Sanctions Fizz is Being Flattened by China in a Huge Data Week

Oil prices are still enjoying the wash of last week's very decent performance as the notion of initial tighter supplies from Russia due to sanctions introduced by the European Union and the likely joining of them from the US which itself, under a Donald Trump tutelage, will be far more hawkish toward Iran. The main futures contracts in their M1 contracts finished the week; WTI +$4.09/barrel (+6.09%), Brent +$3.37/barrel (+4.74%), Heating Oil +13.74c/gallon (+6.44%), RBOB +9.56c/gallon (+5.02%) and Gasoil +$41.50/tonne (+6.41%). Playing as bullish running mates were the political and military vacuum seen in Syria after the fall of the Assad regime and the start of a season in which a series of central bank interest rates will see cuts. With all contracts making new monthly highs, those of technical bent will be keen to see if this week will see if the rally can be built upon to take prices beyond some key resistance areas.

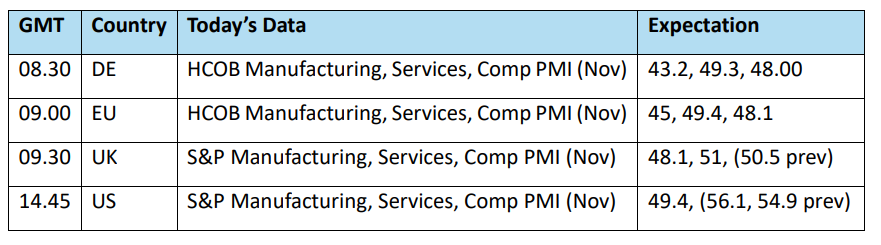

There are due an inordinate amount of data sets, kicking off today with global PMIs, but the pick of the bunch will be the US FOMC interest rate decision on Wednesday, which according to pricing on the CME FedWatch tool is a lock at a 25-basis point reduction. Whether or not that is enough to instil more confidence in oil prices or, as discussed below, not enough to dent the high-flying, and potentially asset-smothering US Dollar makes for great anticipation. Oil eyes can never be averted too long from China and this morning's data is mixed at best. Although the House Price Index fell slightly less than in October and Industrial Production came in a pip better than forecast, Retail Sales at 3% was not only below the 4.6% expectation but much worse than October's 4.8% and whatever stimulus is being deployed, consumers are not buying into it and without a serious sea-change in personal spending behaviour, China's economic fortunes will be stunted. Running along with more China warnings was the outlook from CNPC on Friday in which it saw peak consumption in 2023, a 1.3% fall in 2024 and much less need for transport fuel in the future.

The US Dollar, again and again

It feels as if time and again our eyes will return to the strength of the US Dollar. It is unavoidable. The US markets have carved a path of exceptionalism in global performance and King Dollar is more than geared up to join in the ride. For the moment, gone are the times when risk on would lead to a shallowing performance and risk off mean a greenback rally. Good or bad news seems to cheer the dollar because a decent performing American economy makes its currency attractive and when there are hiccups, the potential toys that maybe deployed against such situations are either supportive, or if indeed negative, are very short-lived.

There can be little doubt that the US Federal Reserve will do anything other than follow through on its 25-basis point rate cut this week. However, there has been a lot of comments from Fed members that revolve around being a little less dovish. Recently, its Chair, Jerome Powell, observed that there needs not be a hurry to lower rates due to the economic circumstances in the US. But the ‘circumstances’ must entail a nod toward what the new Donald Trump administration’s financial path might be. The President-Elect has been verbose on tax cuts, tariffs and spending which are a trifecta of inflation stimulation.

In a very troubled world, and during instances of increased geopolitical strife, the US Dollar remains the go to safe haven. It is almost self-fulfilling. The exceptionalism means the US investment suite attracts a vast amount of overseas investors which also drives the US Dollar. When those investors fly to a safe haven, it is to the very same currency that they have helped by populating the US financial markets with spikes occurring from an elevated level.

The end of last week saw another surge in the US Dollar Index (DXY) as three of the currencies in its constituent six fell away due to central bank decisions. The European Central Bank (ECB) cut rates by 25-basis points, the Swiss National Bank (SNB) and Bank of Canada (Boc) by 50-basis points each, signposting differing attitudes in aggression for monetary easing. Whether or not the aggressive cuts by the SNB and BoC are pre-emptive due to US sanction fear is arguable, but Canada and Europe have been named as targets for punitive trade restrictions by Donald Trump. Europe in particular is vulnerable; exports make up a goodly part of GDP and any loss of export markets can only increase the pressure on what is a rather bleak outlook for the continent's near-future. As for the Bank of Japan, it does not seem ready to raise rates and will probably see how tariffs unfold. The likely outcome to do nothing will again encourage its fall as a forex paring.

Cutting of interest rates, or currency devaluation maybe the only tool in the box for some central banks, which only exacerbates the rise of the dollar. Indeed, there has been recent speculation involving how the People’s Bank of China might allow the Yuan to devalue, in possible response to tariffs. Deviation in the US interest rate path compared with elsewhere attracts investors into US bonds as yields rise and financial thermals will continue on which the American currency will soar.

Higher yields, interest rates and the world's banking currency will eventually adversely affect all types of investments from stock markets to commodities or anything that prices in or is linked to the word's currency marker. From now and in the foreseeable future, the prudent thing is to look first toward one’s investment choice, but quickly back that glance up with the fortunes of King Dollar, its rise in price is commensurate to influence.

Overnight Pricing

16 Dec 2024