A Week of Futile Diplomacy

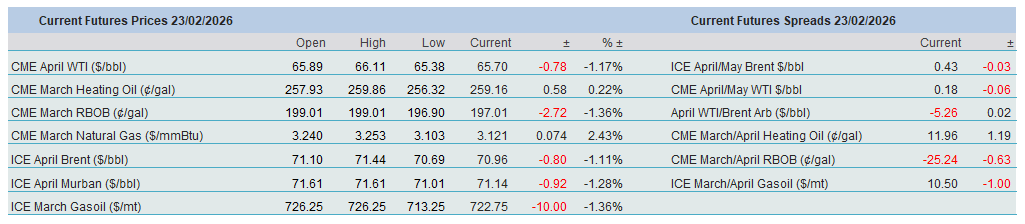

A huge amount of ink has been spilt recently describing the perpetually evolving state of affairs in the two global hotspots that keep the oil fraternity on the edge of its seat. Last week’s events imply that the focus will firmly remain on Ukraine and Iran in the foreseeable future. The two major crude oil contracts, WTI and Brent, rallied to their highest levels since last July and clocked weekly gains of 5.5% and 6% respectively. An unmistakable sign of geopolitics being the dominant driving force is deeper Brent backwardation and a steeper WTI discount at the front end. This so-called box trade, front arbitrage versus longer-dated contracts, will only provide a buying opportunity when tensions surrounding pivotal oil-producing regions abate, something that does not appear imminent at present. The crude oil benchmarks were outmanoeuvred by the CME Heating Oil and the ICE Gasoil contracts, which both registered weekly gains of around 9%.

So, how long will investors have to remain preoccupied by events in these two nerve centres? As far as Iran is concerned, by the end of next week, if President Trump is to be believed. The US bottom line is that Iran must not possess nuclear weapons, something the Islamic Republic refutes. We argued two weeks ago that the US is unlikely to launch a military assault on Iran prior to the midterm elections, as doing so would amount to self-harm in the form of rising domestic gasoline prices. Considering the recent escalation of tensions and the lack of tangible progress in negotiations, this view must be revisited, and military intervention, the odds of which are put at 65% by April, according to consultancy Eurasia Group, cannot be ruled out.

If it does happen, the question is what shape and form it would take. The range of possibilities is wide. The declared aim is to deprive Iran of its nuclear capabilities; however, judging by President Trump’s words of encouragement during last month’s mass protests against the country’s leadership, regime change might well be the ultimate objective. This could, in theory, be precipitated by strikes on the Islamic Revolutionary Guard Corps, leading to a peaceful transition to democracy. History, however, offers little support for this scenario. Attempts to implement Western-style democracy failed spectacularly in Iraq and Libya. A regime collapse might be followed by military rule, the BBC contemplates, or, if the conservative leadership survives, it might moderate its hard-line policies.

US aggression could also be met with retaliatory moves. Attacks on US forces, Israel, or Arab nations in the region would pour more fuel on the fire. The most devastating option, from an oil perspective, involves the Strait of Hormuz, a critical chokepoint for oil transit. Mining this pivotal shipping lane or launching drone attacks on tankers would have a profound impact on roughly 20 mbpd of crude oil and product shipments, with unpredictable consequences for oil prices. Should transit be significantly disrupted, the middle of the barrel would be most affected, as laid bare by last week’s jump in Heating Oil and Gasoil. Energy Intelligence (EI) points out that around 400,000 bpd of diesel passes through the strait (as does a similar volume of jet fuel). The situation remains fluid; the market will be left guessing, apparently, for the next week. Yet one cannot help but wonder whether Iran would have been promoted to the top of the geopolitical agenda, had the US not abandoned the 2015 nuclear accord during the first Trump presidency.

Peace remains elusive in Ukraine as well. What was meant to be a blitzkrieg in 2022 has turned into trench warfare. Soviet troops managed to advance further, to Berlin, to be precise, in a shorter period during WWII than the territorial gains the Russian military has made since 2022. Russia is adamant that it will continue fighting until its maximalist demands, including control over a large portion of Ukrainian territory, are met. Its reluctance to move closer to a ceasefire, truce, or peace deal might seem perplexing in light of the dire straits of its economy. The budget deficit is widening, domestic consumption is falling, and the country’s oil and gas revenues have halved year-on-year. Or perhaps, as some conclude, the very reason for Russia’s recalcitrance is that its war economy is keeping the country on life support, and ending the conflict would trigger a brutal economic shock, leading to unprecedented discontent with the incumbent government.

International sanctions appear to be taking effect; finding willing buyers for its energy products is proving progressively more cumbersome. Therefore, constant or periodic oil price support, also as a result of reciprocal strikes on energy installations, will likely persist until a credible truce is struck, possibly due to US pressure, the timing of which could coincide with the end of its engagement with Iran.

SCOTUS Strikes Down Tariffs

Persistent uncertainty in major oil-producing regions unsettled equity investors last week. Coupled with mixed economic data, share prices failed to gain traction similar to that seen in recent weeks. The US job market appears solid; on the other hand, fourth-quarter economic growth of 1.4% was almost shockingly disappointing. Inflation, as measured by the core PCE index, ticked up to 3% in December from 2.8% in November. The key takeaway from last week’s data set is that lowering interest is not economically axiomatic.

Whatever view one takes on the state of the US and the global economy, it was quickly forgotten by Friday afternoon after the US Supreme Court rejected the administration’s universal tariff policies. Chief Justice John Roberts argued that “We claim no special competence in matters of economics or foreign affairs. We claim only, as we must, the limited role assigned to us by Article III… Fulfilling that role, we hold that IEEPA does not authorise the President to impose tariffs.” The ruling undoubtedly caused euphoria among US importers and foreign exporters, as well as visible and predictable outrage within the US government. President Trump immediately threatened to impose a blanket 15% excise duty on global imports.

The Supreme Court’s decision will be examined in greater detail in a forthcoming note. For now, however, there are too many variables to consider — what practical steps the administration will take, how trading partners will react, and how and when the reimbursement of already collected tariff revenue will occur, among others. At this stage, it suffices to say that the rare Supreme Court rebuke is a major blow to the US President’s economic agenda. Yet, judging by the late rally in US equities, it might turn out to be a blessing in disguise ahead of the midterm elections, as it could help ease the affordability crisis if it is adhered to. When we asked our Magic 8 Ball whether the US government would feel inclined to comply with the ruling, the answer was: do not bet on it.

Overnight Pricing

23 Feb 2026