Unanswered Questions

Two months into the new USA Administration’s activities, unpredictability keeps ruling. Sabre-rattling continued last month, and threats were flying around all over the place. Several, closely or loosely related questions need answering, possibly a challenging undertaking. Whilst it is implausible that reassuring answers will be provided any time soon, it is becoming slightly clearer what to expect from the US in the foreseeable future in foreign politics, the economy and oil. The bottom line is that there seems to be no limit to testing or even overstepping boundaries, ethical or legal. The idiosyncrasy of the apparatus can be characterized as brazenly flexing enormous political and economic muscles without the slightest hint of willingness to co-operate.

The political rhetoric and agenda of the US government are one of belligerent peace attempts and territorial demand. The topic of annexing Greenland or making Canada the 51st state of the US resurfaces on a frequent basis. The temperature in geopolitical hotspots, namely Ukraine and the Middle East has not cooled. Peace, whatever its definition, remains elusive notwithstanding campaign pledges. The brokered truce between Russia and Ukraine currently seems implausible. If the weekend’s outburst of Mr Trump is to be taken seriously (and it should not be), his admiration towards the Russian strongman is on the descent. The US takeover of Gaza seems to have fallen off the foreign policy agenda and the number of casualties in the Palestine enclave keeps rising horrifyingly. It is sadly intriguing to observe that the last two months have emboldened autocrats globally, and they further consolidate their power on their home turf. Add to that the animosity the US transparently projects towards Europe and the declared withdrawal of security guarantees, and it becomes conspicuous that the political world order, as we knew it, has ceased to exist.

The economic agenda, as capricious as it is, is perceptibly one of favouritism of the manufacturing sector, through tariffs and not spending, at the expense of consumers. Investors seem very concerned. The S&P 500 lost 5.75% last month and 4.59% in 1Q. The same returns are -8.21%/-10.42% for the tech-heavy Nasdaq Composite Index This compares with a retreat of 4.15%/1.69% in the MSCI All-Country Index. The German stock market fell 1.72% in March but returned 11.32% in 1Q. The latter is the ultimate manifestation of US foreign policies as the cooling relationship between former allies led to the ramping up of defence and infrastructure spending on the old Continent, albeit the long-term positive effect is questionable as it is dubious how to finance it without cutting back on spending in other parts of the economy or increasing taxes.

The question that arises in the light of the US protectionist economic agenda is how long the Administration will tolerate weakening equities. To put it differently, is inflation or recession a real threat? Or in an even more ominous case, is stagflation a possibility? Decision makers of the world’s strongest economy are convinced that the current move lower in equities is merely a temporary phenomenon before the impositions of tariffs, which are meant to compensate for tax cuts, bear fruit. One unknown is how far equities need to fall in order to reverse the planned tariff regime and whether there would be a willingness from the administration’s side to do so. No doubt, economic data in the coming months will be the measurement of the performance of the US economy. For now, not much should be read into hard data from February or March since the wheels of tariffs are not fully in motion yet, however, the deterioration of investor and consumer sentiment is tangible. The 19% rally in gold prices in the January-March period insinuates growing anxiety about US and global growth prospects.

The salient dilemma in our market is how long the supply side of the equation is able to support oil prices or at least prevent them from falling. As reciprocal punitive import measures negatively impact oil demand estimates (not acknowledged yet in monthly forecasts) oil supply is getting a boost from the very same manoeuvre. Buyers of Iranian, Venezuelan or lately Russian crude oil and refined products have been threatened with secondary tariffs. The moves coincide, intentionally or fortuitously, with the OPEC+ decision to go ahead with the gradual unwinding of voluntary supply restrictions from today.

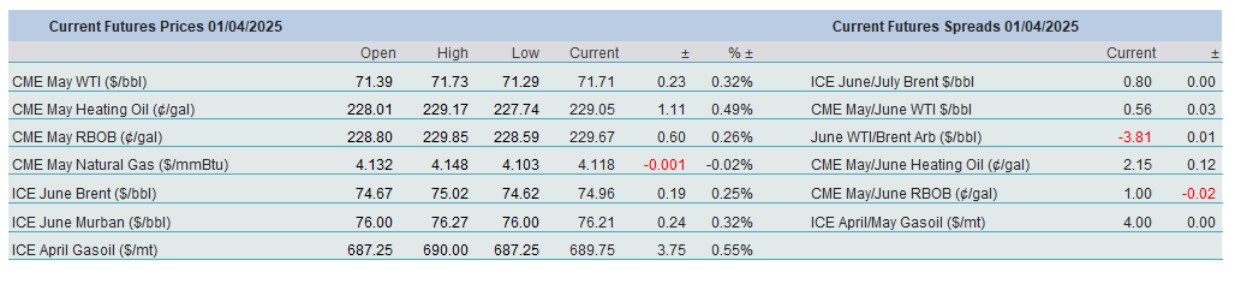

Predicting oil balance, as mirrored in the widely diverging estimates from OPEC and the IEA, is an arduous task. What can, however, be relied on is the view of market players and it was less pessimistic than of those in the equity markets. WTI and Brent finished March 2.05% and 3.10% higher. Brent CFDs, which reflect the future value of the European crude oil benchmark, still show healthy premiums over the forward market. Both WTI and Brent remained in confident backwardation last month. Crack spreads, whilst failing to make meaningful advances, did not weaken either in March. It must also be pointed out that although US crude oil inventories stayed broadly unchanged from February, the major refined product categories declined – gasoline stocks by 7 million bbls and distillate inventories by 5 million bbls.

Oil market participants are facing a million-dollar dilemma. Should they put their faith in eventual demand recovery coupled with tight supply due to sanctions or rising Middle East tension that could potentially lead to the closure of key oil transport arteries or perhaps attacks on oil infrastructures? Or will economic perspectives worsen as excise duties are introduced with the inevitable negative impact on oil demand? It is simply impossible to come up with a convincing conclusion. Yet, it is probably a fair observation that whatever happens, however frequently tariff plans or geopolitical views change one aspect of the current US administration will remain static. That is the detestation of high retail fuel prices. Consequently, our often-mentioned view of limited upside potential must be re-iterated as the first quarter of the year and the first two months of the Trump Administration are now in the rearview mirror.

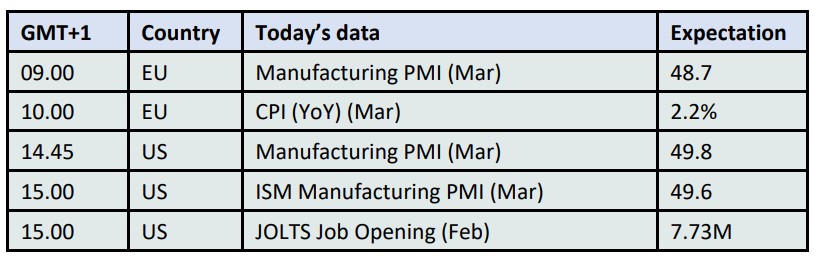

Overnight Pricing

01 Apr 2025