Saying Nothing is Sometimes the Best Policy

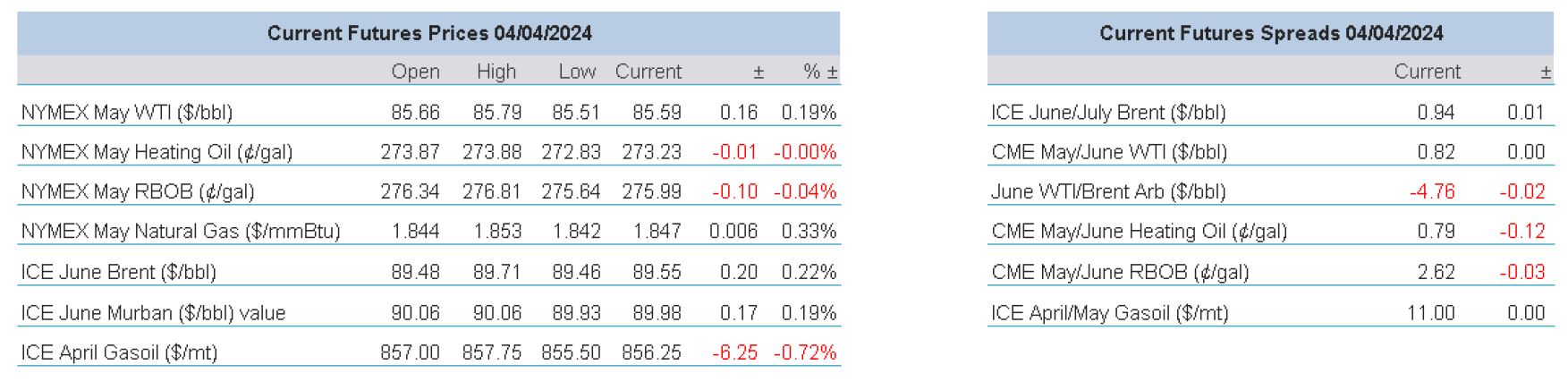

Oil prices retain a positive bias and it would have been a woeful performance from those that gathered at the OPEC JMMC if any intimation of increased supply from members had been uttered. As it stands, the market seems to accept the ill-discipline from Iraq and Russia as to quota adherence will eventually be sorted out, and instead concentrated on how current cuts will roll on through June. Confidence in its current policy from OPEC can be seen on how the next JMMC will coincide with the full ministerial meeting on June 1 removing any doubt that a trimming of cuts might occur in the near future to upset oil’s gathering bulls.

Even the increase in crude oil stocks from the EIA Inventory Report created only a brief hiatus in proceedings as it is easily explained away by reduced refinery runs of 35kbpd and that utilisation diminished by 0.1%. However, because of the focus on Gasoline and products in general due to the Ukraine drone damage at Russian refineries, the draw of 4,256mb against an expectation of -800kb and API draw of -1.5mb, keeps the emotive motor fuel front and centre particularly for US markets and with the added bonus for bulls of a draw in Distillate of 1.268mb, the Crude build served as a dampener rather than an out-and-out ceiling.

The other major feature of yesterday was the awaited speech by the US FED Chair Jerome Powell at Stanford University. In a performance which offered little other than a status-quo, similar to the JMMC, Powell deployed repetitious language on maintaining a balance between economic growth and inflation and that current markers will keep the FED prudent but still open to an interest rate cut in 2024. Later, fellow FED member Raphael Bostic took an altogether much more hawkish line by offering his view that there might only be one 25-basis point cut this year and not until the fourth quarter. The price of oil must be in the minds of such lofty banking folk, cutting interest rates into a rallying oil market would be akin to self-harm. The battle to tame inflation will continue to be a hard-fought grind, and bottle-neck price increases are again prevalent in oil prices as seen by the crimping of Russian refined products available to market which is one of the reasons why central bankers will talk appeasement but continue to deliver no interest rate relief, which is expanded on below.

