The Waiting Game

There are growing concerns about the state of the global economy with bond markets recently under pressure, stocks declining and the dollar in demand. Macro factors, nonetheless, have been swept aside in the last few days as market players solely focused on evaluating Friday’s announcement from the Biden administration on imposing damaging sanctions on Russia and its shadow tanker fleet. As with most geopolitical developments, the gut reaction is usually followed by some consolidation, a period of reflection to gauge whether the impact of the event would be prolonged. In the latest case, it arrived yesterday (with the exception of gasoline, which remained stable because of the closure of the Colonial pipeline), greatly aided by what can be described as a Gaza ceasefire within grasp. If achieved, oil supply will not increase, and the Yemeni Houthis will probably continue atrocities in the Red Sea. The impact of a truce, therefore, is to be brief and the focus will shift back to the US sanctions.

As discussed below, at this stage drawing a firm conclusion is premature and will remain so until the incoming US administration starts dealing with the issue beyond rhetoric. Enforcing the punitive measures effectively will have an inevitably adverse effect on supply and eat into the OPEC+ spare capacity. Loosening or tracking back on them, on the other hand, will ensure adequate supply as echoed in the latest EIA monthly report. It envisages an increase of 260,000 bpd in global stocks in 2025, rising OECD inventories and lower average prices than in 2024. The dust will hopefully quickly settle after the inauguration on January 20.

Bold Move with Ambiguous Effect

In hindsight, the decision from the Biden administration to impose the most severe sanctions on Russia’s oil industry was a smart step. Firstly, it is seen as an elegant move towards the incoming US President as the reference point, on which potential peace talks will be based has been moved in favour of the US and Ukraine; invaluable leverage was provided. Secondly, the possible negative consequences of the sanctions (ie. high oil prices and the resultant inflationary impact) will have to be dealt with by Donald Trump and Co.

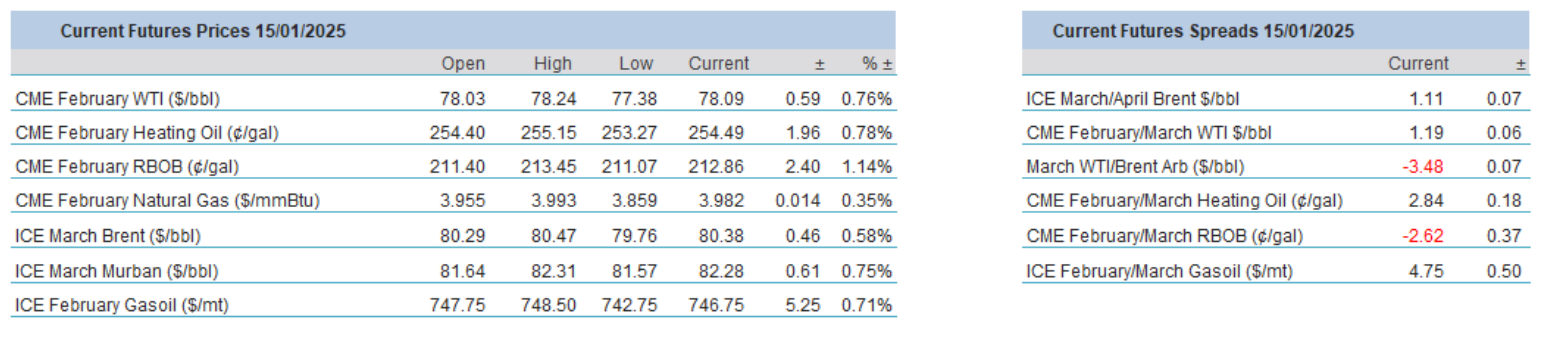

The move's repercussions are twofold. First, it could cut supply, leading to a tighter global oil balance. Second, it is sending freight rates higher. The initial market reaction was one of massive repositioning. In the space of two trading sessions, Brent rallied more than $4/bbl. Trading volumes increased considerably. Before the announcement, on Thursday, January 9, 1.02 million lots of Brent changed hands. It rose to 2.74 million contracts a day later and 2.50 million lots on Monday.

The sanctions understandably affected the front-end of the curve. The premium M1 Brent commanded over M2 rose from 67 cents/bbl on Thursday to $1.36/bbl two days later. The M1/M7 backwardation widened from $2.85/bbl to $5.53/bbl during this period. Speculative shorts frantically covered and those who expect protracted strength started to build up length. Physical players also swung into action as the availability of Russian crude oil (and products) was thrown into doubt. Dated Brent for next week, assessed $1.50/bbl over the April forward contract last Thursday quickly ascended to above $3/bbl by Monday’s settlement.

So, what is exactly at stake? Will supply be disrupted meaningfully and shortage loom large? A rudimentary approach paints an ominous picture. After all, Russian crude oil and product exports exceed 5 mbpd, so the impact of the new sanctions could be grievous. The two biggest Russian oil importers are China and India with a combined daily volume of around 4 mbpd. Reality, however, is more nuanced. Consultancy Vortexa estimates that sanctioned tankers were responsible for shipping around 1.5 mbpd of crude oil and 200,000 bpd products last year.

Indian government officials said that the world’s third-biggest crude oil importers stopped dealing with US-sanctioned tankers. Chinese refiners have also begun their search for alternative supply. In fact, the Chinese port group, Shandong had banned tankers under US sanctions from docking and delivering at its ports before the sanction announcement. Around 65 oil tankers had dropped anchor around the world, including in China and Russia by Monday, according to ship tracking data. Shipping costs are naturally on the rise. Rates on the Middle East-China route rose 39% after the US announcement, Reuters says quoting ship brokers.

The actual and potential impacts are there for all to see. Less available oil and cargoes that carry it are supporting oil prices. Goldman Sachs estimates that Brent could climb as high as $85/bbl in the immediate future if Russian production and exports are materially affected by the embargo. Given the dire straits the Russian economy finds itself in (the war economy is unsustainable and so is the 20%+ inflation), it would make perfect sense for the US to maintain the economic pressure on the invader until it cracks ensuring a considerable fall in Russian production.

There are, however, mitigating factors. Firstly, it is anything but given that the Trump administration is willing to maintain the renewed pressure on Russia for the medium term. Secondly, sanctioned tankers are allowed to discharge until March 12, when the wind-down period ends. Disruption might be minimal if the incoming US president strikes a quick peace deal (although it is unlikely). Thirdly, the OPEC+ spare capacity could fill the supply void precipitated by the latest sanctions. Expect lax OPEC compliance in January and February as buyers should turn to the producer group for help. Finally, and possibly most importantly, prolonged high oil prices will re-escalate inflationary pressure and could lead to higher borrowing costs, something that the Trump government will not tolerate.

Before last Friday, we were of the view that the perceived comfortable oil balance would cap any rally with the top being around $80/bbl basis Brent. Life and the incumbent US administration have rewritten this view. The situation needs to be re-assessed, but the latest development is still fresh, there are many moving parts with a lack of clear direction. It is impossible to predict the precise impact of the sanctions with great certainty. What seems inevitable is that oil prices will come crashing down at one point. When and from where is inconspicuous, admittedly a cynical yet painfully honest conclusion and the most accurate that can be presented at this stage. As Niels Bohr once said, it’s difficult to make predictions, especially about the future.

Overnight Pricing

15 Jan 2025