Supply Shock Triggers Inflation Shock

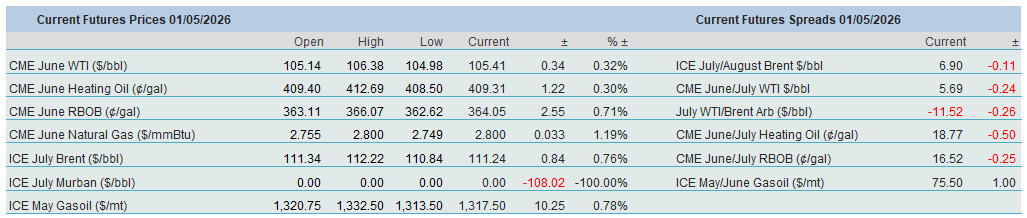

Although prices fell yesterday—perhaps due to the Brent expiry or a reassessment of the damage the Persian Gulf stalemate has caused so far—the weakness was observed on the front-end, the fundamental backdrop has not changed, and the reopening of the Strait of Hormuz is anything but imminent. In fact, the Middle East menu is becoming increasingly Mexican: the appetiser is NACHO (Not A Chance Hormuz Opens), followed by TACO (Trump Always Chickens Out). The former is a novel invention of a creative trader, while the latter is now a ubiquitous phrase coined by a Financial Times journalist. The US President appears determined to keep this pivotal chokepoint under blockade until Iran breaks, but the autocratic regime’s resilience may once again be misjudged by his administration. As a result, price spikes—such as the one seen in the early hours of yesterday’s session—are likely to persist.

When energy is costly, inflation does not fall, and central banks react with inertia. After both the Bank of Japan and the Federal Reserve left interest rates unchanged, the Bank of England and the European Central Bank followed suit. Their leaders warned of rate increases in the coming months if stubbornly high energy prices push consumer prices higher. They cannot be blamed for this narrative, and—to quote the BoE governor—“forceful tightening” may be required. Right on cue, eurozone inflation rose to 3% in April, according to flash data. The new Fed chair may be forced to begin his tenure by alienating his predecessor, leaving rates unchanged or even raising them, as the March Personal Consumption Expenditures Price Index—the central bank’s preferred measure—accelerated to 3.5%, up from 2.8% in February. The seeds of demand destruction are being sown in plain sight, yet stakeholders still believe that global supply will remain in deficit for the foreseeable future.

Risk is Precariously on the Upside

Politicians, economists, investors, and analysts are all predominantly preoccupied with the potential impact of the Iranian war. Everyone has a view, but these can differ considerably. It should not come as a shock since a social media post can upend even the most carefully and thoroughly crafted research. A sensible approach is to establish several scenarios and examine their potential effects one by one. Below is a synopsis of the latest World Bank publication, released two days ago, titled Commodity Market Outlook. We shall pay particular attention to energy and oil.

The significance of the Strait of Hormuz in international commodities trading must not be underestimated. Around 50% of the seaborne sulphur trade passed through it before the conflict. The figure is above 30% for crude oil, just below this level for LPG, around 20% for refined products and LNG, and approximately 15% for chemicals. Disruptions, therefore, reverberate across global economies.

The magnitude and impact of the closure are best illustrated by initial oil supply losses in historical episodes. According to the World Bank, losses peaked at 10 mbpd in March, with the Iranian Revolution now in second place, having caused less than 5 mbpd in losses. The Libyan civil war affected “only” 2 mbpd of production. Consequently, the current hostilities have precipitated the largest energy supply shock the world has ever experienced. The World Bank estimates that its energy price index will increase by 26% year-on-year in 2026—the first annual rise since 2022—before retreating by 17% in 2027. This scenario assumes that the most acute phase of the disruption will be over by the end of May. Even under this assumption, it will take more than a year to re-establish the pre-war status quo. This would imply an average Brent price of $86 in 2026, before falling to $70 in 2027. Of course, a prolonged closure would result in painful price revisions, with Brent possibly averaging in the $95–$115 range this year.

Global oil consumption is expected to decline in advanced economies, as well as in the Europe and Central Asia (ECA) and Middle East and North Africa (MNA) regions, while expanding in other emerging markets and developing economies (EMDEs). Growth in oil output will contract, as the supply disruption in the Persian Gulf will considerably exceed production increases elsewhere. The World Bank, which partly bases its analysis on IEA data, expects the global supply–demand balance to plunge into a deficit of 3.7 mbpd in Q2 2026, the highest ever recorded.

Depending on future developments, the World Bank establishes both “upside” and “downside risk” scenarios. In the former, oil price forecasts may need to be revised upward in the event of re-escalating hostilities in the Middle East or persistent disruptions to regional oil flows. Medium-term damage to regional production and exports cannot be ruled out either, and global oil production capacity could be revised downward by as much as 4 mbpd. This would lead to a significant upward adjustment in oil price forecasts, as indicated above.

Downside risks could stem from three potential sources. First, resilient inflationary pressures may dampen risk appetite, as economic growth proves weaker than expected. Second, rising concerns about oil security could accelerate electric vehicle (EV) adoption. Finally, a sooner-than-anticipated resolution of the shipping crisis in the Strait of Hormuz, coupled with resilient US shale oil production, could ease the tight oil balance.

The paper also devotes an intriguing chapter to the effects of geopolitical oil supply shocks, using a novel methodology. It examines the behaviour of the oil market during periods of elevated geopolitical risk and attempts to quantify these effects. It finds that during spikes in geopolitical tension, a 1% reduction in supply generates an average price increase of 11%—almost twice as much as previously estimated. This seemingly exaggerated reaction to supply shocks is driven by an increased risk premium, reflecting both physical constraints and speculative activity. Additionally, supply disruptions stemming from geopolitical upheavals lead to compounded precautionary measures to secure future supply, particularly through inventory building.

Overnight Pricing

01 May 2026