the word “Armageddon” applies to any part of the ongoing conflict, this is it. Qatar accounts for 20% of global LNG supply, and the plant could be offline for as long as five years. Mitigation measures, be they SPR releases, sanction waivers, or alternative transportation routes, are ineffective. The oil balance will be tighter than projected before hostilities broke out, and the risk premium will stay elevated long after production and exports normalise.

However, talks of de-escalation seem premature; escalation is more likely. Consider intensifying Iranian attacks on oil wells, refineries, and ports in the region, or assaults on ships attempting to transit the Strait. Nor should one rule out a fresh US offensive against Kharg Island. It will take a long time to recover from the damage already inflicted, and further disruption could easily push Brent prices above $150/bbl, with Asian consumers bearing the brunt. De-escalation, for the sake of all stakeholders in this conflict, cannot come soon enough, yet it is impossible to predict when that moment will arrive. Probably when we feel it—feel it in our bones.

Overnight Pricing

23 Mar 2026