Supply Disruptions Still Overrule Tentative Demand Headwinds

If the potential US-Iran ceasefire agreement is on “life support”, if Saudi Arabia, as reported by Reuters, has launched several unpublicised retaliatory attacks on Iran, and if Iran now defines the critical transport route as a significantly larger zone than before the war, then the odds of the conflict escalating and potentially causing further damage to oil installations and infrastructure in the region are growing. The risk of renewed tension sent crude oil prices significantly higher yesterday, although some of these gains are being given back this morning ahead of President Trump’s visit to China.

Supply remains severely constrained, yet it is only prudent to draw attention to the demand side of the oil balance, too. Economic turbulence, precipitated by the 10-week stand-off between the adversaries, is intensifying with each passing day that oil remains expensive. Since energy impacts every aspect of life, the bigger-than-expected rise of 3.8% in US consumer prices last month serves as an ominous warning signal that the longer the conflict lasts, the greater the damage will be. Consumers will spend less, manufacturing will become more costly, and central banks will be forced to make borrowing an increasingly unattractive option by raising rates. As discussed below, supply destruction is still the predominant force in the formation of oil prices, and in the case of a serious escalation, new year-to-date highs remain more than a realistic possibility. But the explicit effect of the war on the global economy is undeniable, and it may explain why investors are reluctant to react more aggressively to the increasingly gloomy peace prospects.

Tighter for Longer

In the current unpredictable environment, it is a reasonable and understandable assumption in any supply-demand outlook that the hostilities between the US/Israel and Iran will end in the foreseeable future. If the conflict drags on, however, the forecasts on both the supply and demand sides will be amended accordingly in the following month. This is the approach the EIA has adopted; therefore, the downgrades to demand prospects are entirely logical. After all, oil prices remained comparatively elevated over the past month, which must be reflected in consumption estimates. There were substantial recalibrations in both non-DoC and DoC supply data following the UAE’s decision to leave the OPEC+ producer group. Looking at global supply figures, one finds an even more significant downward adjustment, implying that the oil balance, at least for the remainder of 2026, will be much tighter than expected only a month ago. Similar changes can be anticipated in June, with a whole gamut of datasets likely to show considerably different values from the current figures if the Strait remains shut in the weeks ahead.

Because of the UAE’s shock decision to terminate its OPEC and OPEC+ membership, it is only sensible to examine the broader supply picture and determine what changes have occurred over the last month. Global supply projections for the whole of 2026 were cut by 2.67 mbpd month-on-month, with the quarterly adjustments as follows: 2Q -3.79 mbpd, 3Q -5.17 mbpd, and 4Q -1.6 mbpd. A normalisation is expected in 2027, with global supply estimates matching the April forecast and expanding by almost 8 mbpd from 2026 levels. Returning to the near term, the EIA estimates that Iraq, Saudi Arabia, Kuwait, the UAE, Qatar, and Bahrain collectively reduced output by 10.5 mbpd last month. The updated report also assumes that the Strait of Hormuz will remain effectively closed until late May, with shipping traffic beginning to recover in June. Oil shipments through the Strait, however, are unlikely to return to pre-conflict levels until later this year, and “we expect some oil production in the Middle East to remain disrupted over that period.”

The slower-than-previously-anticipated recovery in production by Persian Gulf countries naturally supports oil prices, which, in turn, adversely affect oil demand. The annual downward revision amounted to 410,000 bpd, with 2Q cut by 410,000 bpd, 3Q by 470,000 bpd, and 4Q by 440,000 bpd. Global oil demand is now expected to grow by only 180,000 bpd in 2026, versus a supply contraction of 3.73 mbpd. The picture will reverse next year, with consumption expanding by 1.49 mbpd compared to a 7.90 mbpd increase in global supply.

As the cuts to supply projections significantly exceed those to demand, the oil balance will be tighter than estimated last month. The direct consequence of these revisions is faster stock depletion, both globally and across the developed world. Inventories are expected to decline by 8.47 mbpd in 2Q and 4.41 mbpd in 3Q, before turning into a build of 2 mbpd at the end of the year. The average drawdown of 3.63 mbpd over the 2Q–4Q period compares with a decline of just 550,000 bpd forecast last month. Again, due to the continued closure of the Strait, the outlook has worsened considerably. OECD stocks will fall to 2.413 billion bbls by the end of 3Q, the lowest for at least 20 years.

This deterioration is only partially reflected in the oil price forecast. US retail gasoline prices are estimated at $3.88/gallon this year and $3.62/gallon in 2027, 18 cents/gallon and 16 cents/gallon higher, respectively, than in April. Curiously, the Brent spot price, which was projected at $96/bbl for 2026 last month, is now expected to average $95/bbl despite steeper stock declines. For next year, however, the forecast was revised higher by $3/bbl, from $76/bbl to $79/bbl. Our key takeaway from the EIA’s latest findings is that both supply and demand will continue to be destroyed in the current and following quarters, with the former contracting far more rapidly than the latter. An unhelpful conclusion would be that the massive gap between production and consumption destruction could narrow significantly, possibly shortly after oil starts flowing through the Strait again. It is an uninstructive observation, since no one knows when it will happen.

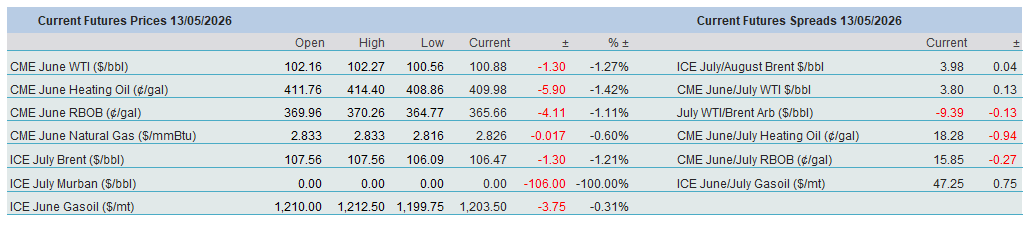

Overnight Pricing

13 May 2026