Sanctions and the Weather Bring Relief, But for How Long?

Oil prices along with many other classes of risk are entering a phase of guessing. The metals tariffs announced by the White House yesterday brings an idea that even though Canada and Mexico are enjoying a one month stay of hand from trade restrictions, this notion that tariffs are transactional threats has just been dented. There are no exemptions on the rate applied to steel and aluminium, therefore, the threat to imports of crude into the US have become very real again.

With the US bearing down on Iranian exports and sanctions still biting into Russian flows, Asian crude grades remain firm and underpin the rally from yesterday. The fate of Russia’s oil industry is in the news again, an ANZ Bank report seen on Reuters estimates Russian oil production is now under its OPEC+ quota being below 9mbpd. In addition, and according to Politico, European countries are holding behind-the-scenes talks on large-scale seizures of Moscow’s oil-exporting tankers in the Baltic Sea.

Sanctions and the pursuit of more are not the only positive driver in the oil space. Cold weather continues to encourage Gas prices higher. According to Bloomberg research, European Gas prices are at $100/barrel equivalent and will encourage power plant ‘switching’ to Fuel Oil and Gasoil. While FGE expects the amount to be of no great significance yet, a likely coinciding situation in Asia where buyers of LNG compete with European customers, might just see an increase in alternative oil burning.

At some stage any rally in oil prices will run into the smothering tariff spectre, it will also have to consider a world that is setting itself for a continued stronger US Dollar. The Fed Chair, Jerome Powell, is due to speak on Capitol Hill today and tomorrow, his testimonies will be eagerly awaited. As ever, the market prices before him and with tariffs deemed inflationary by majority of thinking, Powell’s language is expected to be neutral to hawkish. A Reuters poll of economists sees agreement in the main that there will not be US rate cut until the next quarter. The CME FedWatch Tool predicts a 93.5% chance of no change at the March FOMC meeting and a 73.2% chance of a similar hold in May. Such news is meat and drink to Dollar bulls, but a worry for many other assets including oil.

No getting away from them

All countries, their economies, markets and investment suites are unable to avoid being framed by tariffs. It would obviously make things easier if the framing had firm borders but at present, one day might see a tapestry-size consideration, with every colour of trade in the image; the next a miniature, precise and intricate in design. An interesting prospect is the fluidity of reaction. Currently, there is knee-jerking aplenty in markets, the major investment areas swing, opportunities are welcome or not in equal proportion, and all remains unpredictable. However, it could be argued that immunity is being built. All market fraternities are cynical, a transactional Trump can be seen coming from a distance and as in the Aesop fable in which the boy cries ‘wolf!’ too many times, so is the perception of Trump when he bellows ‘tariff!’.

The pointed end of global trade, in which trading arenas reside, shudder and judder but invariably end up at the place where buyers and sellers meet to strike a price. Reaction is quick, strategy is short-term, day trading increases and each day the vernacular of tariffs is absorbed and in the main, planned for. Risk is the daily pattern, drivers that once moved hearts and minds become also-ran and one only needs look at the immunity eventually felt by oil prices after months and months of feared conflict spread in the Middle East as example. All well and good then, trading medium will fulfil their roles as a place of price discovery and although price prediction remains foolhardy, price reaction management is not, volatility becomes built in.

However, markets are supposed to represent an underlying asset. Particularly commodity markets or those having tangibility. Volatility might be a breeze for those that manage market risk, but it certainly is not for underlying industry, its energy, its source of base supply, the mode in which it arrives and final destination customers. The announcement over the weekend of the US imposing a 25% tariff on all steel imports has sent a veritable shiver through its trading partners. The Guardian and others report in South Korea, the industry ministry saying on Monday that it held an emergency meeting with steelmakers in Seoul to discuss measures to minimise the impact of potential tariffs. Shares in Hyundai Steel, the country’s oldest steelmaking company, fell as much as 2.9% on Monday. Similar conversations will be underway in Mexico, Canada, Brazil and Vietnam, the other main sources of the building metal. The double-edged sword will cause supply and inflationary issues for US car makers, builders and heavy industry involved with international steel. There is also an opinion on wires involving drilling rigs and platforms for the oil industry being affected, and thus production.

Steel is the headliner of the week, but tariffs will be excised on all manner of commodities and produce. The economies of the US’s trading partners are now running in fear of tariffs. Slower growth and overcapacity are easily anticipated leading to lower demand, investment and economic confidence. The European Union may be loading a gun of retaliation if it becomes subject to tariffs, but it will not help an already financially beleaguered economy. Retribution is also a Donald Trump trait. His pursuit of political enemies at home has been headline grabbing, therefore international revenge is almost guaranteed. The WSJ is of similar opinion and debates how the EU is in the firing line because of taxes, regulations and penalties they have imposed on U.S. tech companies such as Alphabet’s Google.

The tariff drip into the cavern of international trade is forming stalactites of impediment. Indeed, while reaction in front-end trading markets is swift and as observed become manageable, the process into the global everyday will take more time and last much longer. The greatest driver in any market is sentiment. The suppressing nature of tariffs, whoever imposes them, is about to have great influence on the socio-economic behaviour of the peoples of the world. It is way too brave in hyperbole to compare a downturn with that of the pandemic, the extent and longevity of tariffs are as easily guessed as which country might become the next 51st state fancy. Yet, damage is being done already. If nation states are taking up defensive trade posturing, then citizens will not be far behind. Investments suites might be adroit, but spending and investing from ordinary Joes and Josephines is not and that lag and drag will eventually make it to risk assets, their prices and behaviour.

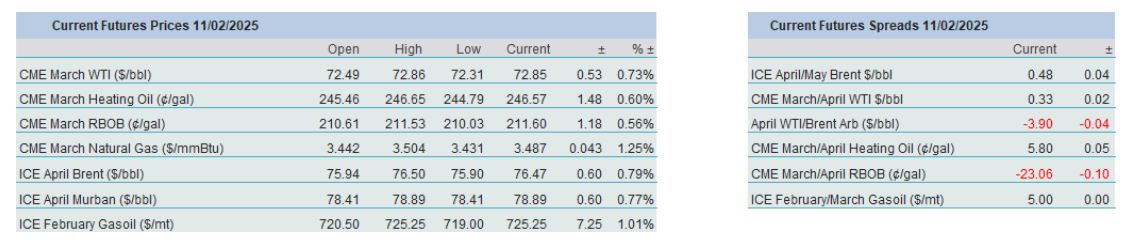

Overnight Pricing

11 Feb 2025