The US may be closed, but it is still the driver

The closing prices of August 25 to September 1 reveal a somewhat disjointed market that is made more confusing by the ensuing price gaps left as the US products underwent an expiry in the front months of Heating Oil and RBOB. The week-to-week changes are as follows; WTI +$5.72/barrel, Brent +$4.07/barrel, Heating Oil –20.25c/gallon, RBOB –28.52c/gallon and Gasoil –$26.25/tonne. The initial rally forged very much by the recent rampant Heating Oil contract and its reliable wing man Gas Oil, was taken up by WTI and Brent and the crudes forged ahead and are now making new 2023 highs. Despite some abject PMI readings that will be touched upon later, the threat of hurricane damage, this time from an unlikely named Idalia (loveable in Greek), sent a palpable shiver through an oil fraternity still very much in the thrall of a tightening narrative and awaiting if Saudi Arabia would indeed roll over its 1-million barrel per day voluntary production cut into October. What then convicted that thought process came from Russia announcing it would release the details of its own continuation in curbs this week, because one does not seem to act without the other at present. This conviction can be seen in the CFTC Commitment of Traders report with managed money increasing their WTI long positions by 19,040 lots.

This morning’s start to proceedings is a sedate affair but one that has carried momentum from last week. With the US enjoying a long holiday weekend, eyes have settled on China and a relief rally currently being felt in the Hang Seng as the pressured property company Country Garden made good on a bond payment while securing an extension on similar debt burdens. President Xi has been about his usual bold and broad announcements of not very much, but the market does appear to have a more receptive and less cynical ear this morning, therefore his promises of support for services sector and relaxing of cross border trade restrictions find sympathy from a market that has fewer drivers with the absence of US participants. Aiding the calmly positive entry into the week is a note from Goldman Sachs over the weekend predicting that the cycle of rate hikes from the Federal Reserve is over which does appear to garner support from market pricing. The FEDwatch tool of predicting interest rates now stands at 93% of a hold in rates at the next FOMC meeting.

PMIs, PMIs and the US

In Friday’s monthly roundup we touched upon the contemporary weak state of the Manufacturing Purchasing Managers Index data from across developed economies and looked forward to finding something from Friday’s ensuing publications indicating a change of fortunes. Judging by how so very far some remain from expansion territory (over 50), one wonders if there is a catalyst powerful enough to ignite seemingly sloth-like world industrials. Chronologically, they disappointed as follows; Australia 49.6, Japan 49.6, South Korea 48.9, France 46, Germany 39.1, Euro Area 43.5, United Kingdom 43, Canada 48, US 47.9 (S&P) and US 47.6 (ISM). Admittedly, a rather laboured list but not as laboured as the activity they represent. For Europe, its historical powerhouse Germany is now suffering stubborn inflation and such poor economic activity that it is proving a wonderful ally for those that are predicting stagflation (inflation plus low productivity) across the continent, possibly being represented by how the Euro/US dollar exchange rate has slid from 1.13 in mid-July to 1.08 COB Friday. As for Asia, South Korea has now registered 14-straight months contraction, much of which is likely the result of a failing China, but as the fourth largest Asian economy and a darling in the eyes of the technology industry, such woeful activity news completes a negative framing of global manufacturing.

Global services PMIs, along with their composites which include manufacturing in its calculation, will be published tomorrow and Wednesday and it has been the service industries that have held the confidence of investors and created commodity derived demand. Wednesday the August S&P Global Services PMI for the US is expected at 51, down from 52.3 in July with the August Composite 50.4 against July’s 52, additionally, and due an hour later is the much more followed ISM August services, previously registering at 50.7 for July. The US data is singled out here because it has been the service sector that the US has relied on, and indeed world investors, for such longevity in job creation with the obvious biproduct being greater wages in the economy and a remarkably effervescent attitude in spending power.

