SPR Release or Not, Concerns Remain

Nothing alleviates the disruption to oil supply, production, and exports from the Persian Gulf. After yesterday’s International Energy Agency announcement about a coordinated effort to flood the market with 400 million bbl of oil over 90 days, equivalent to around 4.5 mbpd, and the US floating the idea of a waiver to the Merchant Marine Act of 1920, oil rallied back above $100/bbl and Heating Oil flirted with the $4/gallon mark, which is equivalent to $168/bbl. The explanation is simple: ships are ablaze in the Gulf, the Strait of Hormuz is closed, and the newly elected Iranian supreme leader has stressed that it will remain shut as a tool of pressure on adversaries.

Overnight, the US Administration took further steps to ease the pain. The 30-day sanction waiver for India to buy Russian oil, announced on March 5, was extended globally last night and will remain in place until April 11, with dubious effect. The market remains unimpressed as the available Russian oil on water, reportedly 124 million bbls, would cover less than a week of oil transit through the Strait of Hormuz. The US, in effect, is now funding Russia’s war against Ukraine, a disturbing U-turn from its pre-Iran foreign policies. The move and the subsequent reaction to it clearly illustrate that Iran has as much leverage to shape the outcome of the conflict as its main foe.

No Impending Price Relief, Reports Suggest

Usually, this is the time of the month when readers are bombarded with data on global and OPEC+ supply, as well as worldwide and OECD demand figures for the coming quarters, as the updated findings of the three major agencies, the EIA, OPEC and the IEA, are released. Because of the joint US/Israel attack on Iran and the subsequent retaliation from the Persian Gulf OPEC member, which has wreaked havoc around the most crucial shipping lane in the Middle East, such an exercise might be futile - although it is still worth glancing through the fresh numbers. What is more germane is to present the views of these researchers on how they see the unfolding, and frankly unprecedented, Iranian crisis impacting oil production and supply from the region in the immediate future. The EIA and, to a certain extent, the IEA do their best to put hard numbers on their estimates. OPEC, on the other hand, has stuck to its approach of not predicting future supply or output levels from the group.

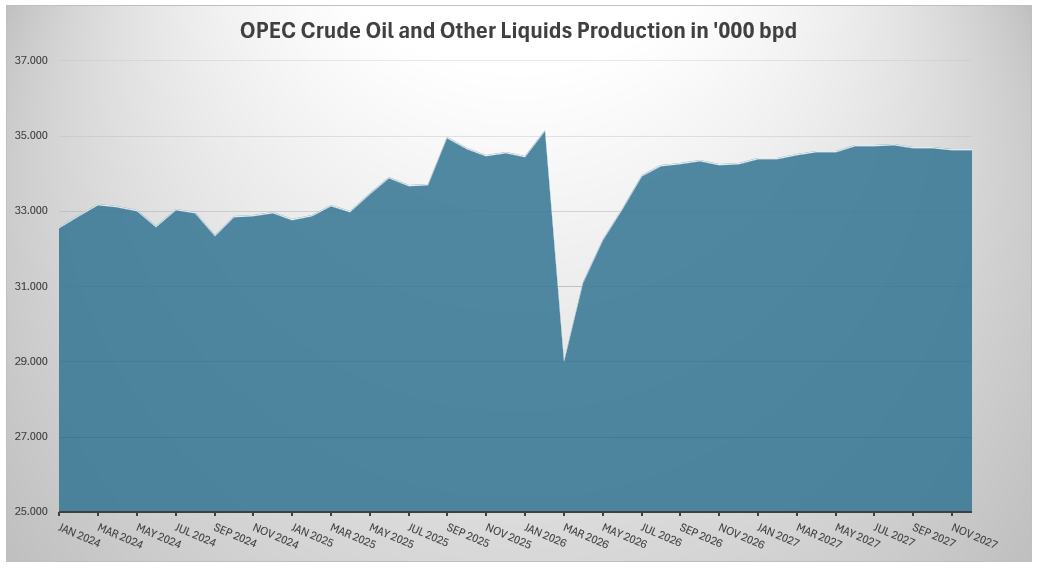

The EIA does not beat around the bush. It sees Brent above $95/bbl for the coming two months, before falling to $80/bbl in 3Q and to $70/bbl by the year-end. For the whole of 2026, the average is currently seen at $79/bbl and for 2027 at $64/bbl. These upgrades of $21/bbl and $11/bbl, respectively, from the previous month encapsulate the severity of the tension. US retail gasoline prices were revised up from $2.91/gallon to $3.34/gallon for this year, and from $2.93/gallon to $3.18/gallon for 2027. Why? The chart below explains.

The EIA expects a drop of 6 mbpd in OPEC crude oil and other liquids production from February to March, with the recovery not expected to be complete until the fourth quarter of the year. Supply from the OPEC group was revised down by 2.12 mbpd for 2Q and by 250,000 bpd for 3Q month-on-month. Of course, these are modelled assumptions that can and will be corrected as events in the Middle East evolve.

As indicated above, OPEC did not comment on the possible reverberations of the Iranian war, which is having a direct and disheartening impact on several member states. What it did do was leave both global oil demand and non-DoC supply estimates broadly unchanged for the rest of the year. Consequently, the call on the alliance’s oil also remained untouched.

Because of the Middle East supply disruption, the IEA estimates that there will be 8 mbpd less oil available in March than in the previous month. The Agency also emphasises the adverse impact on product movements and refinery operations. Product flows through Hormuz have been halted, and about 3 mbpd of refining capacity has been shut. Whilst the 400 million bbl SPR release is meant to alleviate the effect of the disruption, further losses cannot be ruled out should the hostilities prove prolonged. Although the IEA does not provide OPEC supply estimates, it does forecast OPEC+ production levels. The deficit relative to the February report is 3 mbpd in 1Q and 2.4 mbpd in 2Q. This month’s projection for 3Q matches that of February.

OPEC, as noted, saw no reason to revise its global demand and non-OPEC+ supply forecasts and, as such, no change in the OPEC+ call was forthcoming. The EIA and the IEA, on the other hand, upgraded their 2Q DoC demand estimates substantially. As falling OPEC production in 2Q is now part of the equation, it is difficult to see oil prices retreating anywhere near pre-war levels. It is tempting to think back to the very recent 2026 price forecasts of $60/bbl with some sentimentality, but even nostalgia is not what it used to be.

Overnight Pricing

13 Mar 2026