Possible Ceasefire Extension

Markets are warming up to the prospect of some form of peace agreement being reached in the not-so-distant future. These hopes were boosted yesterday as the US and Iran are reportedly on the verge of keeping the hatchet buried for another 60 days, subject to approvals by Donald Trump and the Iranian leaders. During these two months, according to the US version of the tentative truce extension, Iran would gradually reopen the Strait, remove mines and refrain from charging transit fees. In exchange, the US would lift sanctions in phases and unfreeze Iranian assets held abroad. In the meantime, negotiations on the pivotal issues discussed below would get underway.

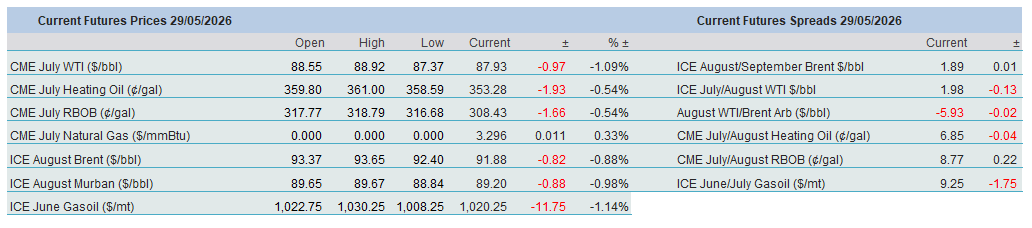

Even scaremongers admit that keeping the truce alive is a welcome development. Yet, what appears to be a discouraging sign is the effect the war has had, and will continue to have, on the global economy. Although oil prices failed to regain previously lost ground yesterday and are trending south this morning, and equities advance further, strong US exports of oil products continue to keep domestic and, by extension, OECD, inventories in major categories well below the seasonal average, thereby setting a floor under oil prices. And when energy is comparatively expensive, consumer prices remain elevated. The Personal Consumption Expenditures Price Index, the Fed’s preferred measure of inflation, increased by 3.8% (headline) and 3.3% (core) in April, significantly above the 2% target. Meanwhile, US economic growth in the first quarter was revised down to 1.6%. Current optimism and the hard economic and inventory data remain out of sync, or in the battle between expectations and reality, the former is winning.

Peacing it Together

When the US attacked Iran more than two months ago and, as a retaliatory measure, the Persian Gulf nation struck US military bases, oil prices jumped by well over $5. The reaction to similar circumstances was much more muted yesterday. History does not repeat itself, although it rhymes, if you will. It is telling that the initial rally of $4 in the early hours of yesterday’s trading was followed by a drop of $3 during London morning, or, in the words of my esteemed colleague, the ‘buy the dip’ attitude has turned into a ‘sell the rally’ approach. The explanation, it would seem, is mundane. The recent exchange of fire is part of the peace talks, desperate leverage-seeking from parties who know that there will be no winners, that this war should not have started, and that the response to it was disproportionate; nonetheless, they are reluctant to admit it.

So, if one accepts that there will be an agreement, whether fragile or solid, temporary or permanent, how would the market react? We must remember that, in intense anticipation of a deal, oil is already $34, or 27%, below the peak of the year, on a Brent basis. Is it going back to where it came from, around $70, in the event of a cessation of hostilities? When trying to draw a conclusion, it is reasonable to categorise the possibilities into what we do not know, what we know, and what we suspect.

What we don’t know: the details of any potential long-lasting peace deal. Several pivotal points need to be agreed upon. As far as the oil balance is concerned, the most salient of these is the reopening of the Strait, the blockade of which by both parties is flatly illegal under international maritime law. Will oil flow unhindered, or will Iran be able to control this passageway? Will there be a toll? The inability to provide reassuring answers to these questions could cause serious delays in striking an agreement.

It is important to recall that the initial reasoning for the conflict was the removal of the current Iranian regime, the dismantling of its regional proxies, and the deprivation of the leadership’s nuclear capabilities, including a ban on nuclear enrichment. Failure to limit Iran’s nuclear capabilities will render the war itself a catastrophic mistake and will plainly show that the Obama-era JCPOA agreement was superior to the Trump administration’s foreign policy MO, something that the incumbent President will simply not accept.

What we know: the damage the conflict has already done. Despite the relentless march higher in US stock prices, the economic headwinds are plain to see. Monetary doves are turning into hawks. Several central banks have already tightened policy by increasing interest rates; the ECB will plausibly do so in June, and the Fed, under the leadership of the new Trump appointee, will most likely refuse to cut. Inflation is elevated and will remain so. US consumer prices rose by 3.8% in April, far exceeding the official target of 2%. Consumer sentiment in the world’s biggest economy is bleak and at its lowest level in 70-odd years, the University of Michigan survey found. Eurozone inflation jumped from 2.6% in March to 3% in April. It will take time for consumer prices to retreat to their declared objectives, along with all the adverse economic repercussions. Oil demand growth will ultimately slow.

What we suspect: the impact of the energy shock will be felt in the near and perhaps even the medium-term future. While a deal is eagerly awaited by every man and his dog, global oil inventories will keep depleting. After the adversaries announce an agreement and traffic resumes through the Strait of Hormuz, it will take months for energy flows to normalise. According to the CEO of the Abu Dhabi National Oil Company, the time frame is around four months for traffic volume to reach 80% of the pre-war level. Oil fields that were shut down will need even longer than that to restart. A backlog of about 2,000 stranded ships needs to be cleared. Some of the freed-up oil will have to be used to replenish depleted storage. Damaged LNG infrastructure could take years to repair. And, of course, lest we forget, the summer driving season has arrived, and global oil demand will see a seasonal uptick. The mean estimate for 3Q global demand expansion is 2.26 mbpd from the current quarter.

Even if a credible deal is struck, global and regional oil inventories will plausibly continue drawing. The pace might slow, but there will be less oil in storage, whether industrial or strategic. It takes a bold, or even brazen, man to predict where prices will be in one, two, or three months. Although we are not among them, we can resist everything but temptation. The balance of what we do know, what we do not know, and what we suspect implies that, whilst rallies are currently viewed as selling opportunities, the announcement of a deal could be reminiscent of the reverse Gulf War I syndrome. When the present bearish perceptions are proven accurate, it will be time to cover.

Overnight Pricing

29 May 2026