Russian Cracks

Although traffic through the Strait of Hormuz came to a virtual standstill yesterday following the latest flare-up in hostilities between Iran and the US, oil investors remained admirably relaxed, or even nonchalant, about the situation. On the other hand, they are clearly worried, though not about supply disruptions but about demand destruction. Reciprocal strikes, precipitated by the dispute over control of the Strait of Hormuz, failed to provide sustained price support, with WTI and Brent settling around 2% lower on the day. Instead, sentiment was shaped by the Fed minutes, which revealed deep concerns about inflation, potentially leading to higher interest rates, the classic anathema to advocates of demand growth.

While one geopolitical hotspot is failing to provide meaningful support, another is undeniably lurking in the background: the price differential between refined products and crude oil has been skyrocketing. Despite yesterday's comparatively sharp decline in distillate and gasoline prices, the premiums they command over WTI and Brent remain eye-watering: $78 and $55 per barrel for CME Heating Oil and RBOB, respectively, and $63 for ICE Gasoil. The Ukrainian strikes on Russian oil installations have been so effective that one of the world's largest exporters of refined products has been forced to ban diesel exports, depriving itself of precious wartime revenue. It has even been compelled to rely on foreign supplies to satisfy domestic demand and suppress growing public discontent. It is nothing short of ironic that Russia has actually beaten Europe in weaning itself off, well, Russian oil.

Russia is losing its war against Ukraine, but while the market does not anticipate a severe escalation in the Persian Gulf, reality could prove very different in Eastern Europe. And if, at some stage, Vladimir Putin has to go, he will not go quietly.

Not As Loose As It Appears

While the latest developments in the Persian Gulf might be described as concerning, they are far from explosive. The trigger was the control of the shipping route: which side of the Strait should vessels transit the chokepoint? As banal as this excuse is, it undeniably caused temporary anxiety among investors, as reflected in a nearly $10/bbl jump in prices on Tuesday and Wednesday. Common sense dictates that neither party is incentivised to pursue further escalation. Iran needs the revenue from exporting its crude oil, while the US administration could certainly do without recurring inflationary pressure ahead of the midterm elections, now a mere four months away. But do we rely on common sense when an autocratic regime fighting for survival and a democratically elected, but mercurial and untamed leader stares at one another?

Prices retreated yesterday, and let us assume that nerves will calm further. The question then is whether the downtrend will resume and those predicting sub-$70 Brent prices will be proven correct. It is hopefully useful to take another look at the monthly EIA outlook released on Tuesday to see how the balance is expected to evolve until the end of the year and even beyond. Furthermore, taking a step back and looking at the broader picture could also prove revealing.

Given the huge amount of uncertainty surrounding the supply, production and exports of black gold, every analysis must begin with assumptions. The EIA's are as follows: with the signing of the Memorandum of Understanding between Iran and the US, traffic through the Strait of Hormuz increases, inherently leading to a significant reduction in the supply deficit during the current quarter and a sizeable stock build in the fourth quarter, which will accelerate throughout 2027. The monthly balance is projected to swing by 5.10 mbpd in the second half of 2026 and by 1.04 mbpd in 2027.

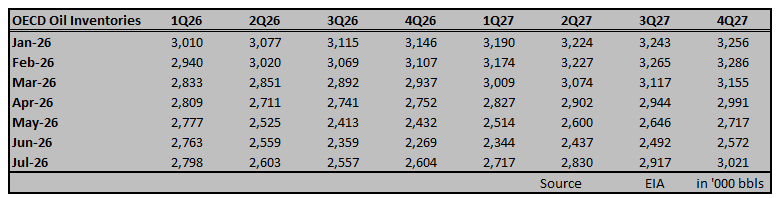

It is a robust but intelligible change in the EIA's assessment of the chasm between global supply and demand, one that foretells an abundance of oil and, consequently, persistent downward pressure on prices. The picture differs, however, when viewed from another angle by comparing the pre-conflict outlook with the current snapshot provided by the EIA. Take a look at the table below.

When the hostilities began in early March and intensified in April, perceived and actual supply disruptions forced the EIA to markedly reduce its OECD stock estimates by more than 700 million bbls between February and June for the third and fourth quarters of the year, as well as for end-2027. Based on the latest assumptions described above, there has been an understandable and justified upward revision to OECD oil inventory projections for the coming 18 months from June to July: 198 million bbls for the third quarter, 335 million bbls for the fourth quarter and 449 million bbls for end-2027.

What is noticeable, nonetheless, is that these new projections remain meaningfully below the pre-crisis stock estimates. While the EIA expects global oil production to rise faster than previously thought, resulting in the market shifting back to its pre-conflict state of oversupply in 2027, OECD inventories are still bound to remain beneath the levels projected in February.

The purpose of this exercise is not to present an unconditionally bullish backdrop, but rather to point out that the EIA anticipates a tighter market in the future than it did in February. This view is reflected in its Brent price forecast. For the whole of 2026, the EIA now expects Brent to average $82/bbl—or $77/bbl for the remainder of the year, given the year-to-date average price of $87/bbl—up from its February forecast of $58/bbl. For next year, the prognosis stands at $65/bbl, $11/bbl higher than five months ago but still well below the current forward curve. The key takeaway is that, while no substantial price increase is envisaged, the market may have found its floor, at least based on the EIA findings. These price projections will prove too conservative only if all hell breaks loose in the unpredictable Middle East.

Overnight Pricing

10 Jul 2026