Russian Supply Concerns Ease, Fed Under Siege

One can only guess why oil prices dropped relatively sharply while equities, bonds, and the dollar remained comparatively stable yesterday. After all, Ukraine last week launched one of its most effective drone campaigns against Russian refineries, significantly damaging the country’s ability to churn out products. As a result, Russia announced an increase in crude oil exports, which naturally implies reduced product sales to willing importers, as the priority is currently ensuring adequate domestic supply.

Two possible explanations for the abrupt halt of a four-day winning streak originate from the US. European officials, citing talks with their US counterparts, said that Washington is willing to provide air and intelligence support for Ukraine, enabling European ground troops to shield the country from further atrocities. Of course, a peace deal is a necessary precondition for such support, and it remains elusive. Even so, the prospect of tentative US involvement seemed sufficient to push potential sanctions to the back of investors’ minds, prompting some profit-taking and sending oil prices, particularly Heating Oil, lower. Further pressure came from the restart of BP’s Whiting, Indiana refinery, although full production is not expected until after next week, according to IIR. The overnight API report, which showed drawdowns in US oil stocks across the board, helps prices stabilise this morning.

The relentless assault on the US central bank continued yesterday, as the President fired, whether successfully or not remains to be seen, one of its governors. This represents a serious attack on the independence of one of the most important and trusted US institutions, yet market reaction was counterintuitive. Equities and bonds strengthened, and the dollar edged slightly lower. The alleged subterfuge for the dismissal (the governor supposedly falsified her mortgage statement) is irrelevant. What matters is that the Administration appears determined to seize control of monetary policy and push rates lower as quickly as possible, regardless of economic justification. Premature cuts will only rekindle inflationary pressures, to the detriment of growth. It is a reckless strategy, the long-term consequences of which will be anything but constructive.

High Production, High Independence, High Leverage

To say that the US oil industry has undergone a spectacular transformation over the past 10–15 years is a massive understatement. Its impact is felt in almost every corner of the world, for better or worse. The shift began with the groundbreaking technology of hydraulic fracturing. The term itself provides a strong clue: oil and gas are extracted by drilling deep horizontal wells, injecting water, sand, and chemicals to create fractures. When sand props these fractures open, trapped oil and gas are released.

The impact of this technology is there for everyone to see. The US pumped 5 mbpd of crude oil in 2008. It compares to a Saudi output level of 9.11 mbpd or a Russian one of around 9.65 mbpd of the time. Then the ascent started. US production reached 6.5 mbpd by 2012, broke the 10 mbpd barrier in 2018, and the inevitable pandemic-induced dip was followed by a more than impressive bounce to 13.44, year-to-date, weekly EIA data shows. Both Saudi and Russian oil production is decisively under the 10 mbpd mark, making the US not just the biggest oil consumer but also the producer in the world.

On the way up to these record levels, at the end of 2015, President Barack Obama lifted the export ban on crude oil shipments, introduced in 1975 because of the Arab oil embargo. The repeal of the ban not only reshaped the domestic oil landscape but also significantly altered international oil flows.

Net crude oil imports have since collapsed. Before 2010, the US relied on almost 11 mbpd of foreign crude to cover its ~20 mbpd domestic demand, which has remained largely flat. With exports virtually nonexistent at the time, gross imports nearly matched the net volume. From 2015 onward, however, crude oil exports surged. A decade ago, only about 500,000 bpd left US shores; by 2025, the figure has risen above 4 mbpd, helped by the inclusion of WTI Midland in the Brent basket, the most important crude oil benchmark. While refiners still import significant volumes to offset quality mismatches, the thirst for overseas crude oil has fallen from 11 mbpd in 2008 to just 6.3 mbpd today.

The composition of crude oil importers has also gone through drastic changes. Former partners and allies are fading in significance, and new ones are relied upon. Crude oil shipments from the Persian Gulf have dropped from over 2 mbpd in 2008 to below 500,000 bpd in 2025, whilst total OPEC exports to the US have declined from 5.4 mbpd to 900,000 bpd in these 17 years. The explosion in Canadian oil sands production, on the other hand, helped the US’s northern neighbour to more than double its exports to above 4 mbpd. It explains the hardened US stance towards Iran or its belligerent rhetoric towards Russia, which soon might be backed up by action.

Soaring production and stagnant consumption have given the US full independence from foreign oil, as reflected in net combined crude and product exports. In 2005, the US imported 12.5 mbpd; by 2025, it has become a net exporter of over 2 mbpd.

In fact, it is impossible not to notice the long-term reverse relationship between crude oil production and net exports. Since 1990, it stands at -98% meaning the higher the crude oil output, the lower the net exports and vice versa. In the immediate aftermath of the Covid-19 pandemic, the obituaries of the US shale industry had been written, yet the sector proved remarkably resilient. Although the latest OPEC attempt to regain market share does no favour for US producers to fulfil the unreasonable central directive of raising output by 3 mbpd during the incumbent’s term and domestic output might even plateau or even decline some in the coming years, unless there is a meaningful retreat, combined export will remain elevated, independence on foreign oil intact and foreign policy hawkish.

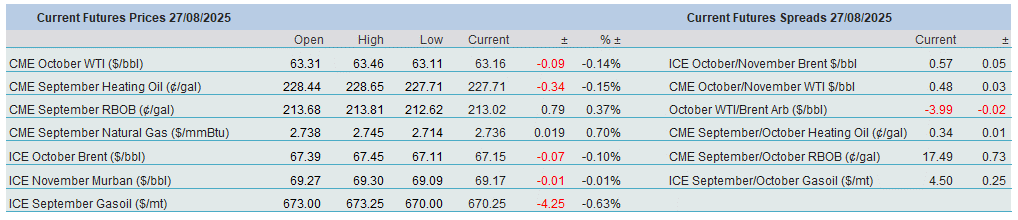

Overnight Pricing

27 Aug 2025