Pragmatism, not Panic

Every war is idiosyncratic; it has its own characteristics. Motivations, impacts, and outcomes can and do differ. It may be a futile exercise to compare the current Iranian conflict with Russia’s invasion of Ukraine; nonetheless, attempting to highlight what is common and what is different in these geopolitical events could help assess how high oil prices might rise.

In both cases, the instigators have their well-publicised and, in their own view, justified reasons. Curiously, however, these are so wide-ranging that they can be viewed as contradictory and even laughable—if they did not have such severe effects on society, international relationships, and the global economy. Vladimir Putin presented the aggression against his western neighbour as necessary to protect the Russian-speaking population in Ukraine. Alternatively, it was to prevent NATO expansion, or to demilitarise and “denazify” the country. The pretext for the US/Israeli assault on Iran was, according to the Israeli Defence Minister, to “remove imminent threats against the State of Israel.” The US Secretary of State, acknowledging Israel’s action, said the United States had to act “pre-emptively.” President Trump emphasised that Iranian missiles can reach the US and that action was therefore inevitable, although this claim was not supported by US intelligence. Regime change is another frequently cited reason.

A common feature of these two wars is that both fly in the face of international law. A major difference is that the Russian Duma, surprise, surprise, authorised the invasion, while the US Congress did not approve of the strike against Iran. The Senate, however, on Thursday blocked a motion aimed at stopping the air campaign. It seems that a well-crafted narrative, story, or fiction is often more than sufficient to launch military interventions against perceived or actual enemies.

Although this is a subjective and possibly premature observation, the broader picture suggests that the damage caused by these wars outweighs their benefits, at least on a global scale. Russia’s invasion was the primary reason for the slowdown in the fight against climate change; it contributed to inflationary pressures and the realignment of political relationships at the expense of economic prosperity. The current crisis has also raised fears of slower global growth and a possible backlash against unilateral or bilateral military actions carried out with impunity.

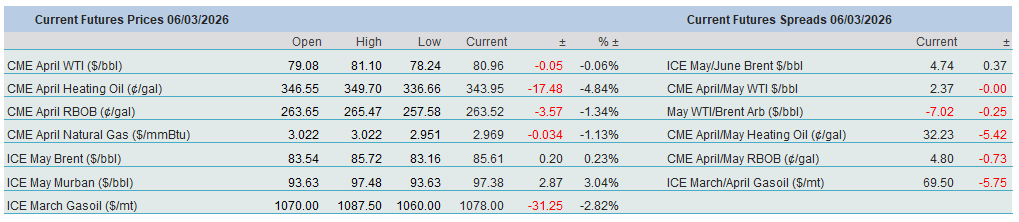

One of the starkest differences between the Ukrainian and Iranian conflicts can be found closer to home, namely in the oil market. Investors appear comparatively less apprehensive about the current crisis. In 2022, Brent rallied to $140/bbl with around 7.5 mbpd of combined Russian crude oil and product exports in jeopardy. Today, the now-infamous Strait of Hormuz could prevent around 20 mbpd of oil from reaching international markets. Yet Brent remains a long way from flirting with the $100 milestone that many feared would be breached if Hormuz were closed. Is it an insouciant or justified attitude?

Recent events do not fully confirm this apparently blithe approach. The relentless widening of backwardation and the surge in global crack spreads to stratospheric levels clearly display a considerable degree of anxiety about a very real shortage of crude oil and, consequently, refined products. Yet it is noticeable that the premium of roughly $12.5 that M1 Brent commands over M7 remains well below the $18 level registered in March 2022. Yesterday’s price jump was yet another proof of growing supply worries. Iraq has been forced to cut output by 1.5 mbpd due to swelling storage. Kuwait and the UAE might follow suit shortly. Resuming production, whenever it comes, will take time. India, Reuters reports, is paying a hefty premium for Russian crude oil, a jump of more than $15/bbl in the differential compared to last week. No tanker passes through the Strait of Hormuz. China has suspended product exports, Asian (and global) crack spreads are rallying out of sight.

The flexibility of oil exporters and traders, demonstrated during the Ukrainian war and the Gaza conflict, does not provide a fully satisfactory explanation either. Russian-friendly oil buyers took advantage of depressed differentials, a shadow fleet emerged, and cargoes were routed around the Cape of Good Hope instead of through the Suez Canal. These adjustments merely redirected oil flows rather than disrupting them. The Strait of Hormuz, however, does not have a true alternative. The East-West pipeline in Saudi Arabia and the Habshan–Fujairah pipeline in the UAE bypass the Strait, but together they would only alleviate the disruption by roughly 3–3.5 mbpd, leaving well over 16 mbpd at the mercy of Hormuz.

So why is oil not significantly higher? One possible explanation lies in inventories. To begin with, oil stored on water amounted to about 1.82 billion barrels, according to S&P Global (December estimate). The White House yesterday issued waivers for Russian oil purchases, and, oh boy, there is an abundance of Russian crude stored in tankers. At the end of 2021, prior to Russia’s incursion into Ukraine, OECD commercial stocks stood at 2.65 billion barrels (OPEC data). This compares with 2.85 billion barrels at the end of last year.

Non-DoC supply growth is pencilled in at just under 2 mbpd for 2026, compared with around 1 mbpd in 2022. In 2022, the global economy was recovering from the devastation of COVID-19, and annual demand growth was estimated at 4.5 mbpd. In 2026, it is expected to reach only 1.4 mbpd. You got the picture.

Most importantly, market participants plausibly factor in the difference in the personalities of the two world leaders. Putin has been waging his war for more than four years largely because of ideological convictions. Donald Trump, by contrast, is more likely to pursue immediate success, whatever form that success may take. While in an autocracy such as Russia, public discontent is rare, if not entirely absent, the United States remains a functioning democracy. Although political checks have weakened, stock markets and bond yields still exert a credible restraining influence on the president.

Investors are growing more confident that, with equities falling, US retail gasoline prices well above $3 per gallon, and midterm elections only a few months away, the conflict will not be protracted. What shape possible concessions might take is not evident, but the pressure on the US administration to act is clearly growing. Hence, last night’s bizarre announcement about intervening in the futures market to tame galloping energy prices. Will cutting physical oil supply be countered by slashing financial oil demand? Hmm.

Whether the above represents the ubiquitous view is naturally debatable, but it could be. The market is less hectic and fearful than it was in 2022. This is not to say that a break above $100/bbl is implausible; under the current circumstances, of course, it is. Every day that passes without signs of de-escalation brings another jump in prices. Yet asking where prices will peak may turn out to be the wrong question. A more reasonable one is when, and the answer is probably weeks rather than months.

Overnight Pricing

06 Mar 2026