Who and What to Believe?

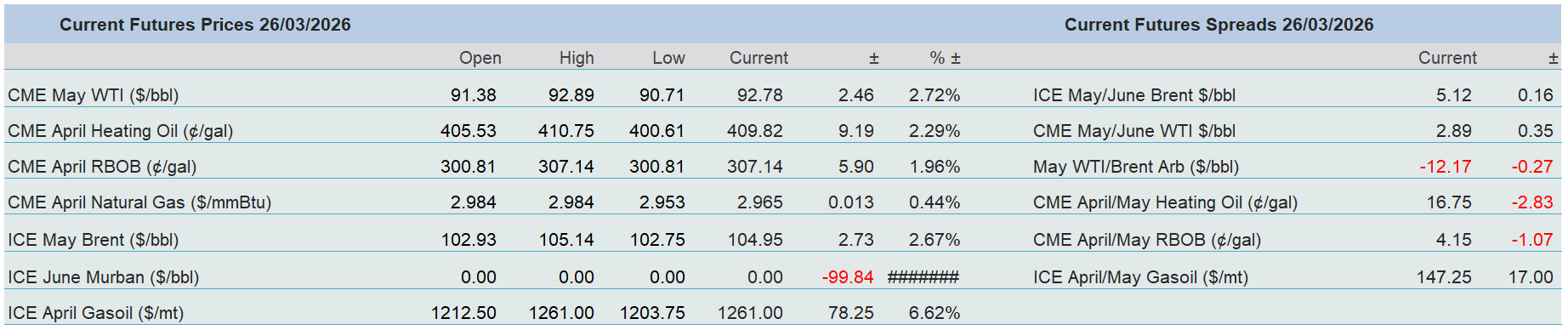

Oil prices took an early breather this morning, although by the performance of Gasoil futures, it looks as if diesel did not get the memo and inspires the rest of the complex to once again rally and doubt the US framing of current negotiations. President Trump in all the magnanimousness he could muster, granted Iran a further ten days to agree to the terms set out in the US offer of a ceasefire, and civilian power supply targets would be left be during which Trump expected Hormuz to be opened.

Markets are edgy across the vast suites, and with the deployment of first-wave, beachhead soldiers by the US, investors are rightly guarding against a weekend operation, which has been the favoured time for new military initiatives by the joint forces of Israel and the United States. Reports congregate around the number 5,000 for marines and paratroopers being readied for action, which if correct, is hardly the size of force needed to take control of a vast country such as Iran. Therefore, and inarguably logical, if the world sees Kharg Island suddenly developing its own form of illegal immigrants arriving in dinghies over the weekend, there will be little surprise.

Poor taste in humour aside, there are conflicting reports in the press with the WSJ quoting a Pentagon source on how the US is considering sending a further 10,000 ground troops. Whereas Axios is reported as quoting a source that Iran representatives could meet for talks in Washington this weekend. All the time the US President sounds off on Iran wanting a deal, the Iranians are still publicly saying that the US fifteen-point plan is one-sided and unfair.

What is evident for our market is how the Strait of Hormuz will not be opened any time soon, and if by some miracle it does, the backlog and backwash of damage and traffic will hardly clear. The effect makes Iran currently a superpower in economic terms. Yesterday, and because of the shipping bottleneck, the Organisation for Economic Co-operation and Development cut its global GDP forecast from the 3.3 percent of last year to 2.9 percent for 2026. Worryingly for inflation watchers, the OECD predicts that inflation within the G20 will push on by 1.2 points to 4 percent this year.

Economic damage is contagious

The damage suffered at Ras Laffan, the major production hub for LNG in Qatar, which will have an estimated repair time of five years, according to Qatar Energy, highlights the wider ramifications of the current Persian Gulf crisis. Staying in the remit of LNG for the moment, there was an excellent insight from Reuters yesterday highlighting how Iran's blocking of the Strait of Hormuz, which handles 20 percent of global LNG flows, with damage to Qatar's liquefaction trains and the sidelining of 12.8 million tons per year of LNG for three to five years, have prompted consultancies S&P Global Energy, ICIS, Kpler and Rystad Energy to cut global supply outlooks by as much as 35 million tons. Taking this into the wider account, any shortage of LNG will cause a self-fuelled spiral in energy prices, particularly that of crude and its refined burning products because there will most certainly be a bout of fuel switching.

Those involved in energy pricing, particularly importing nation states, are coming to terms with the possibility of elongated disruption to supply. Trying to solve energy communication might have an easy remedy in the spare capacity of OPEC members, but as most of the cartel’s supply is locked up behind the Strait of Hormuz, its consideration is void. As storage tops out and well-heads shut in, they become even more susceptible to an Iranian drone and vulnerability can only price one way. The loss of life in this current swipe at humanity is tragic, but the pain is not localised. Soaring price rises are the new pandemic, and the peoples of the world are becoming increasingly affected or even, infected. Pain has arrived swiftly in Asia as some 90 percent of fuels transiting Hormuz have Eastern destinations. Markets are delivering a double whammy as the flight seen in stocks, bonds and Gold have found destination in the US Dollar, therefore, not only is the commodity higher in price due to retarded supply, but it is also made even more so with the unwelcome devaluing of local currencies versus the benchmark.

The latest Asian economy to feel this double jeopardy to its economic wellbeing is Thailand. Prime Minister Anutin Charnvirakul has little choice other than to slash existing subsidies for refined fuels. The effect was immediate and yesterday Gasoline and Diesel prices shot up by 22 percent. According to The Edge of Singapore, the increase marks a turning point for Thailand’s long-standing fuel-subsidy regime, introduced in the wake of the 1970s oil shocks. The Oil Fuel Fund, designed to stabilise and subsidise domestic prices, has seen its deficit widen as global crude costs climbed following the war in Iran, forcing the government to scale back support. The Thai Baht has weakened nearly 6 percent in the last month against the US Dollar and outlines the crippling effects this war is having on countries far and wide.

This is indeed a pandemic and there have been some quite alarming warnings for Europe. There are opinions suggesting restrictive practices designed to decrease the use of fuel in Asia will not stay in that continent alone. Quoted in the Daily Telegraph, Wael Sawan, Shell’s chief executive said this week in Houston, “It is a ripple effect […], we see south Asia first to get that brunt, that moves to south-east Asia, north-east Asia and then more so into Europe as we get into April.” He is not alone in suggesting that Europe must start to bring in supply-side measures, but if that means hunting for alternative supplies then the competition can only send prices higher.

Without coherent strategy from the Trump Administration when this war might end, the ability to catastrophise, be it real or perceived, will increase with time, and the longer this assault on every market’s senses lasts, the more doomsaying it will inspire. Until, the ultimate killer of energy price rises, namely demand destruction, rears its catastrophic head. What a dreary thought going into the weekend.

Overnight Pricing

27 Mar 2026