What News from Camelot?

It is rather ironic how this week saw President Trump’s first 100 days in office coinciding with the 50-year anniversary of the satirical film ‘Monty Python and the Holy Grail’. One is a spoof on the Arthurian legend where a nonsensical Camelot populated by bungling Knights of the Round Table who sally forth with a mix of ineffectual or damaging edicts, ridiculous choices in battle and contempt for its peasants, and the other, please choose which, is the American government. Yesterday’s market moves were directly attributable to Washington’s attitude in foreign policy. Cancelling the nuclear talks with Iran due in Rome this weekend, the US President announced a desire to bring secondary sanction on any nation or individual conducting oil purchases from the Islamic Republic. Oil participants had started to settle into the idea of a negotiated settlement culminating in Iranian oil being once again available and tradeable. Bearing in mind the forthcoming increase in OPEC+ production, see below, the 1-1.5mbpd from Iran in exports ought not to have such a rallying effect on oil prices, but after a week of crushing falls, it was a kicker to relief and aided more importantly by what seemed to be glimmer of light from Beijing in trade war negotiation.

Yesterday, China at last fully admitted that approaches from the United States were indeed ongoing and it is currently assessing proposals by the United States to begin trade talks, and this morning a Commerce Ministry official said, via CNN, “The tariff and trade war was unilaterally initiated by the US, and if it wants to negotiate, it must demonstrate genuine sincerity.” Whether or not this descends into a who goes first in a calming of tariffs remains to be seen, but for now and at the end of a first quarter riddled with ill will and collapsing markets, investors are in the mood to cling to anything. Along with oil prices, US bourse futures are trading much higher along with Hong Kong’s Hang Seng, but corporate results serve to act as a counter. After yesterday’s encouraging earnings from Microsoft and Meta, two of their Magnificent 7 counterparts joined together in caging any further upswing in stock markets. Amazon fell after hours on missed cloud revenue forecast, but along with Apple warned on extra costs caused by tariffs with the phone maker warning trade difficulties will add $900 million to second quarter costs.

Saudi grasps the nettle of oil reality

It cannot be anything other than inevitability in which Saudi less than surprised everyone with an almost admission more OPEC+ oil will be seen making its way to market very soon. The real dam buster came last month when it was announced, in surprise, the cartel and allies had decided on increasing supply by 411kbpd starting in May. What is interesting is how this semantic variation of the ‘OPEC leadership’ decision is now one of Saudi’s alone and arguably outlines the Kingdom’s frustration with its oil producing brethren and willingness to be more than just a de facto head. The last decision by the OPEC leadership to accelerate May oil production was to fire a shot across the bows of the serial cheaters Russia, Iraq and Kazakhstan. Whatever intricate and barely believable woven explanations that it was to enable quota busters to make recompense on their misdeeds almost immediately misfired. When the newly appointed Energy Minister of Kazakhstan said the country would prioritise national interests over those of OPEC+ when deciding production levels, it made an absurdity of not only reparation but any future plans that might entail holding back OPEC production to protect prices.

A Saudi step away from consensus management can now be viewed as a long-term change of mind on oil production planning. Reuters reported that Saudi Arabian officials have been telling allies and industry experts that the kingdom can endure a sustained period of depressed prices. Such a strategy shift heralds a change in Saudi’s recent role in which it has for several years sacrificed its own oil potential and income in the vanity of trying to not only keep a sheen of cooperative behaviour within OPEC+ but also to keep oil prices higher. The oil hierarchy of Riyadh are cool operators and to underestimate their knowledge of markets is an injustice. The backdoor feeding to the market of a new path is most definitely planned, not some favour to a friendly diplomat or hack. It prepares the market for what is to come and allows incremental price adjustments rather than $10/barrel fallouts. The next time an OPEC+ increase is decided on by whatever future Joint Ministerial Monitoring Committee (JMMC) there will be, it will be a rubberstamping of what has been previously leaked and ‘priced in’ by markets.

Grabbing the reins of the unruly team that pull this cart of oil producers along is not the only motivation for Saudi. For too long market share has been sacrificed with little sympathy and few scruples being displayed by those outside the Declaration of Cooperation. The United States has not been bashful in claiming the biggest producer in the world moniker and the lofty oil aspirations of others from the Americas is all too plain to see. Guyana is now estimated to be producing over 600kbpd and according to an ExxonMobil report at the end of March, this will double to 1.3mbpd by 2030. For all the trials and tribulations facing Canada and its oil space problems in navigating the Trump tarifflippery, oil income is such that investing in pipelines that do more than just feed the United States are forever being investigated enabling its desirable heavier crudes to make intercontinental journeys. Not to be ignored are Mexico and Brazil, therefore the ‘inevitability’ opened with here facing Saudi is not a ‘truth’ but hard to be argued against. This measured return of oil precludes the 2020 dramatic Saudi sulk where the teaching of a lesson to overproducers hurt everybody, including the Kingdom itself, by collapsing M1 Brent futures to $15.98/barrel will be avoided. But as Saudi has said, it is prepared for a prolonged period of lower oil prices and if the leader of OPEC is thus predisposed, then so should we all.

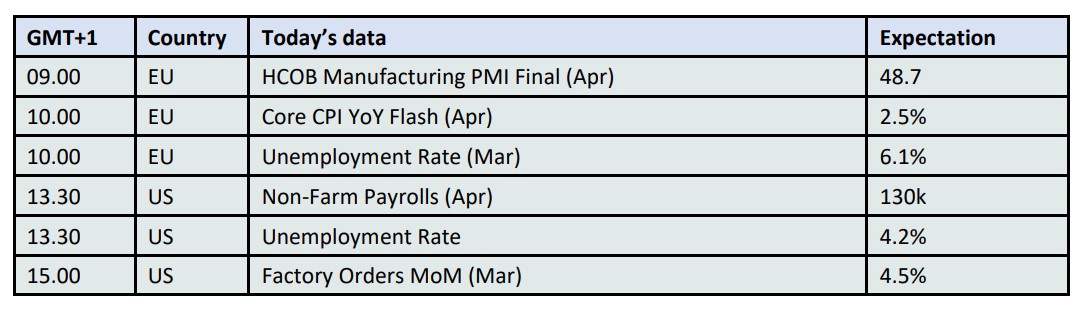

Overnight Pricing

02 May 2025