Turkish Delight in the US

After the three-day Easter hiatus, the performance of gold, the dollar, equities, and bonds are reliable barometers of the direction the oil market takes. Gold’s astronomical rise continued yesterday with another 2.9% jump, taking the combined return to 15% since April 7 and 33% since the US election last November. The dollar has been in a freefall for the past three months and the parachute has not opened yet as its index against six major currencies reached a nadir not seen for three years. The 10-year Treasury bond yield edged higher also reflecting ominous investor sentiment.

It is reasonable to assume that the tariff war between the two biggest economies cannot get worse than it is now. By that we mean that it is broadly irrelevant whether the US and China keep throwing numbers around and impose 150%, 250% or 500% punitive taxes on each other’s goods. Trade flows, it is safe to conclude, will come to a near complete halt between the two nations leading to elevated consumer prices. The Conference Board’s Leading Economic Index, composed of 10 economic components and usually deemed the messenger of near-term trends, fell sharply in March. Deteriorating financial data has been accounted for in asset prices. What triggered yesterday’s meltdown was President Trump’s recalcitrant attitude toward his appointee of the Federal Reserve. His stubborn view of lowering interest rates is reminiscent of the Turkish President’s admiration of cheap borrowing as the monetary Holy Grail to cure economic slowdown. The result was an inflation of over 80% in October 2022 with the Turkish lira worth less than tuppence ha’ penny - literally. No such drastic collapse of US fortunes is anticipated but it is only a natural reaction to get rid of further US assets, including stocks, when the Fed’s independence is under threat. The S&P 500 index plummeted 3.27% yesterday.

In these uncertain times, oil follows equities and yesterday’s sell-off, which took the price of Brent $1.70/bbl down on the day, was exacerbated by conducive developments in the US-Iran nuclear talks as negotiators agreed to lay down the framework for a possible deal. It, nonetheless, would be foolish to believe that the handshake and the embrace between these adversaries are imminent and talks could break down faster than you can say Grand Ayatollah. Abrupt rallies, therefore, cannot be ruled out but only an implausible change in US trade policies will significantly brighten the presently gloomy mood.

Annual Energy Outlook 2025

The Energy Information Agency, the statistical arm of the US Department of Energy is required by law to prepare an annual report about trends of energy supply and demand in the US. The policy assumptions of the latest report, published on April 15 consider laws and regulations implemented as of December 2024 and cover the period throughout 2050. It is an important criterion as with the new administration, which came into power in January, laws and regulations underwent considerable changes therefore the diagnosis might differ meaningfully from the ones presented in the Annual Energy Outlook 2025 (AEO2025). As with most projections, the AEO2025 offers Reference and Alternative Case scenarios. Below we sum up what we deem the most informative findings of the AEO2025, including but not limited to the Reference Case scenarios.

It is sensible to begin with macroeconomic assumptions. Under the Reference Case scenario, the US economy will grow 1.8% annually between 2024 and 2050. (As a reminder, according to the US Bureau of Economic Analysis, the US economy expanded at the rate of 2.8% in 2024.) Under the Low Economic Growth case, the number drops to 1.2% whilst the optimistic assumption envisages a growth rate of 2.1%, still considerably under the 2024 figure. From the Low to the Reference and to the High Economic Growth case the population will grow 0.1%, 0.3% and 0.5% whilst non-farm employment will, on average, expand by 0.2%, 0.3 or 0.5% a year.

The AEO2025 sees US energy consumption peaking this year at 94.60 quadrillion Btu, up 0.9% on 2024 then gradually retreating to 88.19 quadrillion Btu by 2050, an average annual decline rate of 0.2%. Consumption of major refined oil products, such as motor gasoline, kerosene, and distillate fuel will all decline in the next 25 years and so will that of natural gas. The unstoppable prevalence of electric vehicles is mirrored in assumed gasoline consumption, which is projected to shrink by 2.2% a year or 45% between 2024 and 2050. Jet fuel demand, on the other hand, will increase by 0.9% annually or 25% in 26 years. Whilst the transition, albeit slower than anticipated, is irrevocably under way, consumption of petrochemical feedstocks will remain robust with an average annual growth rate of 4% or close to 200% between 2024 and 2050.

The total primary supply of petroleum and other liquids will fall from 20.79 mbpd in 2024 to 16.90 mbpd in 2050, an average annual contraction of 0.8% or 19% over the 26 years. It is curious to observe that the US will nearly double its net product exports from 4.80 mbpd last year to 9.06 mbpd in 2050, an annual growth rate of 2.5%. The opposite is true for crude oil. Net imports are expected to be down to 1.89 mbpd in 2025 from 2.45 mbpd in 2024 but by the end of the reporting period, are seen at 4.04 mbpd. And the reason? Peak crude oil production is predicted at 14.00 mbpd in 2027 after which a steady decline will have it reach 11.28 mbpd in 2050. The solid downturn in US crude oil production is almost exclusively the result of a plunge in shale output. Tight oil production, which is estimated to ascend from 9.15 mbpd in 2024 to 10.00 mbpd in 2027 will fall to 7.77 mbpd by 2050 whilst retaining its share of 69% of the total US crude oil output. As pointed out above, the AEO2025 is based on laws and regulations as of December 2024, yet the current administration’s campaign pledge of increasing production by 3 mbpd as part of the grand plan to achieve energy independence seems genuinely unattainable.

Under the Reference Case scenario Brent will bottom out this year at $72/bbl, stabilizing around $80/bbl between 2026 and 2033 only to rise to $91/bbl by 2050 in 2024 dollars. WTI follows a similar trajectory. It will advance from $68/bbl this year to $77/bbl in 2033 and to $89/bbl 17 years later. Because of the diminishing popularity of combustion engines, gasoline prices at the pump will fall from $3.45/gallon in 2024 to $2.61/gallon in 2050, an annual decline rate of 1.1%. The AEO2025 confirms the general belief that although the transition from fossil fuels to renewable energy is a fact of life, demand for the former will remain comparatively healthy in the coming decades. Yet, the uncertainty surrounding the global economy and our market is aptly echoed in the High and Low Brent Oil Price cases which range from $155/bbl to $47/bbl for 2050.

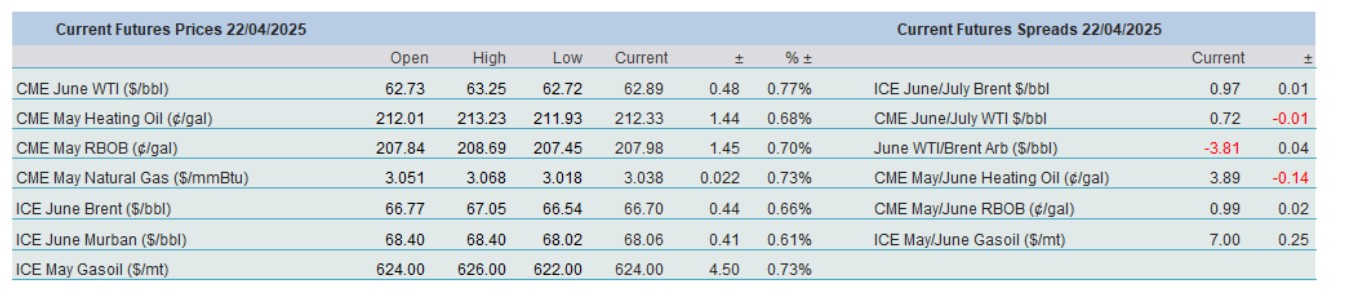

Overnight Pricing

22 Apr 2025