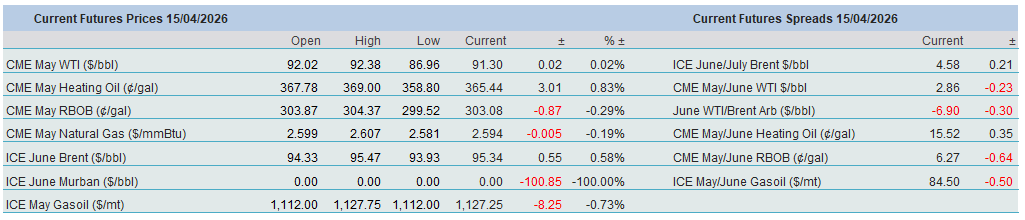

War or Peace

All it took was another announcement by the US President, this time in an interview with the New York Post, that talks between his country and Iran might resume in the immediate future, and markets reacted obediently. Oil was sold off, casually ignoring the fact that traffic through the Strait of Hormuz remains significantly below pre-war levels (10.1 mbpd was lost in March, according to the IEA), and that the US will allow the Iranian oil waiver to expire. We have been here before, and one cannot help but think that the US President, with oil once again below $100/bbl, will feel emboldened to play hardball and re-ignite belligerent rhetoric and actions. On the other hand, an eventual extension of the two-week truce, or even peace, while expected to be fragile and likely broken, will briefly send prices even lower before the realisation of worryingly tight physical markets sets in.

Equity investors were equally sanguine about a successful outcome of the Strait, but not-so-straight talks. The S&P 500 index has now all but regained the ground lost since the start of the war, possibly helped by better-than-expected US PPI data, which still showed an annualised increase of 4% in headline and a 3.8% rise in core producer prices. Inflationary pressure is conspicuously rising, and the IMF, in its latest World Economic Outlook, cut its growth estimates to 3.1% in its reference case (short-lived war) and warned of 2.5% growth in its adverse scenario (prolonged war). By any measure, dark clouds are gathering, but as discussed below, it will take time for potential demand destruction to outweigh the damage the conflict has been causing to oil production, supply, and exports.

Tightness is not Acknowledged in Prices

There is broad and unequivocal agreement among forecasters that the impact of the US/Israel war against Iran, and the response from the Persian Gulf OPEC nation, will result in a sharp tightening of the global oil balance, particularly in the current quarter. What was deemed a supply surplus two months ago has turned into a sizeable deficit. Whether the shortfall in available crude oil and product cargoes will persist into the third quarter and beyond depends entirely on the unconditional reopening of the Strait of Hormuz, whose closure currently prevents around 10 mbpd of oil from reaching consumers across the world.

As highlighted in recent reports, the EIA predicts a swing of around 8.1 mbpd in global stock movements. Pre-conflict, the statistical arm of the DoE envisaged a second-quarter surplus of 3.03 mbpd, which has since flipped into a deficit of 5.09 mbpd. If global oil inventories draw, OECD stocks will inevitably decline as well. Commercial stocks in the developed world are now seen at 2.711 billion barrels, compared to 3.020 billion barrels two months ago.

OPEC, naturally, concurs with this abrupt shift in outlook. It left its global demand estimate for the whole of 2026 unchanged but downgraded its second-quarter projection by 500,000 bpd. Demand for the second half of the year, however, was revised upwards. That said, if prices remain elevated for longer than anticipated, reassessing these projections will be unavoidable. Changes in demand, nonetheless, pale in comparison to fluctuations in production, particularly in OPEC output. One need look no further than the March estimates from secondary sources. The 12 member states collectively produced 28.67 mbpd in February and 20.79 mbpd in March. The four Gulf producers bore the brunt of this decline: Iraq (-2.56 mbpd), Kuwait (-1.37 mbpd), Saudi Arabia (-2.31 mbpd), and the UAE (-1.53 mbpd). Assuming second-quarter OPEC+ output of 36.6 mbpd, 5.3 mbpd lower than in March and 7.4 mbpd below the February prognosis, global oil inventories are expected to decline at a rate of 5.2 mbpd, compared to a predicted build of 1.8 mbpd in February.

Both the EIA and OPEC project annual demand growth this year: 590,000 bpd and 1.32 mbpd, respectively. In their view, consumption will either prove relatively resilient to high oil prices or the current tightness will not be prolonged. Conversely, the IEA now expects global consumption to contract, as the price spike is likely to dampen demand. This contraction is estimated at 50,000 bpd, compared to the projected growth of 1.18 mbpd in March and 900,000 bpd in February. Bearish enough? Not quite, as the hit to OPEC+ (i.e., Persian Gulf OPEC producers) supply significantly outweighs that to global demand, especially in the second quarter. The downward revision for the full year between February and April is 3.5 mbpd, and for the second quarter it stands at 9.1 mbpd.

To fully grasp the severity of the Iranian crisis, it is useful not only to examine absolute OECD stock levels but also to assess them in terms of demand, that is, how many days of consumption they can cover. The EIA expects a 6–7 day decline for both the second quarter and the whole of 2026 from its February projection, from around 67 days to 60 days. OPEC anticipates an even more pronounced impact, forecasting a drop of nearly 9 days, from 64 days to 55 days, an alarmingly low level.

The bottom line, at least in our view, is that the Iranian crisis has reignited concerns about global energy security. It is likely to lead to increased investment in both oil exploration and production, as well as renewable energy. This represents a double whammy for those who had anticipated a significant demand surplus toward the end of the decade. In the near term, however, the market remains tight. Forecasts for the current quarter suggest that competition for available barrels, both crude oil and refined products, will remain intense in the coming months and possibly beyond, unless a solid and reliable agreement between the US and Iran is reached promptly. While demand growth may soon begin to falter, the loss of production and exports is expected to far exceed any demand weakness in the short to medium term, ensuring a yawning gap between demand and supply and, consequently, elevated prices, possibly higher than the current levels, at least in the second quarter.

Overnight Pricing

15 Apr 2026