Short-Term Hedge Against Escalation

The support that geopolitical events provide to oil prices is finite. When tensions rise in oil-producing regions such as the Middle East or around Russia, the market’s gut reaction is to cover short positions and build up some length. These moves are driven by perceptions, specifically, the belief that not only financial but, more importantly, physical oil supply will be adversely affected. This was evident yesterday following the Israeli strike on Hamas leaders in Qatar and the Russian drone incursion into Poland. Both WTI and Brent rose by more than $1/bbl. The resilient performance was further supported by last week’s downward revision of annual nonfarm payroll numbers and yesterday’s slight dip in August US producer prices. Equities rallied, and these two data points make next week’s Fed rate cut a virtual shoo-in.

When the perceived disruption fails to materialise, however, hedges are unwound and prices typically retreat to prior levels, or even lower, provided the fundamental backdrop has not improved. The EIA’s outlook on the oil balance for the remainder of this year and for 2026, published on Tuesday, suggests no such improvement. It neatly aligns with the latest US oil stock report, which showed builds across the board. The result was a 15 million bbl increase in US industrial stockpiles, which might just portend a significant rise in OECD inventories for the rest of the year and beyond.

For now, pragmatism remains key. Tighter sanctions on Russian crude buyers, notably China and India, could provide further ammunition for oil bulls, but such measures remain at the level of rhetoric for now. Geopolitics, with all its unquantifiable consequences, prevents prices from falling. Yet without a tangible plunge in available supply, this support can only last so long.

Bleak Future, the EIA Predicts

As pointed out above, the unpredictable but ostensibly perpetual rise in the geopolitical risk premium is putting a floor under the market, at least for the time being. However, once consensus shifts and investors begin betting against major and abrupt supply shortages, the focus will move to the perceived and actual oil balance. If the updated Short-Term Energy Outlook from the EIA is considered a reliable basis for forming an opinion, then what is now a floor under the market could well become a ceiling above it.

The latest EIA findings on the state of the global oil market are reminiscent of 2016, when the CEO of one of the oil majors famously remarked that traders might soon start filling swimming pools with crude oil. While that comparison may have been biased and exaggerated, today’s outlook is increasingly similar to that of nine years ago, particularly with regard to 2026. For context, in January 2016, front-month ICE Brent bottomed out at $27.10. Although it showed some signs of recovery later that year, it averaged just $45.14/bbl. OECD commercial oil inventories peaked at 3,048 million bbls in the third quarter of 2016 before retreating to 2,967 million bbls three months later.

Fast forward nine years, and the backdrop, while not as bleak as it was then, is hardly encouraging. The opening pages of the latest monthly report already flash red lights. The EIA forecasts a significant decline in the price of the European crude oil benchmark, projecting Brent at an average of $59/bbl in 4Q 2025 and $51/bbl for 2026, down from the August mean of $68/bbl. (It is worth noting that the Brent forward curve currently prices 4Q 2025 at around $66.70/bbl and 2026 at around $65.80/bbl, both considerably higher than the EIA forecasts.)

Both global oil demand and non-OPEC+ (non-DoC) supply estimates have been revised upwards this month, with the latter outpacing the former. As a result, the EIA now projects a falling call on OPEC+ oil. For 2H 2025, global oil demand has been adjusted higher by 120,000 bpd, while non-DoC supply has been revised up by 330,000 bpd. In 1Q 2026, demand is raised by 150,000 bpd and supply outside the producer alliance by 270,000 bpd. For the full year 2026, demand is expected at 105.08 mbpd, 180,000 bpd higher than last month’s forecast, while non-DoC supply is projected at 62.45 mbpd, an upward revision of 260,000 bpd.

The 3Q and 4Q calls of 42.00 mbpd and 42.21 mbpd on OPEC+ oil fall significantly short of projected group output, which is estimated at 44.01 mbpd and 44.41 mbpd for the second half of 2025. This results in builds of 2.01 mbpd and 2.20 mbpd, respectively, in global oil inventories. The pace of swelling accelerates to 2.45 mbpd in 1Q 2026 before moderating to an average of 1.27 mbpd across 2Q–4Q 2026.

These excess global stockpiles will inevitably push OECD inventories higher as well. They are forecast to close 2025 at 2,911 million bbls, rise to 2,975 million bbls in 1Q 2026, and end next year at 3,084 million bbls, matching the 2016 levels.

Given the high degree of uncertainty on both the supply and demand sides of the oil equation, the accuracy of the latest report is open to challenge. What stands out, however, is the EIA’s relatively optimistic outlook for OPEC+ production, averaging 44.21 mbpd in 2H 2025 and 44.20 mbpd in 2026. This compares to a July level of 41.94 mbpd, as seen by OPEC’s secondary sources.

Undeniably, as the group accelerates the unwinding of production constraints, output will continue to rise, but it may not reach the projected 44.20 mbpd by the end of next year. This is particularly likely if the anticipated weakening in oil prices materialises, which would act as a disincentive for both OPEC+ and non-OPEC+ producers to expand output meaningfully. Nonetheless, absent unexpected supply disruptions in global geopolitical hotspots, the current state of the global economy points to ample supply and rising inventories. The only question is the scale.

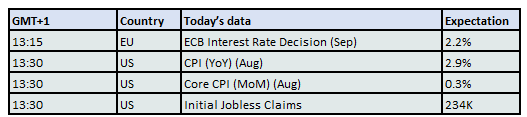

Overnight Pricing

11 Sep 2025