Whom to Believe?

It is a well-known and widely accepted mantra that the best traders, by and large, thrive in a volatile trading environment. However, as it turns out, there are several types of volatility, and yesterday’s violent price movement was nothing short of unmanageable. It is beyond comprehension how anyone, perhaps apart from flies on the walls of conference rooms in Geneva hotels, could have successfully ridden the wave of uncertainty precipitated by the Iran–US nuclear talks.

This is the part where the previous day’s major events are listed, with an attempt to assess how they might influence future price movements. Well, we will sheepishly pass on the prediction part and, admittedly and somewhat arbitrarily, present our take on the roller-coaster price ride that characterised yesterday’s trading.

The early morning weakness was probably the result of Iran trying to offer a sweetener to the US in the form of investment opportunities in its oil and gas reserves, as reported by the Financial Times, possibly in return for a lenient approach to uranium enrichment for peaceful purposes. Brent dropped by $1.5/bbl.

The ensuing rally was most plausibly triggered by disappointing remarks from the US delegation, citing a lack of progress and a recalcitrant attitude on the Iranian side. From low to high, the European crude oil benchmark rallied by more than $3/bbl amid elevated fears of military intervention.

By the end of the day, the mediator, Oman’s representative, calmed nerves by concluding that significant progress had been made during the talks, without elaborating. Whether “significant progress” means that the US will further delay, but not call off, a potential attack, despite its unilaterally imposed deadline for striking a deal, which expires shortly, remains unclear. According to Oman’s foreign minister, technical talks will resume next week in Vienna.

That is yesterday in a nutshell. As it turns out, after such a chaotic session, we feel tempted to offer a prediction, an honest one: we have no idea which direction the next $10/bbl move will be. However, hectic, headline-driven price swings are likely to remain the defining characteristic of oil trading until either a US–Iranian embrace or an irreversible fallout.

State of the Union, State of the Economy

Tuesday’s State of the Union address had everything the MAGA heart desired. It is usually meant to include reports on the nation’s budget and the economy, and to outline policy goals and legislative priorities. Traces of these plans and goals were apparent in the speech, but it was undeniably a campaign-style event about the achievements of the incumbent administration, sprinkled with superlatives and self-praise. If a personal observation is allowed, it was reminiscent of addresses by communist party leaders and officials during the 1980s in Eastern Europe, frequently interrupted by carefully choreographed yet supposedly spontaneous plaudits and standing ovations, only for people to joke afterwards about the inverse relationship between the length of the speech and the state of the economy, strictly within the confines of their flats or houses.

So, is the US economy as splendid as presented on Tuesday, and has the “turnaround for the ages” really arrived for the benefit of every US citizen? In all honesty, notwithstanding the cynical remarks above, the picture is far from discouraging, but it is not buoyant either. A good starting point would be the results of the latest polls on the popularity of the US administration. Approval ratings are usually reliable indicators of the electorate’s mood, and since voters predominantly check their wallets and bank account balances before delivering their verdicts, the latest polls are not aligned with the upbeat and, arguably, misleading assessment of falling inflation and rising wages. Averaging partisan pollsters from both sides, the President’s disapproval rating is around 40%. That is high.

The actual economic backdrop, nonetheless, based on available data, is more nuanced. US economic growth has beaten expectations. Although the 4Q 2025 estimate of 1.4% came as a mild shock, it was largely due to the 43-day government shutdown, which considerably curtailed government spending. Significant improvement is anticipated when the 1Q 2026 figures are released. Expansion will be spurred chiefly by tax cuts and AI investment.

The trade deficit, which ballooned in early 2025 as importers front-loaded orders to beat the newly announced tariffs, narrowed significantly in the latter half of 2025, only to widen again towards the end of the year, registering an annual gap of $1.2 trillion between imports and exports. Yet customs revenues soared from under $10 billion last January to close to $30 billion a year later. This explains why Trump antagonists find “the affordability crisis” the most potent weapon against the President; after all, these import taxes are ultimately paid by the US consumer. Inflation, as my colleague outlined in yesterday’s note, remains a major concern.

The achievements and the outlook are mixed, something the US stock market corroborates. The President’s claim that “the roaring economy is roaring like never before” is blatantly exaggerated. It is curious, and possibly ominous, to observe that, despite US equity indices hovering around historic peaks, cracks are beginning to appear. The MSCI All Country Index, which is heavily skewed toward US equities, has performed better year-to-date in both 2025 and 2026 than either the Nasdaq Composite or the S&P 500. This suggests that although money is not flying out of US stocks, no significant new money is arriving either. Investors appear to see better returns elsewhere. One wonders whether yesterday’s tech sell-off signals the loss of confidence in the AI sector, which would remove a key pillar of support from US equities.

While the US economy is not robust, it remains resilient, for now. This is mirrored in the domestic oil demand outlook, as seen in EIA data. Although oil consumption has struggled to convincingly return above the pre-COVID level of 20.5–20.6 mbpd, at least demand is not contracting. The 2024–2025 growth rate of 210,000 bpd slows to 20,000 bpd this year and 70,000 bpd in 2027, according to the latest findings.

If one were to label the state of the US economy as precarious, the President’s nearly two-hour-long State of the Union speech offered little encouragement. It is worth underlining that it was delivered just a few days after the Supreme Court ruled the emergency tariff regime illegal. Possibly for this reason, President Trump was at pains to reinforce his economic creed of numerical simplicity: deficits are bad, surpluses are good. A contraction or recession may be implausible, but the stubborn economic agenda, together with confrontational foreign policies, may ensure that the US slowly, albeit gradually, loses its status as the preferred investment destination.

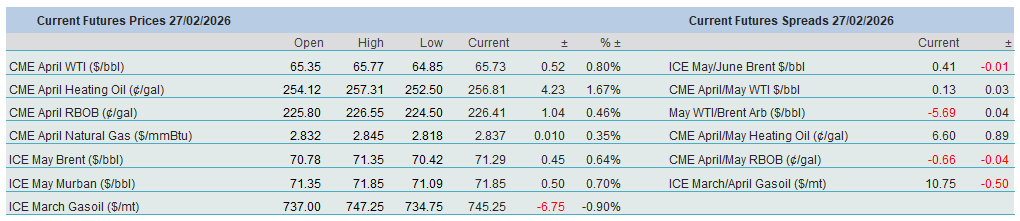

Overnight Pricing

27 Feb 2026