Sanguine Markets

The Fed is worried. In its latest semi-annual Financial Stability Report, issued last Friday, it admonished investors about the risks the ongoing Iranian crisis poses to the smooth functioning of the economy. The main tenets of the publication are the risks to inflation and growth stemming from the Middle East conflict and the oil shock. A protracted conflict in the Persian Gulf and dysfunctional commodity supply chains could adversely impact the global and US economic outlook, while volatile price movements in energy and related financial products might lead to market strains. There are also growing concerns about stretched asset valuations and debt-funded AI investments. Across the five major categories- geopolitical risks, oil shock, AI, private credit and persistent inflation- the share of respondents who perceive elevated risk has increased substantially since last November.

No doubt equity investors acknowledge these risks and keep a close eye on them; however, stock market performance does not indicate that the danger of a worldwide economic fallout is deemed imminent. The MSCI All-Country Index gained 2.38% last week, the S&P 500 index matched its performance, and the Nasdaq Composite Index bettered it, returning 4.5 cents on every dollar invested the preceding Friday. The relentless march higher can be explained by solid, albeit downwardly revised, growth forecasts, stellar earnings reports from the majority of S&P 500 companies, a seemingly robust US labour market and, of course, unbroken faith in the growth potential of the technology sector, specifically Artificial Intelligence.

As convincing as the stock market rally appears, it is worth noting that this buoyancy is largely driven by a handful of tech companies. As pointed out by the Financial Times, half of the 12% gain in the S&P 500 Index since the beginning of April came from five tech giants: Alphabet, Nvidia, Amazon, Broadcom and Apple. It might serve as a warning signal that equities are more exposed to sharp corrections than at any time in the past, although the timing remains dubious (and, of course, in trading and investment, timing is everything). Add to that US consumer sentiment, which reached a historic nadir in April, and the re-ignited threat of tariff wars as the US warns of fresh punitive measures against the EU and China, and one can only begin to wonder when the nasty correction will start.

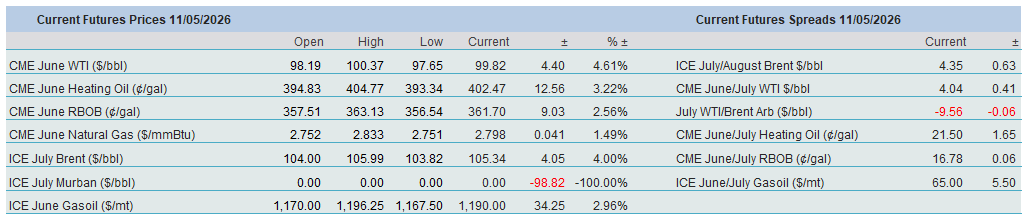

It is not impending, as equities imply, and oil agrees. Despite the absence of a ceasefire and the continued closure of the Strait of Hormuz, preventing 10–13 mbpd of crude oil and refined products from reaching international markets, oil prices drifted lower last week. The two major crude oil benchmarks lost more than 6% over the week. The M1/M7 WTI spread fell by $6.36/bbl and its European counterpart by $6.96/bbl. Global oil inventories are declining markedly, and several analysts warn that the situation could become critical by next month.

Negotiations between the US and Iran are stalling, notwithstanding the US administration’s claim that the ceasefire remained in place last week, although there were regular attacks on ships around the Strait. Maritime security incidents continued, US forces reportedly prevented 70 tankers from accessing Iranian ports following the implementation of the blockade, and the US struck Iranian targets on May 7 after accusing Iran of attacking US vessels. The week ended with neither a full reopening nor a complete shutdown of Hormuz. The situation resembles an unstable armed stand-off: diplomatic channels remain open, but commercial shipping is still constrained, military assets are building up on both sides, and any isolated incident could quickly escalate into a broader confrontation.

No Love Found between the US and Iran

As matters stand, the end of the Iranian hostilities is nowhere in sight. That much has been implicitly acknowledged by the warring parties, as a comprehensive peace deal remains more elusive than ever, and both the US and Iran appear to be seeking a limited pact: a truce or armistice that would defer discussions on the salient issues. It is worth recalling the original US objectives at the outset of the war. These included removing the Iranian regime, destroying its ballistic missile capability, preventing it from obtaining nuclear weapons, neutralising its naval capacity and weakening its regional proxy network.

Clearly, these targets will not be achieved in the foreseeable future. The infamous one-page document presented by the US to Iran, which was intended to serve as the basis for truce talks, reportedly called for an immediate cessation of hostilities between the US/Israel and Iran. It proposed a 30-day ceasefire and negotiation window during which a permanent settlement could be worked out, alongside the gradual reopening of the Strait of Hormuz. Iran’s shipping restrictions and the US naval blockade would be lifted incrementally. Iran’s nuclear programme would be limited in exchange for US sanctions relief, including the lifting of primary and secondary sanctions and the unfreezing of Iranian assets. The major point of contention remains the moratorium on Iranian uranium enrichment (the market estimate is allegedly a five-year bid from Iran versus a 20-year offer from the US). Other potential sources of disagreement include Iran’s enrichment capability and control of the Strait of Hormuz.

The Iranian answer arrived yesterday. Just by looking at oil prices this morning, it is painfully clear what it was. It included Iranian demand for war reparations and control over the Strait. It is a nonstarter for the US or, in the words of President Trump: ‘I don’t like it – TOTALLY UNACCEPTABLE’. Iran clearly believes that time is on their side. We will find out soon enough whether the forthcoming US-China summit will change this attitude. US concessions regarding Taiwan might nudge China toward pressing Iran to reopen the Strait. Conversely, excessive Chinese demands on trade and AI could alienate the US President and lead to renewed escalation in the conflict. This geopolitical chessboard contains far more than 64 squares.

Overnight Pricing

11 May 2026