Reality Fails to Check in

Once again, oil and equities yo-yoed and danced to the tune of the narrative surrounding the Persian Gulf. And what a vibrant day it was. Wednesday’s sell-off in oil continued into the early hours of yesterday’s session after the US President confidently announced that negotiations with Iran were in their final stages. A sharp reversal was triggered after Reuters reported that the Iranian Supreme Leader had issued a directive stating that the country’s near-weapons-grade uranium must not be sent abroad, one of the key demands of the US. Then again, news of a draft agreement between the two countries produced yet another handbrake turn, sending oil $6/bbl lower within the space of three hours.

All the while, following the sharp decline in US oil stockpiles reported by the EIA on Wednesday, Goldman Sachs warned that global inventories are being depleted at a record pace, while the head of the IEA said that stockpiles will fall below critical levels by July or August if oil does not start flowing through the Strait of Hormuz soon. Clearly, the market wants to believe that it will. Yet, should explicit signs emerge to the contrary, another spectacular change of heart could easily send prices back where they came from. For now, the consensus is that the gaps have narrowed (Iran), and there are ‘some good signs’ in talks (Marco Rubio), but oil has not started flowing, setting a floor of around $96 basis Brent, and $90 on WTI.

Finite AI Support for Equities

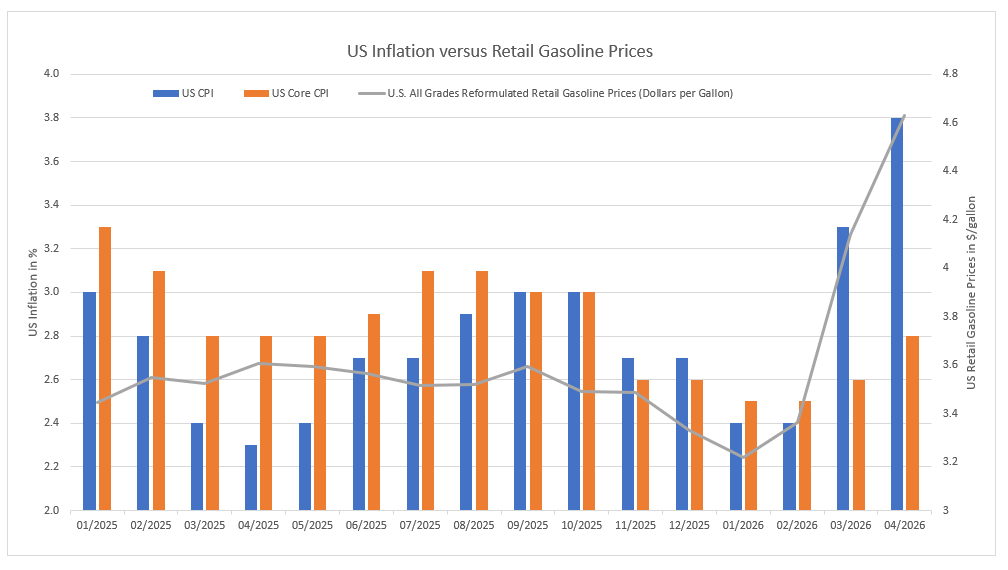

Whatever the US President pledged during his campaign in the run-up to the 2024 elections needs re-evaluation. The self-declared ‘President of Peace’, who promised not to start wars but to stop them, has been waging a conflict against Iran for nearly three months now. He vowed to defeat inflation quickly, make America affordable again, and bring down the prices of all goods. The annual increase in US consumer prices has jumped from 2.3% in March 2025 to 3.8% last month. He also envisaged $2/gallon gasoline prices at the pump. Instead, they are worryingly close to $5/gallon.

In a way, it is a package deal, deftly summed up in the chart below. Although the US has become an inward-looking nation that believes protecting its own interests can be achieved through confrontation rather than co-operation, the global consequences of impulsive and ineffective foreign policy have been laid bare by the Persian Gulf crisis. Had he chosen to deprive Iran of its nuclear capabilities through negotiations, similar to those pursued by his Democratic adversary, Barack Obama, it is fair to say that inflation, and with it gasoline prices, would be significantly lower.

He did not, however, and the repercussions of that decision are strikingly visible in the graph. The rise in the cost of goods in the US is the steepest in three years, while pump prices are the highest since the immediate aftermath of Russia’s invasion of Ukraine. Elevated forecourt prices are driving inflation higher, and when inflation exceeds wage growth, the economic outlook turns grim. An unmistakable sign of looming hardship is the worrying surge in US bond yields. This could force the Cerberuses of US monetary policy to raise borrowing costs, which would undoubtedly provoke outrage in the White House.

Of course, once the crisis is over and the Strait of Hormuz reopens, the status quo may eventually be restored, allowing the economic manna to be enjoyed by all, not just the privileged few. Yet such a scenario appears implausible in the near term. First, it will take months rather than weeks for the global oil supply to return to its pre-crisis norm. Consequently, US gasoline prices, already facing an exceptionally tight summer market marked by severely depleted commercial inventories, are likely to remain elevated. Given that gasoline is a heavily weighted component of the consumer price index, headline inflation will probably stay uncomfortably high. Worse still, core inflation, which excludes food and energy prices, tends to follow rises in gasoline prices and headline inflation with a two-month lag. Consumer and producer prices are therefore likely to continue rising for the foreseeable future.

The US President is confident that his beloved country is the hottest in the world. If he means the inflation outlook, he may well be correct. Despite these gloomy prospects, however, the US equity market continues to perform remarkably well. As aptly described in yesterday’s note, this optimism stems largely from unbroken faith in the AI sector. Yet that support will not last indefinitely. Persistently expensive gasoline, elevated inflation and rising bond yields are likely to trigger further interest rate increases. That may well be the moment when support from AI begins to wane, while oil remains comparatively stable. After all, it is an attractive hedge against inflation.

Since the start of the current conflict, oil prices have risen more than equities. At the end of February, one unit of the Nasdaq Composite Index could buy 350 barrels of WTI crude. Although the stock market has remained resilient, that ratio has now fallen to 270. If inflation persists and interest rates continue to rise, the narrowing of this quotient is likely to continue.

Overnight Pricing

22 May 2026