Proverbial Animal Farm

The Efficient Market Hypothesis holds that asset prices reflect all available information at any given time. As a result, it is not possible to beat the market average on a risk-adjusted basis over the long term. Contrarians argue that temporary mispricing upends this theory, which does not take into account behavioural biases such as greed, fear, or herd behaviour. It was probably the temptation to lock in irresistibly attractive profits that prompted those who had the foresight to build up substantial length at the end of last week to sell in the early hours of Monday, even though tensions between Iran and its adversaries, the US, Israel, and several other Gulf countries, remained elevated throughout the day and are likely to remain so for the foreseeable future. Fears of protracted supply disruptions were visibly on display yesterday as prices continued their upward trajectory, with no de-escalation in sight, although some retracement, similar to the one on Monday, was observed toward the close of business.

History suggests that oil price spikes can fade quickly. In September 2019, when Iran targeted Saudi energy facilities, temporarily knocking out half of the Kingdom’s oil production, a weekend spike of around $9/bbl quickly ran out of steam. After Russia’s invasion of Ukraine, the panic rally lasted for less than two weeks. Last June, when the US Air Force and Navy attacked three Iranian nuclear facilities, the European crude oil benchmark advanced by slightly more than $10/bbl over the course of a week. After a telegraphed Iranian retaliation on a US military base, prices began to drift lower.

Does the latest black swan event appear different? One might conclude that the joint US–Israel attack on Iran, including the liquidation of the country’s supreme leader, was unforeseen and that the consequences are impossible to grasp. Up until last weekend, Iran was considered the elephant in the room; whether it has now been reduced to a lame duck is far from obvious. Its initial response to the US–Israeli attack, with missiles raining cats and dogs, is what is pushing oil and gas prices, freight rates, and shipping insurance premiums higher. Iran’s stance is understandably obstinate, yet it resembles the broadcasts from Iraq during the Second Gulf War, when the country’s defence minister defiantly announced that “We are in control” while US tanks appeared in the background. Iran will find it cumbersome to take the bull by the horns.

What it has managed to achieve so far is to kill two birds with one stone: inflicting considerable damage on oil infrastructure in neighbouring countries, thereby alienating them, and bringing traffic through the Strait of Hormuz to a virtual standstill. Iraq started to cut production as storage fills, and Saudi Arabia is contemplating rerouting its exports away from the Strait. Although uncertainty will prevail and investors will have butterflies in their stomachs every now and again, their views have been clearly expressed in price movements.

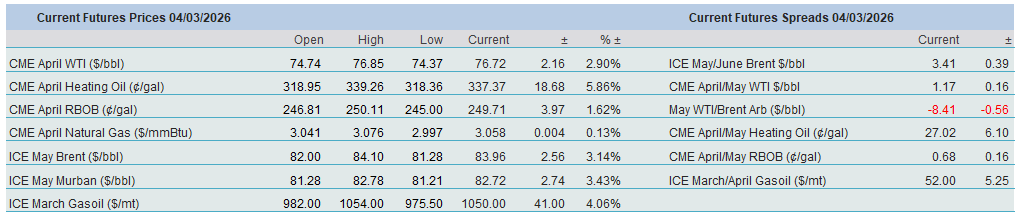

Shipping insurers are cancelling policies and raising the cost of cover by as much as 50%. VLCC rates from the Middle East to Asia reached a record high of $420,000 per day, LSEG data showed. The ongoing conflict has had the most profound impact on gas prices and distillates. The European TTF price for May delivery has jumped 68% since Friday. ICE Gasoil and the CME Heating Oil contracts rallied 34% and 23% over the past two trading sessions. Their respective differentials to Brent and WTI have risen by $21/bbl and $14/bbl.

The crisis has also had a tangible impact on crude differentials. Middle Eastern benchmarks such as Dubai, Murban, and Oman have registered record premiums. The M1/M7 Brent spread has tripled in value in three days, and the premium May Brent commands over May WTI has widened from $5.98/bbl to $7.85/bbl since last Friday.

The US and Israeli governments claim the attack on Iran was needed due to imminent threats, though details remain vague. Despite a gamut of conflicting official explanations, their overriding aim appears to be regime change. What shape or form that might take is anyone’s guess, and the repercussions remain unclear. Iran is an ethnically diverse country, and any attempt to introduce democracy could revive painful memories of Iraq and Libya. The US track record in removing autocratic regimes and securing peaceful transitions in the region is anything but pristine. Re-establishing order in the OPEC member state could prove to be like herding cats. Growing US casualties could trigger domestic backlash, particularly if the US President were to deploy ground troops to Iran. The economic impact of a prolonged conflict could also lead to rising inflation. Last Friday, one unit of the S&P 500 index bought 102 bbls of May WTI; by yesterday’s settlement, it was worth just 91 bbls. Overnight, the South Korean stock index has been pushed over the precipice, falling 12%. An energy shock leads to an economic shock.

The situation is fluid and changes by the minute. As long as Iran is willing and able to inflict damage on energy infrastructure and shipping lanes, the rally may prove as stubborn as a mule. The conflict is likely to drag on longer than last June’s military intervention, which had the lifespan of a mayfly. Yet there is little doubt that when the reversal comes, possibly in the form of a Truth Social post, it will be abrupt and brutal. It would trigger a spectacular turnaround in flat prices, time spreads, and crack spreads.

It is intriguing to note that the post-settlement Trump announcement of the US providing escort for tankers through the Strait has been ignored – apart from a sharp but brief sell-off. On the other hand, it is a tacit admission that the consequences of the invasion have not been fully thought through. A stock market rout and elevated energy prices will, further down the line, and together with possible domestic discontent about the war, force the US to make gradual concessions. The extent and timing of it remain murky. What is clear, however, is that until then, bulls are likely to remain the dominant force in price formation.

Overnight Pricing

04 Mar 2026