A Star-Spangled Rodeo

It may have only been a year since his inauguration, but the troubadour of trouble seems to have been walking these streets so long and singing the same old song of conflict that markets should be inured to a capricious President Trump. But his subject matter is so wide, and his fog-horned solutions so spiked with immeasurable consequence, that oil market participants can ill-afford to roll their eyes and dismiss him with a ‘whatever’. It is indeed a target-rich environment for the President to take pot-shots or fire salvos at, but most of them are of his own making. Taking from the 1939 British WWII motivational poster, there must be a ‘Post-it’ note next to his machine of choice when updating ‘Truth Social’, reminding him to “Keep Bloviating and Carry On.”

The ouster of Nicolas Maduro took another twist last week and as seen in an exclusive for Reuters, Trump speculated that it would probably be better if the South American and founding OPEC country stay in the cartel. If the US intends to remain in charge of Venezuela’s oil industry for the foreseeable future, is it then by default also part of OPEC? There is little reason to believe the US is about to share the much-sought sour crude produced from the Orinoco Oil Belt, after all, nearly three-quarters of US refining capacity is designed for heavier crude. Indeed, as seen in Al Jazeera, the University of South California reminds on how “many of the US refineries along the coasts of Texas and Louisiana were built and designed to process Venezuela crude.” There might just be dire consequences for the US domestic oil industry. While any meaningful amounts of heavy feedstock from the south will take time to plot along the US Gulf Coast, the huge flows of lighter US crude grades will be fighting even harder now for international customers. Prices are starting to vote with such a thought as Brent futures slowly begins to outperform its US cousin, not only in structure but in how the WTI/Brent arbitrage continues to falter.

On the week, M1 futures in WTI finished +$0.32/barrel (+0.54%), Brent +$0.79/barrel (+1.25%), Heating Oil +10.26c/gallon (+4.81%), RBOB +0.46c/gallon (+0.26%) and Gasoil +$22.50/tonne (+3.56%). The paltry increase in the crude prices belies the ranges of the week. Both WTI and Brent enjoyed around $4/barrel ranges but importantly were up $3.50/barrel before qualification of US military intervention in Iran were seen from a reality-checked Trump. The commander-in-chief had little option to adhere to his advisers that due to the rotation of US aircraft carriers to other parts of the world, there just was not enough firepower at hand to carry out his promise of help being on the way for Iranian protestors, the very same folk who have likely been inspired to air their grievances because of the effect of US sanctions on their everyday lives. Although, there are reports of USS Abraham Lincoln carrier battle group moving back to the Middle East. As it was, prices might have fallen into negative territory if it were not once again for the intervention of the decent distillate performance. The drone strike on tankers last Tuesday in the Black Sea is a reminder on how Russian oil assets are vulnerable particularly at this time of winter in the Northern Hemisphere. A new disruption of the Polar Vortex has begun, according to some weather trackers, and therefore an increased likelihood of severe bouts of cold air across North America and Europe can be expected in late January going into early February with any oil shortages from either concern finding first footing in diesel and heating oil.

Make America great again is more like make America larger. The ex-reality TV star’s inner dreams of being a ‘face’ on Mount Rushmore might see some sort of against-all-odds bizarre fruition if Greenland is added to the land mass of the United States. The North Atlantic Island is larger than both Texas and Alaska and what a feather it would make in Donald Trump’s Davy Crockett hat. The trouble is this current form of frontiersman is tearing down the world order of allies and the announcement by The Donald that he will impose an extra 10 percent tariff on all goods sent to the US from Denmark, Norway, Sweden, France, Germany, the United Kingdom, the Netherlands and Finland, for opposing any US expansion desires will once again shake North Atlantic relations to the core. So much for last year’s policy of rolling over in appeasement and flattery, showing one’s belly to this bully has clearly not worked. It is baffling that the reason used by the White House for this verbal invasion, if not yet military one, is to counter China and Russia but such a move can only be an enabler for Beijing and Moscow’s desire to expand their own borders. President Xi can find justification in any plans to reacquire Taiwan because the US and its current allies are traversing the Taiwan Strait and pose a security threat. Likewise, the Greenland language can be spun by a probably delighted President Putin on how his campaign into Ukraine is to protect Russia from NATO/European expansion. Calling Greenland’s price influence either way for oil is impossible, but the anxiety felt by all markets and the citizens of the world should not be underestimated and at least initially will discourage risk takers from being overly expressive. If an ensuing trade war breaks out, which at present seems more plausible than a shooting one, the globe will once again have to face up to the prospect of reduced trade and by default lower oil demand.

In recent times, the US stock market is very much able to ignore plenty of what spews forth from the White House because the main drivers, as in A.I. associated tech companies, are afforded elite status. Such is the passion for Nvidia et al, that they are treated as a rare and tangible asset, which is a stretch when said out loud, but with a lack of amortisation normally seen in intangibles and quarter after quarter of positive results they have become the basis of investments in which portfolios are leveraged against, and by default immune to intra and inter-day geopolitical strife and are thus frequented by long-only thinking and institutional investors. Who cares about the dividend when the flat-price increases by 30 percent each year? Overblown, over-brokered, vulnerable to cheaper rivals from the likes of China and bubbled? Probably all eventually right, but we have heard the same naysaying for the last 2 years. Still, reduced trade and the unwinding of 70 years of allied treaty cannot be ignored which is why global bourses are protesting this morning and, in some cases, losing up to 1 percent of their value. If markets are experiencing anxiety, then spare a thought for those in the Inatsisartut (parliament) of Nuuk and how they must explain to Greenland’s 57,000 inhabitants that given a worse-turn of events, they might just come under the heel of the real estate autocrat in the White House who is currently plucking at really bad chords on the harp of peace as would a legendary misanthropic classical god before his eventual fall. But, not before much damage and despair.

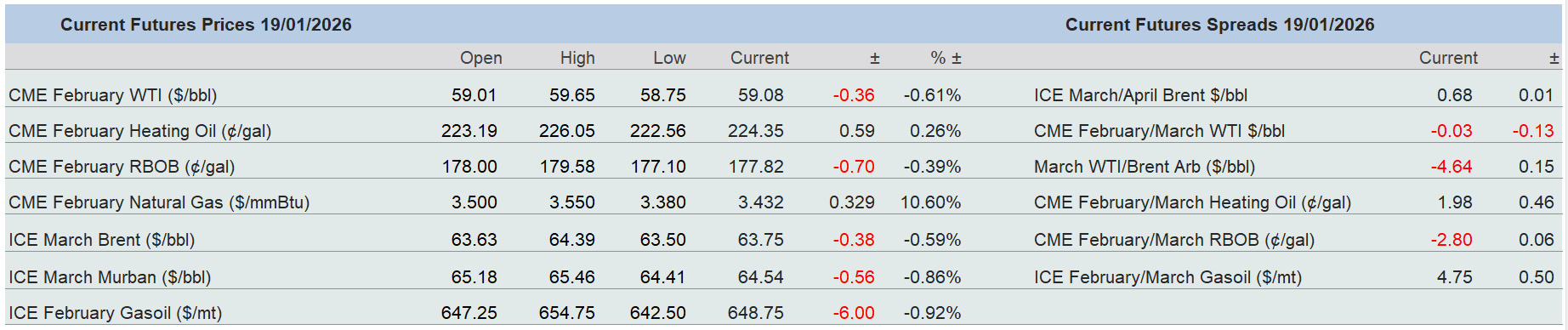

Overnight Pricing

19 Jan 2026