Ukraine, Alone in Action - Again

Even though each week threatens to reveal a final solving of the never-ending and multi aspects of a Russian solution in oil market thinking, there is always a Narnia cupboard door allowing an escape into fantasy to gather more unforeseen and unexpected twists. The political masterclass of buying time was in full resplendence in Türkiye last week; the geography in which any ceasefire agreement might be achieved between Kyiv and Moscow. The Russian chargé d’affaires, Alexie Ivanov, expressed how his country remained ready for peace talks, being lip service to US Secretary of State Marco Rubio's conclusion that Moscow was not ready for dialogue, and obfuscation as the Kremlin’s forces gain the upper hand in the three-year slaughter. The intervention was successful, at least in oil price terms, well, for a while anyway.

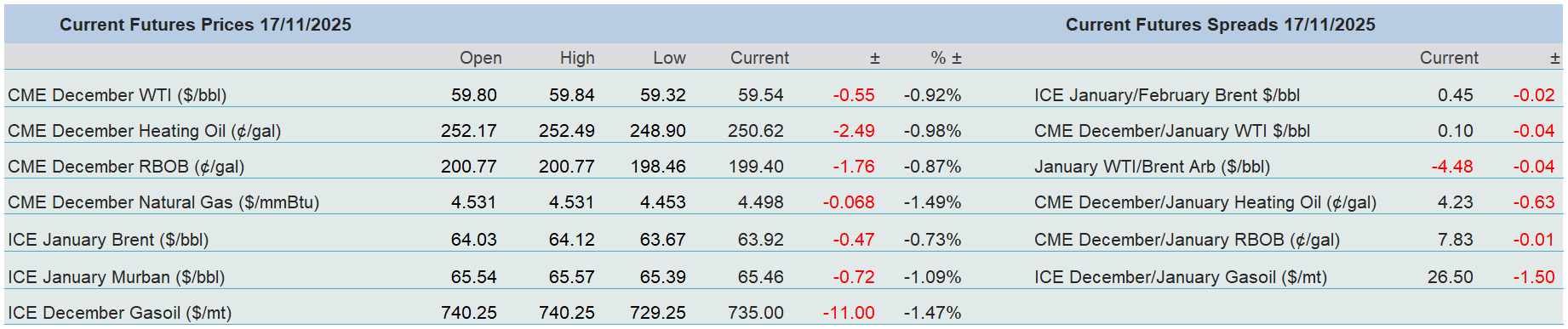

The mid-week fade lower was ultimately overshadowed and accelerated by the monthly report from OPEC in which it decided now was the right time for a reset in its forward thinking on the oil supply/demand balance and brought them into much more mathematical alignment than its previous musings. The glut of oversupply stories once again started to shout louder and if it were not for another successful drone attack by Ukraine into the Black Sea port of Novorossiysk causing a halt to oil exports estimated to be around 2 percent of global supply, prices might just have finished in much more of a negative state. Ultimately, and on the week, M1 WTI finished +$0.57/barrel, Brent +$0.76/barrel, Heating Oil +4.90c/gallon, RBOB +7.13c/gallon and Gasoil -$14.75/tonne with the European distillate being largely pulled lower by the monthly expiry. The modest changes belie the inter and intra-day moves, where it is now acceptable and indeed necessary to change one’s mind hourly, let alone daily.

Whatever sanctions might have been placed on Rosneft and Lukoil, the very fact there is competition in part purchases of their empires reveals how successful bidders believe assets can still be utilised and makes a mockery of their oil networks not being able in the future to still spill forth black gold. Therefore, the scepticism on how and if US sanctions will ever be fully implemented remains rife, and even Bloomberg’s reporting of a Senate bill allowing President Trump to impose tariffs of up to 500 percent on imports from countries that buy Russian energy products and are not actively supporting Ukraine, being deemed “okay with me,” overnight by Trump, agnosticism will attend all such strategies until they become reality. Kyiv obviously shares this view, which is why its drone response and all-out attacks on Russian oil infrastructure is really the only game changer the oil market has in its locker at present.

