The War Drones On

Well, that did not take long, did it? The language of negotiation now includes the added lexicon of limited military strikes representing the unacceptability to the terms of whatever current thread holds up the rocky road to peace. The trading of airstrikes, the second time this week, has the US military shooting down Iranian drones and hitting a drone-control station after Iran had allegedly fired attack UAVs at US and commercial shipping, voices from Washington said. Kuwait has reported incoming missile and drone attacks, which lines up with Iran claiming to have targeted a US base in the region. The US President was in a testy mood yesterday and threatened to “blow up” Oman if it fails to “behave” after reports circulated that Muscat and Tehran had been negotiating how they might jointly charge a toll for passage through Hormuz. An irritated Donald Trump normally comes with something being blown up.

Whether or not these trading of airborne nudges act as a reminder of what might happen if an agreement is not met, shows how limited progress is, but at present neither the US nor Iran can afford escalation. Americans are exhibiting increasing dissent toward the war as the mid-term elections loom and within Iran, the financial squeeze and lack of everyday necessities because of the blockade are causing much civil pain. Bombing one’s way to peace is a curious practice in negotiation and normally the craft of terrorists in this strange game of proportionality. Every soul in the world wants an ‘off ramp’, but at present the protagonists are hurtling on and keep missing the junctions. Tweaks, twizzles and the odd explosion will be seen in the language cutting across our screens in many adaptations of something that will not find agreement any time soon.

Confused? You will be

The indestructible stock market roars on and it is impressive indeed bearing in mind the length of time crude oil prices have been spending at $100/barrel, and with it the now undoubted inextricable creep higher in inflation. Markets are going back to school, for the tried and trusted reactions and strategies to meet it are not just shifting in nuance; they are taking great leaps and bounds. The problem for all and sundry is trying to work out the longevity of the current flux and is as clear as when this subsection of a Middle East war might end. In times of yore, when inflation was spotted coming over the hill, then defensive hedges might see length in oil prices and shorts in equity bourses. Imagine then after the outbreak of hostilities on Iran from the US and Israel coalition a risk manager sought the logical strategy of buying say, $150/barrel call options in Brent, and/or buying 6000 put options in the S&P. Such moves would have seen one dumped in a debtor’s prison quicker than Charles Dickens might write ‘Little Dorrit’.

The impressive bearish narrative of the Trump administration and the use of existing inventory to supress oil prices, coupled with the equally stoked furore surrounding A.I. have served to quash the tried and trusted methods of inflation hedging, meaning price rise exposure needs to land somewhere. There has been a real shift in the shaping of yields, that which defines the link between when bonds might mature and where interest rates will be perceived when they do and how higher rates suck the profits from fixed-income investments. Just taking the story within the greatest wealth creator of all, the United States, the 10-year US Treasury yield has recently risen to the highest levels since early 2025. It is also an interesting muse when reflecting on the Mag 7. If their performance is the main global economic driver through their ever-increasing value, then are they not likely to be as reliable an inflation hedge as oil has been in the past?

The world is in a very different financial space from the post-2022 era and is indeed much richer. However, such wealth does not now preclude the worries surrounding inflation that occurred back then due to bottlenecks and the restrictive flow of goods from the Ukraine region, or indeed the weaponizing of oil. As the world emerged from lockdown and faced the illegal invasion by Russia, inflation was defined by widespread shortages in all nature of commodities, whereas up until recently, inflation has been driven by domestic wages and service costs. But the period of “great resignation” when the folks of the world undertook greater risk in their employment has now been replaced by a “job hugger” attitude and not only due to A.I. The World Economic Forum last year warned on the combined forces of technological development, green transition, and demographic shifts are fundamentally reshaping labour markets. This is exacerbated by microeconomic uncertainty and tighter household budgets.

It is to these preconditions that the state of inflation must and should define the next batch of interest rate decisions from central bankers. Yet, even with the almost united front of custodians being in synchronisation after the Covid years and initial outset of the Ukrainian war, a common cause is likely to be attended to in differing decision from the higher echelon of the US Federal Reserve, the European Central Bank, the Bank of Japan, the Bank of England and even the People’s Bank of China.

