Reality Bites, Hard

Whether or not there is any truth to a story in ‘Axios’ overnight that the US is contemplating a fresh wave of airstrikes on Iran to break the current deadlock in negotiations remains to be seen. But oil prices need little encouragement to tempt them higher at present. After warning that the US blockade of Iran could run to many months, the US President is widely reported to have consulted the heads of major oil companies if there are any measures as to how any effect of a lasting closure of the Strait of Hormuz might be mitigated. The market can answer that for you Mr President, the answer is no, bearing in mind the eight-straight days of rally seen in Brent futures to achieve levels this morning not seen since March 2022, just after the outbreak of the Ukraine war. Admittedly, the front month in Brent is subject to exaggeration as it expires today, but $125 Brent, is $125 Brent. Donald Trump need not look further afield anymore as the state of the US market is beginning to represent how inventories around the world are depleting. The EIA showed crude stocks fell by 6.23mb, gasoline by 6.08mb and distillates by 4.49mb. The world is starting to pull on US crude as exports are now running at 39.9 percent higher than the 5-year average. Gasoline and heating oil stocks are 1.4 and 5.1 percent respectively lower using the same average and more worryingly, the implied demand in gasoline has not yet been affected by the summer driving season. For those who do not think Brent prices have the potential to reach $150/barrel, you ought to look away now.

It just became even more difficult

According to the ‘Oxford English Dictionary’, a cartel is a group of independent commercial or industrial enterprises that coordinate to fix prices, restrict output, and divide markets to increase profits and avoid competition. One wonders in the years to come how many members there will be left in OPEC and OPEC+ to coordinate. Tuesday’s news of the United Arab Emirates leaving the lobby of its 55-year history as a member of the group has not been totally unforeseen, what is, is the timing. The Emirate has been quietly grumbling on the disparity between its OPEC quota of 3.4mbpd and its capability of 5mbpd production, something achieved with a $150 billion investment. Such a surplus in production may not have mattered with crude at $60/barrel, but the opportunities at nigh on $120/barrel are self-explanatory.

An ally to Saudi Arabia within the Gulf of Cooperation Council and security issues particularly when dealing with Iran, the UAE has, however, taken a more competitive step with regard to encouraging investment from overseas and seeking export markets for more than just fossil fuel energy. According to ‘Gulf News’, since the issuance of the Commercial Companies Law in September 2021 until the end of 2025, the UAE has attracted nearly 760,000 new companies, bringing the total number of active companies to more than 1.4 million, a growth of 118.7 percent. ‘Free Zones’ have been a major attraction due to the tax environment and have seen trade in other sectors than energy such as technology, finance, logistics, media, healthcare and manufacturing. With such an entrepreneurial attitude in these sectors, the idea of being limited in what it can produce and sell from hydrocarbons is an anathema to its declared desire to bring the active company count to 2 million in the next decade, as predicted by Abdulla bin Touq Al Marri, Minister of Economy and Tourism, at the start of this year. Increased income from oil revenue will aid the high level of investment into energy transitions as the UAE is the leading player in the region of renewables such as solar power aligning to its ‘Energy Strategy 2050’, launched in 2017. The strategy has been subject to updates, nonetheless, many of the aims are still valid such as tripling the share of renewable energy by 2030, increase the contribution of clean energy generation by 2030 to 32 percent and the creation of 50,000 new green jobs by 2030 allowing for energy demand being met, and sustaining economic growth in the UAE. Using oil income to pay for energy transition and economic expansion cannot then be hindered by an antiquated quota.

Opportunity knocks then in the current Middle East war. Imagine if this announcement had been made before oil prices had taken to the skies. We might have been experiencing $50 Brent rather than our current inflated times. It is ultimately very bearish, but that reaction must be belayed until the current hiatus in oil movement is well and truly over. The heavy hand of the United States must be a contributing factor. Uncle Sam has never been shy of showing its antipathy toward OPEC and the current President has cried foul when accusing the group of “ripping off the world” which has had historic sympathy on Capitol Hill where the ‘NOPEC’ bill has seen a Congressional effort to address the issue that, under federal law, foreign governments cannot be sued for predatory pricing or failing to comply with federal antitrust laws and if ever passed would pave the way for legal action. If one allows for a conspiratorial track, then ponder on how the US has now had a hand in taking out Venezuela, Iran and the UAE as effective cartel members. Therefore, any extension of relationship between Washington and Dubai and an undermining of OPEC is a very useful tool for the current Administration as it attempts to assure the world that there is plenty of oil supply on the way. New economic ties announced last year is now suiting the strategic goals of both. The $440 billion pledged by the UAE into US oil infrastructure up and until 2035 is answered by US oil companies expanding operations in the Emirate and a deal that will give the UAE access to some of the most advanced artificial intelligence semiconductors from US companies, a major boost for Abu Dhabi's efforts to become a global AI hub.

Howsoever one looks at this cessation from OPEC by the UAE, it is a knife to the heart of the producer group. The loss of such a member, and its fourth largest producer, will now not only question the commitment of others to keep the group together but also its effectiveness as a cartel in managing global supplies. Disparaging as one might be toward OPEC, it has been a unifier in a geography sadly lacking in any cohesion. It is hard not to envisage a long and slow erosion of the Organisation of the Petroleum Exporting Countries, but one of the side-effects of a break up will be how oil custom competition will increase geopolitical tension and far from making the future of oil supply from the Middle East more stable, this reshaping of alliances and OPEC will cough up even more points of contention and possible conflict.

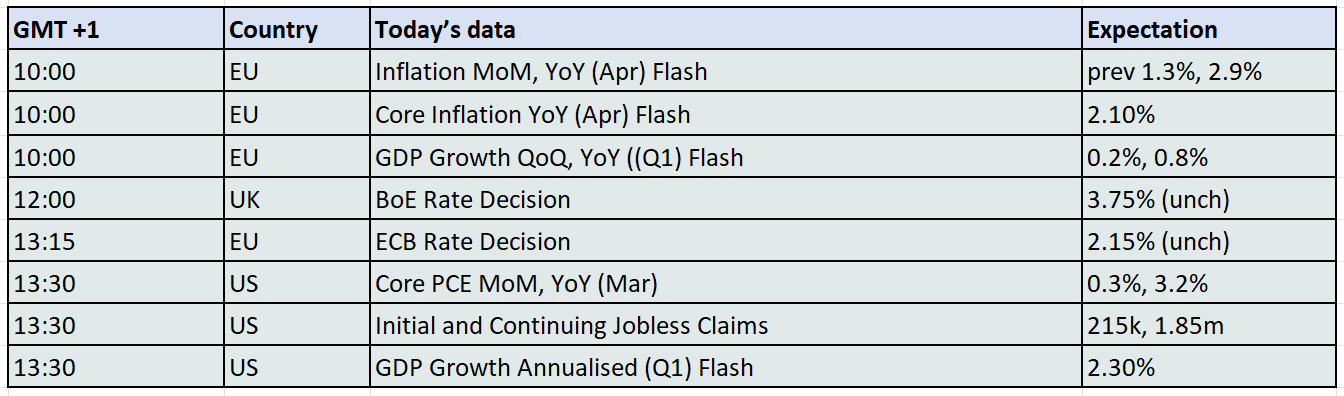

Overnight Pricing

30 Apr 2026