The Volatility of the Probability of Interest Rate Cuts

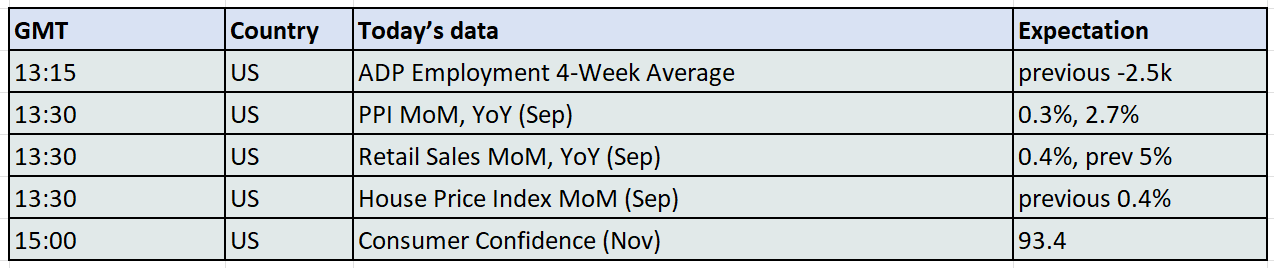

The world is about to play catch up on US data and today sees another bout of metrics from the previous months in which all information sat in the in and out boxes of US government agencies during the shutdown. Patterns are now sought from investors trying to affirm a newfound attitude that there will indeed be an interest rate cut from the US Federal Reserve in December. It may be that market participants are more attuned because of the importance of individual attitudes, but there seems a raised willingness by Fed board members to be verbose in opinion on monetary policy. The latest being Christopher Waller and his leanings for a 25-basis point reduction next month due to the probable weakening of the labour market in the US. Such has been the helter-skelter of the CME FedWatch tool, it has almost become a tradeable asset in itself. One month ago, a quarter-point cut was almost nailed on with a probability of 91 percent, at the front of last week it was pricing as low as 42 percent with the current betting offering an 81 percent likelihood. Each shift in interest rate thinking will continue to bring direct consequence across all suites, particularly the psyche of equity market which having gone through a serious bout of existential analysis is looking for any reason to bring back the bullishness. Given that the trading week will be strangled by yesterday’s Japanese holiday and the end of week Thanksgiving festivities in the US, the two countries most guilty of handwringing over interest rates, the importance of data, be it old or new, is understandable.

Russianisms in a US peace plan

Cycles in geopolitics and or markets seem to be continually coming into nexus or convergence resulting in imagined inflection point or any other word parings that describe situations of cause and effect that potentially bringing marked changes. Such is the headache of the latest bout of negotiations in the Ukraine war where a hurried United States seems hell-bent on breaking the impasse. Will land be ceded, will recognition of stolen lands be granted, will asking for reparations be appropriate, how many military personnel might be allowed and who can be a member of global alliances be they formal or casual? What that this were to be applied bilaterally. Every contention must be addressed by Ukraine, not the aggressor, and when reading the proposal for “peace” (with all the disdain the use of quotation marks derives being intended) it is more akin to Vladimir Putin’s list he might write to Дед Мороз of the North Pole. As much as a sense of urgency is being portrayed from the American sector, the embattled stance of both Ukraine and Russia do not match aspirational Washington bigwigs or that the situation on the ground is about to see a change of fortunes anytime soon.

It is once again a fabulous victory for Russian strategy. It really is not hyperbole to state how Moscow owns the narrative and if one were to doubt such boldness of observation, one only need look at the authoring of the road map to peace being hawked by US diplomats. Many news agencies, and neatly put by the Guardian, believe the plan to be scribed by a Russian hand. The UK daily opines the proposals for Ukraine appear to have been originally written in Russian. In several places the language would work in Russian but seems distinctly odd in English. If true, it is a very worrying development and shows how negotiations are being conducted within a cabal that is not including experts whose job it might be to tidy linguistic anomalies and diplomatic language. Indeed, away from Washington intrigue, it is a both a slap in the face and a scary prospect on how the Trumpers never saw fit to consult European leaders before making merry with a future Russian bear prowling the Old Continent’s borders.

The whole thing is distastefully transactional. After all, the potentates in the US administration, Trump, Witkoff, Lutnick and Bessent are all business people, in case anyone wonders why such an attitude exists in the Administration. Not satisfied with denuding Ukraine of its mineral resource control when Washington snatched part of them in exchange for US military personnel remaining in Ukraine, any monies sequestered when US sanctions entrapped Russian assets will be split 50/50 with US investors and Ukraine. Volodymyr Zelensky has probably only just recovered from the mauling he received in the infamous Oval Office ambush, only to once again hear the words of his showing “zero gratitude” to President Trump, the US leader’s commitment to ending the conflict and the US arms given to strengthen Ukraine military forces. ‘Given arms’ is a stretch bearing in mind only weapons contracts negotiated under Joe Biden having been delivered with other arms sales funded by members of NATO. Trump’s 28-point plan echoes of the 20-point plan he rolled out for Gaza. The process was all about force of personality, of deadlines and threats which could only be made good by the most powerful earthly office.

Why the US Eagle has chosen now to circle the skies of Kyiv is because its keen eye and power would never be allowed above Moscow which has proved impervious to its powerful gaze. Russian lives and Roubles are being frittered no less than that of its victim. Yet it does not have a President subject to democracy and who is made weaker by scandal. Associates of Ukrainian President Volodymyr Zelensky are allegedly involved in a scheme to defraud $100 million from Ukraine’s energy sector. It is manna from heaven for the Russian Department of Misinformation and its chatbots that feed our news algos. Zelensky’s international reputation is being increasingly sullied and with it his vulnerability to being bullied. Not only is Putin pressing on such reputational bruising, so is Trump. The pillaging of Ukraine’s sovereignty under this new proposal would not have been given the time of day a few months ago, but political careers in every country and over all histories prove to be more important than the fate of a nation. Trump smells weakness and with the anniversary of his first year in sight, it can only be imagined how a ceasefire in the two most dangerous wars would be carved in gold in the new White House ballroom.

Every near concession made by Ukraine brings another sell order into the suite of oil trading mediums. And even without Kyiv compromise, the US President shows that he is more an ally of Russia than antagonist. Data sets need time to mature, but sanctions on Lukoil and Rosneft are likely to encumber Russian oil revenues by only a tolerable amount. With India and China set to re-instate themselves as Russian oil customers as and when the US sanctions are worked around, the idea of a world awash with crude is very hard to shake in our community. If it were not so, then Brent would be $70/barrel and not looking to break back down into the high $50s. We still strongly believe the US Administration’s target range of crude price tolerance is $50-$70/barrel, therefore, at these current levels and the low state of volatility, allowing at least a notional solving of the Ukraine war and a ‘welcome back Mister Putin’ into the ranks of accepted oil providers completely fits the American playbook of things that suit them.

Overnight Pricing

25 Nov 2025