Consumer confidence is set to be problematic after recent readings in the United States. In June the Consumer Confidence Index registered 110.1 with the Conference Board and then 116 for July. Last week, the business research group published a reading of 106 more than erasing those 2-month gains as canvassing revealed US spenders are concerned with the rise in the prices of foodstuffs and gasoline. The Board’s survey went on to say assessments showed receding optimism around employment as fewer consumers said job are plentiful with more saying jobs are hard to get as the average of the number of weeks unemployment is ticking up. On a 6-month moving average basis, plans to purchase cars and appliances were higher but plans to buy houses still trended lower, in line with interest rate worries.

We have deliberately held the US in snapshot for the simple reason that it currently is the driving force in oil price moves. Its influence comes in on a multi-level basis but it all can be tracked back to how consumers and services sector workers, which account for over 70% of the jobs market, currently behave and if that changes any times soon. The US was the first to feel the pinch of a refining sector unable to keep up with oil product demand, which ultimately saw the world scramble for distillate derivatives and securing the foundation from which oil prices have been able to rally. A hurricane finding landfall in California, or the eastern side of Florida should be met with concern as to the human suffering caused, but in ordinary circumstances their effects on oil prices should have been limited. This is not the case because of the sensitivity the world now feels when production of any kind might be possibly interrupted in the largest global oil producer.

Conversationally, and open to argument, is that the introduction of WTI/Midland into the North Sea basket has fast-tracked Midland from being a domestic crude that traders used to be able to give a metaphorical ‘fly-over’ and rendered the US grade the most important in the world, well currently anyway. The fixing of VLCC Forties cargoes with an Eastern destination used to light up the wires and telephone banks of oil traders and their associated media cohorts. Currently, this is now the remit of Midland; how many cargoes are going to Asia, how many to Europe, what the freight rates are and Midland to any grade being the arbitrages that are mostly in vogue.

Purchasing Manager’s Indices globally are so very important on marking the progress of economies. However, the US ought to enjoy special attention, not only because its stock-bourses have propped the confidence of investors, but its economy has similarly aided oil prices. Betting against the consumption power and confidence of the US population this year has borne little fruit, but there is enough data at present that might just change that. A looser domestic market in the US will ultimately allow for greater availability of Midland crude for export, or a continuance in economic performance and sentiment, less, and because of its current importance the logical fall or rise in global crude prices.

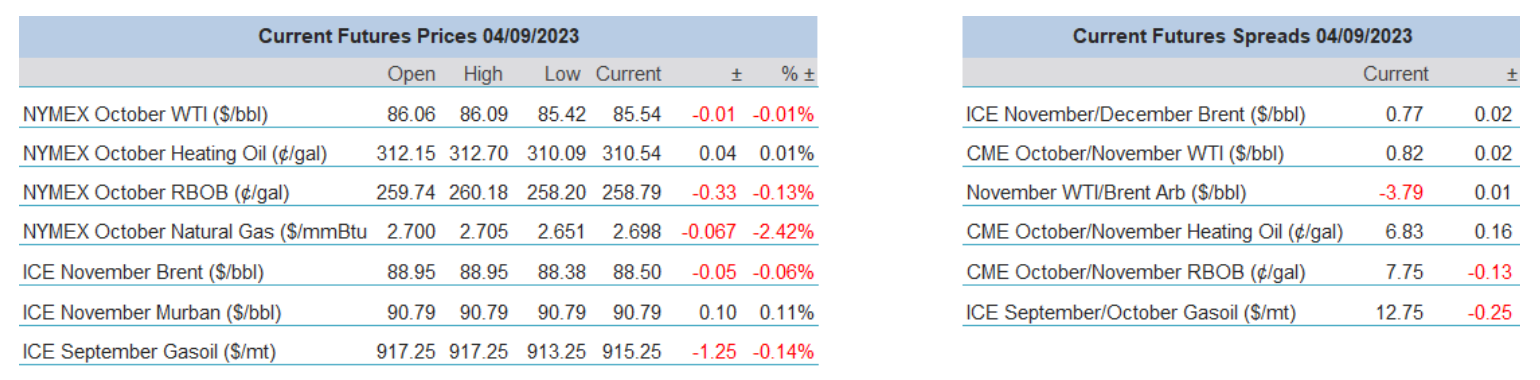

Overnight Pricing

04 Sep 2023