The Fed is now set to hold rates after there being much expectation of a dovish lean after the appointment of Kevin Warsh as Chair, but he faces an Iran war, tariffs and an A.I. balloon, making it harder to forecast interest rate easing. The ECB is likely to hike, its community is so very much more exposed to energy price shocks, and the central bank has never been shy in firing a hawkish shot across the bows of impending inflation. Yesterday morning, Bank of Japan Governor Kazuo Ueda, said the current energy shock might become more persistent, this is not just the gateway for higher rates, the beleaguered Japanese Yen is in dire need of more than just supportive intervention, it needs a policy to stop its tumble into being another inflationary prop. The Bank of England is so caught up in political mess and government borrowing that it cannot afford to upset the bond or gilt market as it is called, because the UK is in complete hock to these owners of its debt. As for the PBOC, it recently announced it was keeping its 1-year and 5-year Loan Prime Rates at 3 and 3.5 percent respectively. But because of such poor domestic demand and geopolitical concerns, and according to Bloomberg, the central bank has allowed the medium-term lending facility (MLF) to drift as low as 1.45 percent this month in an attempt to inspire any sort of growth.

There is no conclusion to be drawn from this foray into just part of the financial and economic conditions that are a la mode. We seek only to point out how fluid and confounding the future is likely to be. Markets, economies, and those charged with keeping them orderly may only do so when there is a reasonable chance of predicting how geoeconomic and geopolitical events might unfold. But at every corner of interpretation, and at every instance touched on above; they are completely reliant on how the war in Iran will end, if it ever does, and whether any of the moves by markets, by strategy or by central banks currently being dabbled in, will be fit for purpose if a season of normality suddenly breaks out.

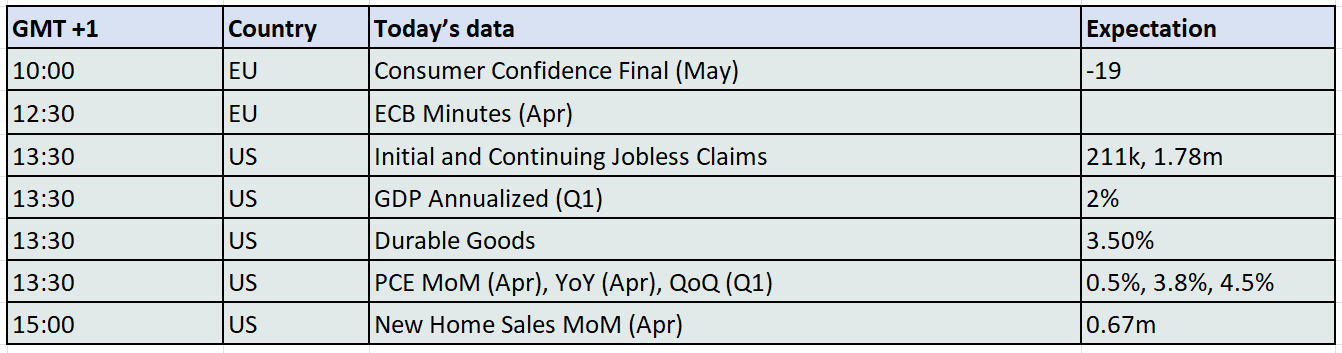

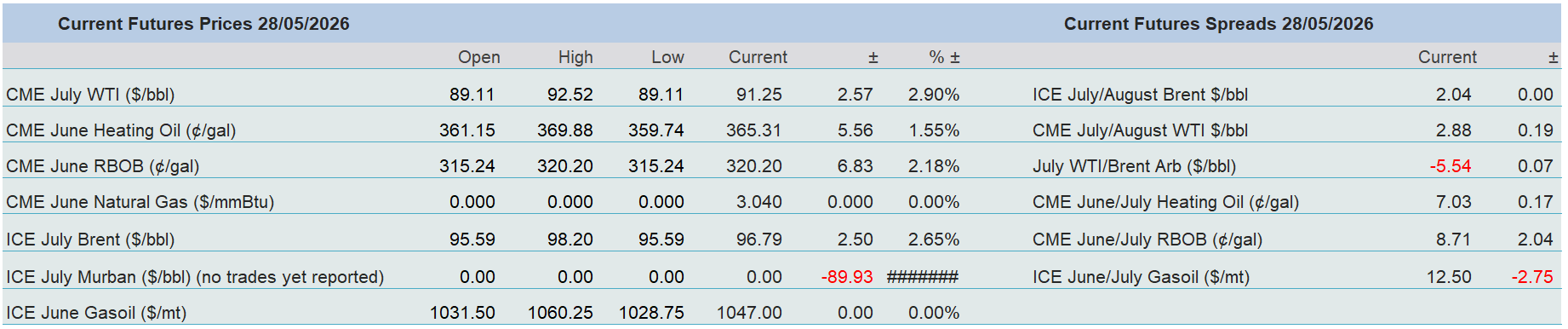

Overnight Pricing

28 May 2026