Products win out again

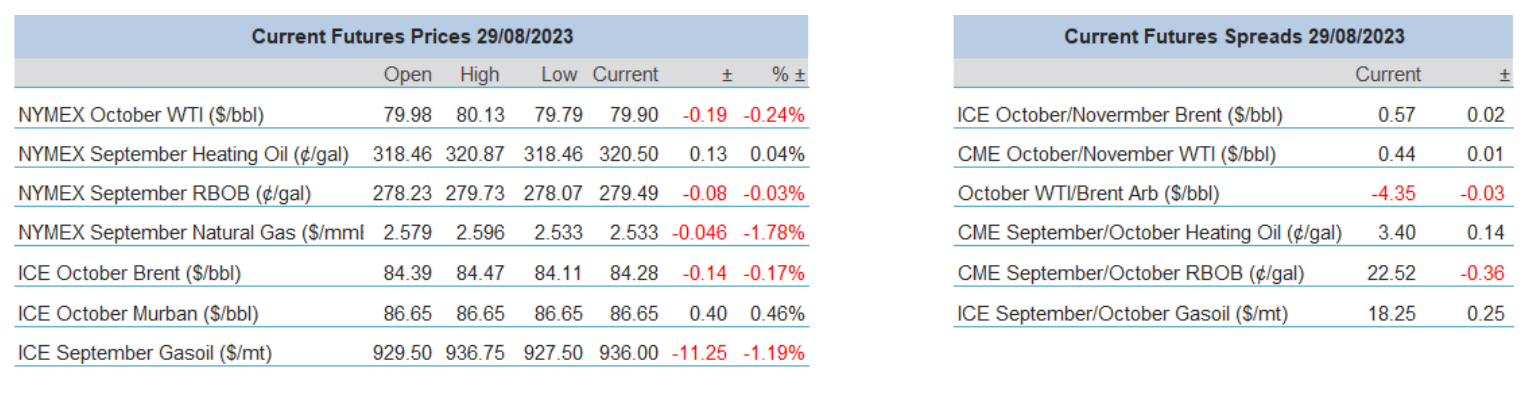

The changes in weekly prices examples the state of the current play within in the oil complex as products yet again outdo the performances of the crudes with some style. While WTI finished Friday -$1.42/barrel and Brent -$0.32/barrel on the week, Heating Oil was 14.78c/gallon higher, RBOB 5.32c/gallon higher backed up with a positive ending for Gasoil gaining $26.25/tonne. As much as the market accepts a derivative driven rally it would appear that aggregation in the recent commitment of traders report, crudes still show something of a reticent tone. Bloomberg’s averaging attests to this, showing money managers have decreased their bullish Brent and WTI long-only positions by 35,637 lots and total length fell by 19,748 lots to 500,704 in the week ending August 22, this is the lowest in 7-weeks.

None of this is particularly rally-worrying for products which are still dogged by refinery issues. Much of Friday’s rally and the recent bump in sentiment was derived from the news concerning a fire at Marathon’s Garyville site. Although the fire is now out, and probably the contributor to this morning’s slip in product prices, such incidents will remain catalysts in upward movement as the oil community is currently very sensitive to interruptions to any refinery, anywhere in the world. Keenly watched are weather outlooks in and surrounding the US Gulf. Hurricane season is truly upon us and if one of these poetically named ‘spinners’ finds landfall somewhere product-sensitive, bears will be blown away metaphorically and physically. Currently the National Hurricane Centre (NHC) is tracking tropical storm Idalia which is expected to become a hurricane at any time over the Eastern Gulf of Mexico.

There is little point labouring through the eternal battle that is macro versus oil derivatives, this week will see ample opportunity enough. There are great movers from data to come, namely China’s NBS Manufacturing PMI, European CPI, US GDP, PPI and Non-Farm Payrolls and those yet unseen. For bulls, plaudits must be heaped on the product suite for keeping the hounds of dissension to an oil rally at bay. Yet there is little reason to believe that fuels have burned their brightest, gas in its various guises is beginning to show up as a great accompanier to oil derivatives, none more than that which currently unfolds in the LNG market.

|

GMT +1 |

Country |

Today’s data |

Expectation |

|

15.00 |

US |

CB Consumer Confidence (AUG) |

116 |

LNG rides shotgun to oil product strength

It does seem that until the world gets to understand the true extent of finished product tightness after the refinery maintenance period is over, the oil market’s upside twitch remains ready to twang the complex higher after enduring and surviving the confidence battle brought on by any curve ball delivered at Jackson Hole last week.

Energy types and associated wires which have harboured bullish leanings are rightly pointing out that more of a deterioration in LNG supply will amplify any effect felt by a shortfall of distillate fuels particularly that in Europe. The thirst for Liquified Natural Gas remains unabated which was noted in last week’s EIA report on US exports which stood at an average of 11.6 billion cubic feet per day (Bcf/d) in the first six-months of 2023, 0.5 Bcf/d higher than the same period of last year and 1.0 Bcf/d higher than the 2022 average. The European Union plus the UK account for 7.7 Bcf/d (67%) in destination of US exports and is now higher by some 14% than the average of 2022.

According to the International Group of Liquefied Natural Gas Importers, EU/UK capacity to import will increase in 2024 by over one-third. Therefore, when a major source to market looks set to be disrupted by trade union unrest as it is in Australia at present, global gas markets that are called upon to contribute to a Europe still weening itself away from a heavy Russian reliance, begin to feel the upward pressure of buyers trying to prepare themselves for winter. Kpler predict Asian demand for LNG imports will amount to 23.92 million metric tonnes in August, up from 21.61 mmt in July meaning 2 continents competing for 1 commodity. It is worthy to note how forward in sentiment gas markets often trade as seen in last week’s extraordinary TTF swings when Woodside resolved its industrial dispute with Australian workers, because an unremarkable, benign winter will destroy such emotional buying but with that reality way in the distance, current thinking will keep gas markets buoyed.

Chevron have not managed to achieve a similar accord thrashed out by Woodside last week and its LNG workers have voted to strike at the Gorgon and Wheatsone plants as of September 7. If the strike ballot had been carried at Woodside as well, the reaction would have been somewhat more important, but it is nonetheless still concerning as Chevron’s facilities account for 5% of the world’s LNG production. The extent of strike or what type of industrial action is not quite clear, but having fulfilled its obligation in giving one week’s notice the union body of the Offshore Alliance does on the face of it appear to be engaging in more than just sabre rattling.

Freed from the handcuffs of influence from central bankers, well at least for a while, Australian industrial action supported by influences such as high temperatures in the US, a decrease in gas supplies from Norway into Europe because of maintenance at the Troll field (Reuters); power markets will run as a timely ally for a product-led oil rally.

Overnight Pricing

29 Aug 2023