Nvidia earnings this week ramp up in importance

Meanwhile, unfolding in the world of equities is a smidgen of doubt. What has been the catalyst for this momentary self-assessment is the lack of data coming from the US government. It is curious that even when there is bad news, equity hunter-gatherers always glean a reason to buy, but it seems the paucity of metrics on unemployment and inflation gives over to doubt which is the enemy of positive sentiment. The obvious relief when the record-setting government shutdown was finally over was represented in the Dow Jones punching to an all-time high after President Trump signed the interim budget bill. For over a month markets have had to cope with being unable to peruse official data but whether or not they are acted on is ancillary, the measures give a numeric narrative allowing informed decisions, even if that includes ignoring them. Therefore, it is odd that such reticence has not been expressed before now. Masking over the cracks were the week before results from the mega-caps and their astonishing ability to defy gravity and warnings of overvalue.

However, not a one of the equity in-crowd saw the sucker punch delivered by Japan’s investment giant SoftBank. What might just be an end-of-year book-out, could well be rather prescient as the bank belatedly reported on how it unloaded its entire holding of Nvidia stock in October. Now, while the move is being seen as freeing up of capital and a doubling down on exposure to A.I. bets, when such a big player sells 32.1 million shares of anything all markets must sit up and pay attention. As much as analysts contend an entire evacuation of such a position is not a judgement or renewed negative stance on Nvidia, but a realisation of A.I. ambitions, those who have been gracing the airwaves with ‘bubble’ talk have found a greater number of ears willing to listen to misgivings.

Enthusiasm in stock markets have also been given another rung of concern. Arguably the biggest frightener for investors is inflation and with the data desert in Washington currently preventing any analysis of official metrics, what appears to be a recognition by the Trump Administration on the hardships now being felt by millions of Americans due to passed-down tariff costs is a shot across the bows for confidence. Such supermarket staples of fruit, meat, juices and many, many more are having tariffs rolled back by renegotiated trade deals with the South American suppliers whose products populate the aisles of American mercantile. It is a significant climbdown from a President who perpetuated in his rank and file the idea of ghastly foreign countries preying on the needs of US consumers, and even if he did manage an unlikely win in a randomly chosen $5 billion figure from his defamation case against the BBC, and an even more unlikely drop of courtroom gained booty into the American exchequer, it would not be enough to counter the pain being felt by the majority of his day-to-day fellow citizens.

It appears the cause and effect of tariffs have berthed in the US, and they are many layered with inflation being at the top of the pile. Howsoever the threat of rising prices has arrived, it is being greeted with concern by those at the top of US monetary policy making. Federal Reserve members often speak in riddles with any views aired covered with disclaimers of ‘ifs’ and ‘buts’, yet markets are seizing on a growing indication of a hold in rates at the next decision due in December. According to Reuters, on Friday, Kansas City Fed President Jeffrey Schmid, Dallas Fed President Lorie Logan and Cleveland Fed President Beth Hammack largely repeated the hawkish views each had laid out soon after the Fed cut its policy rate last month. Even the usually dovish Christopher Waller, the would-be Powell successor, voiced concern when measuring higher economic growth versus worsening employment being exacerbated by the lack of official measures. He intimated that unless the two showed more harmony, then it would be inappropriate to make changes to policy that might be so damaging as to be reversed at a later date. The sentiment change in pricing is stark. Using the CME FedWatch tool, one month ago a 25-basis point cut in December had an 88.2 percent probability, the week before last it was 66.9 percent and at close of business on Friday it registered at 44.4 percent. Investors for the first time are experiencing a many-sided shape to warnings rather than just overvalue, and while nothing here signposts a path to the ruination of all, ‘vigilance’ and ‘correction’ warnings are about to become de rigueur in the writings and talking heads of stock market analysis.

Overnight Pricing

17 Nov 2025