GMT+1 | Country | Today’s Data | Expectation |

09.00 | FR, DE, EU | HCOB Services PMI Final (Mar) | 47.8, 49.8, 51.1 |

09.00 | FR, DE, EU | HCOB Composite PMI Final (Mar) | 47.7, 47.4, 49.9 |

09.30 | UK | S&P Global Services, Composite PMI Final (Mar) | 53.4, 52.9 |

12.30 | EU | ECB Minutes (Mar) |

|

13.30 | US | Initial and Continuing Jobless Claims | 214k, 1.813m |

If you think inflation is over, think again

The full extent of the 7.4-magnitude earthquake that struck Taiwan will not be known for some days yet in terms of any human tragedy. However, what will take much longer as an aftermath effect of the most violent quake for 25 years is what it might mean for world inflation. Even though it is accepted as a manufacturing hub, the loss of Taiwan as an importer is not exactly market shattering. Imports valued at $23 billion in February do not compare well with China mainland’s $180 billion, therefore, the world will not have an untoward amount of goods without a home. The issue will be exports, but exports of a specialist kind. Taiwan Semiconductor Manufacturing Company (TSMC) is the main manufacturer and supplier of microchips to Apple and Nvidia and in fact, Taiwan accounts for more than 60% of current semiconductor supply worldwide, as well as more than 90% of the most advanced chips. Microchips are not only for the likes of mobile phone and computer names, but they are also obviously used in many industries and consumer goods, and one only has to remember back to how difficult it was in buying a car post-COVID with semi-conductor shortage being the main named reason for supply issues. In 2021, and according to Politico, 60% of appliance and machinery imports into the EU came from Taiwan. The longevity of any microchip shortage is hard to determine but given the fragile nature of these vital technology components and their susceptibility to seismic activity and their need for vacuum-like construction, existing large stores may already be damaged and current factories out of action. Nature may not give notice on when it meddles with inflation, but politicians do.

As ever, one can never stray too far away from what the US election entails for the world, and inflation will certainly figure keenly as not only an election campaign tool but what might happen if The Donald swaggers back into 1600 Pennsylvania Avenue. Full of huff, puff and bluff there will be a certain air of unfinished business in some of the early policies of a Trump II administration, one of them being a possible tariff war with China. Back in February the former US President confirmed that he would impose tariffs of 60% or higher on Chinese goods were he to win a second term in office. Bloomberg Economics have been running numbers on a successful application of the threat and found that the impact on inflation would be quite dramatic. Households would be the first to feel the upward price pressure as the core personal consumption expenditure price index, the FED’s favoured marker, increases to 3.7% by the end of next year well above the 2% target, wider consumer prices up 2.5% and GDP to lose 0.5% of growth. History is there to back up such an assumption with a CNBC observation that Trump’s trade war with China cost Americans an estimated $195 billion since 2018, according to the American Action Forum, a conservative think tank. The economic battle also led to the loss of more than 245,000 U.S. jobs, according to the U.S.-China Business Council.

It is bemusing how some quarters claim that the battle on inflation is won. My learned colleague touched on this last month as to how a hallowed 2% target by central banks is more of a wish than a necessity. However, rampant inflation of any kind cannot develop unhindered which is why the Central Bankers take on the role of Cerberus and guard the gates of Hades inflation and why they cannot commit to the wishes of the investor cavalry waiting in the wings of worldwide bourses for a signal to buy stuff. If the likes of Jerome Powell and Christine Lagarde had acquiesced already, the DOW might be above 40,000 and the Nasdaq above 20,000, but wires would now not be full of copy on when interest rates might be cut, they would instead be full of warnings as to when a hike might be considered to counter an impending late in the year inflation bloom. The US has yet to feel what the supply disruption after the Baltimore disaster might be, the world has yet to experience what another Taiwan inspired microchip shortage might do to our tech-driven world. And who knows what a returned, belligerent and score-settling Donald Trump might bring to the bottle-neck inflation table. Inflation is not beaten, it is merely contained, sedate and sedated in an interest rate pen. However, if somebody leaves the gate open, we can all say good-bye to interest rate cuts in 2024.

Overnight Pricing

© 2024 PVM Oil Associates Ltd

04 Apr 2024