President Trump tarrifies the world, and it should be scared

Last week oil prices saw eventual limited outcomes with the two main crude futures prices falling between 2 and 3% with products registering even more meagre declines. It really did not matter what might occur with weather, wars and what OPEC might do, it was all about President Trump ‘tarrifying’ the market, used here as not only a state of trade, but also emotion. Sure enough, the reticence by oil protagonists was rightly judged as the new President put fact to threat and imposed 25% tariffs on Canada and Mexico with China incurring 10%. Even though Canada’s energy sector will only be subject to 10%, and applied later in the month, the tectonic plates of world trade take a massive shift over the weekend and the fallout is beyond prediction.

Economists gather round the expectation of higher inflation within the US, slowing global trade and in the case of Canada and Mexico, economies being thrown into recession. Tariffs are now the main weapon of trade negotiation, which means they may as easily be rescinded as be levied. The only guarantee for market risk takers is uncertainty, at times welcomed in opportunity, but in the main it will make for a jittery day-by-day existence with bullish and bearish news becoming confused and dare we say ‘fluid’.

Today sees such ruction. Stock markets have been hammered overnight, bourses in Australia, South Korea, and Hong Kong on its return have all fallen by around 2%, with Japan’s Nikkei faring worst by dropping nigh on 3%. In Europe, the main bourses of Germany, France and the UK are lower by 1.5-2% on futures markets and their US counterparts have not been spared. The Dow is -1.5%, S&P -2% and Nasdaq -2.5%. The mini contagion has not kept within the borders of stock markets, crypto has felt the cold hand of risk evacuation. On Friday, Bitcoin was trading $104,500, this morning it has been as low at $92,000. In currencies, and against the US Dollar, the Canadian Dollar has fallen to a 20-year low, Mexican Peso a 2-year one and a tariff threatened Europe sees the Euro drop to 1.03, a level not seen since the pandemic. Flight into the greenback is confirmed by the sharp rally in the US Dollar Index (DXY) to 109.50 after experiencing a bout of disfavour following the inauguration of January 20.

Despite the Dollar strength, oil prices have put in a decent rally at time of press as 500kbpd from Mexico and 4mbpd in the case of Canada are at risk. While this might be bullish for crude in the future (speculated on below), it is the immediate issue for refiner feedstock that concerns oil patrons and how that will be reflected in product price, particularly that of Gasoline.

Could Canada’s loss be OPEC’s gain?

The considerations that beset OPEC as it gathers this week are many and varied for not only will the cartel’s members have to show the usual political cunning and guile to squeeze the best deal for each of their country’s oil industry, negotiating a plan will also have to encompass an outcome that offers appeasement to a prowling Donald Trump which is probably something they could do without. However, it is worth considering that the further alienation of Russia by the fresh sanctions of Joe Biden will actually help OPEC’s cause.

Tracking the amount of Russian Crude getting to water is made difficult by the dark fleet consideration, but according to S&P Global Commodities at Sea data, middle of January shipments averaged close to 4mbpd. Sanctions will obviously take time to inflict damage on flows but customers in Asia are not hanging around in trying to replace the barrels. From March, India and China will stop making purchases of Russian oil and will instead seek alternative sources. Asian grades are represented in how Dubai is commanding stronger premiums to the main benchmarks of WTI and Brent. At one-point last week February WTI/Dubai fell to a discount not seen for 2 years and Brent/Dubai the lowest since 2015. Dubai is considered to be a medium grade crude oil, but compared with Brent and WTI it would be regarded as heavy. It is a favoured feedstock in Asia as it satisfies the area’s processing plant’s preference for more sour grades but is adaptable for lighter processing in the massive plastic industries. Asia is not the only oil arena needing heavy crude.

In the age before fracking and shale, US refiners obviously relied on foreign imported crude grades which when compared with WTI condensate were generally much heavier. Processing was then geared accordingly; therefore, heavy crudes are a necessity for the refining sector as running domestic lighter crudes is inefficient. Last year, it emerged that crude from Permian is getting sweeter as drilling moves from first-tier drilling areas into those that contain more natural gas and are lighter in make-up. WTI Midland had consistently showed a gravity of an average of 40 degrees, this has now lightened to 42 degrees giving US refiners a headache. Lighter crudes are very much welcomed if the plastic feedstock of Naphtha is the intended product but no so if it is motor fuels such as Gasoline and Diesel. Crude blending then allows for greater efficiency and indeed profits. According to American Fuel and Petrochemical Manufacturers (AFPM), more than 70% of U.S. refining capacity runs most efficiently with heavier crude. That is why 90% of crude oil imports into the United States are heavier than U.S.-produced shale crude.

The tariff threat that hangs over Canada remains questionable, which is why at present the level is set at 10% for energy and will be implemented later this month. This offers the notions of pragmatism from Washington and that everything is Trump-transactional. There are important reasons why. The US’s greatest source of heavier crude is from its northerly neighbour’s Western Canadian Sedimentary Basin (WCSB). Canada produces 5.5mbpd of which over 4mbpd finds its way south. Importantly, the inland regions in the US of the Midwest and Rocky Mountains or PADD 2 and PADD 4 are served by pipelines. Replacing Canadian crudes into this geography will be more than problematic. Given the state of Asian Crude grades including heavier ones, and their current commanding of premiums to both WTI and Brent, adding a US bid into that mix is not only financially unviable it must be politically so. Imagine a US oil industry having to go cap-in-hand to those who NOPEC Senators labelled ‘market manipulators’ of OPEC? The US benefits, and its leaders brag on, energy self-sufficiency, but in fact oil independence is made possible by the mineral wealth of Canada.

This cannot be unnoticed by OPEC. How tariffs are made manifest, and their viability were keenly argued in Friday’s report. The ramifications for international trade are undoubtedly bearish. However, in the short-term tariffs and sanctions can be bullish. The state of premium enjoyed in Asia crudes is intriguing, it will only be made more so by improving if Canada’s oil is indeed subjected to tariff. In such a scenario, OPEC can afford to bring barrels back to the market and satisfy the shouting of the US President. This will probably just be a bringing forward of the proposed reintroduction outlined for April, but the US’s punitive trade action on Russia’s side-effect, and possibly Canada’s, makes for an easier meeting for the cartel than it probably envisioned.

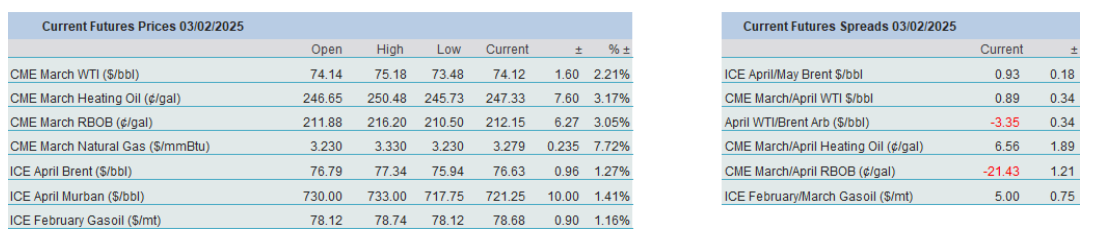

Overnight Pricing

03 Feb 2025