Widening Conflict

Every week that passes makes the nature and the contours of the Iranian war ever more unequivocal. Now that the conflict has entered its fifth week, the political, economic, and oil market consequences are becoming clearer, and the outlook is discouraging. The end is anything but nigh, and whilst hoping for the best is human nature, expecting the worst is common sense.

Adversaries and Allies

Among the three major participants in the war, it was a choice on the US side, but probably a necessity for Israel and Iran. A director at the National Counterterrorism Centre noted in his resignation letter in the middle of the month that Iran had posed “no imminent threat” to the US; yet the US President, possibly still feeling the sugar rush after the capture of the former Venezuelan dictator, decided to give the green light to the joint operation against Iran. The consequences were greatly miscalculated, and the US is now unlikely to withdraw its troops from the region in the foreseeable future, as doing so would mean losing both face and the war.

Israel saw an unmissable opportunity to take a giant leap toward its ultimate objective: removing Iran’s feeble ultra-conservative leadership with US support. Over the last two to three weeks, however, the Jewish state has reportedly conducted military operations without coordinating with its long-standing ally. The latest and most troubling example was last week’s attacks on Iranian nuclear sites. The US–Israel alliance could eventually weaken in the medium term.

The war poses an existential threat to the Iranian regime, and consequently, it feels entitled to take whatever measures it deems necessary to protect itself. The most significant leverage is the potential blockage of the crucial trade artery, the Strait of Hormuz, along with attacks on the region’s energy installations. The conflict widened over the weekend as one of Iran’s proxies, the Houthis in Yemen, was drawn into the hostilities, firing missiles at Israel on Saturday. Disruptions to maritime traffic through the other pivotal chokepoint in the region, the Bab al-Mandab Strait, must not be ruled out.

Recession, Inflation, Stagflation

Wars tend to harm economic growth. Given the strategic importance of the Strait of Hormuz, various economic indicators have deteriorated alarmingly. Private business activity across the globe has slumped amid the ongoing conflict, perhaps the first sign of the broader economic damage it may cause. The eurozone PMI fell to a 10-month low; in the US, business sentiment reached an 11-month nadir; Australia’s PMI showed contraction at 47; and Japanese private-sector activity also slowed considerably in March.

The European Central Bank revised its 2026 growth forecast from 1.2% in December to 0.9%. The Fed Chair, Jay Powell, warned of rising consumer prices due to higher energy costs, while the Bank of England underlined that a severe energy shock would feed into prices across every segment of the economy. The OECD, in its latest report, highlighted the potential damage the Middle East crisis could inflict on the global economy, revising growth forecasts for advanced economies downward and warning of supply chain disruptions in the event of a prolonged conflict.

Inflation expectations are indeed rising. The US 10-year Treasury yield climbed from below 4% at the beginning of the month to 4.48% on Friday. Investors are rapidly reversing their rate-cut expectations. In the eurozone, for example, markets now anticipate two rate increases this year in an effort to tame inflation. Stagflation appears to be a realistic outcome of the war. It is therefore no surprise that global equity indices remain significantly below their February closing levels, with the Far East, most dependent on Middle Eastern energy, bearing the brunt of the decline.

Complacency or Not, Oil Looks Cheap

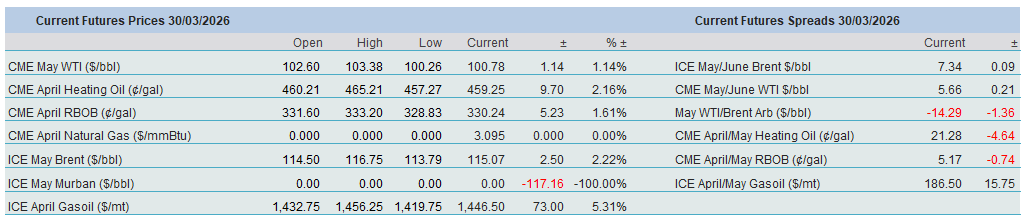

The opposite trend is observed in energy prices. The lion’s share of Middle Eastern oil flows to the Far East; therefore, the impact of any closure of the Strait would be felt most acutely there. The European crude benchmark, Dated Brent, has risen by just under $40/bbl month-to-date, while its US counterpart, front-month WTI futures, is up $32/bbl in March. Murban futures gained $45/bbl after peaking at $160.50/bbl a week ago. The front-month Dubai EFS premium skyrocketed from $1.50/bbl at the end of February to over $12/bbl last Friday.

Mitigating measures do not appear to be working. Saudi Arabia is using the port of Yanbu to move as much oil to market as physically possible, yet Brent prices remain well above $100/bbl. SPR releases have not had the hoped-for impact. Lifting sanctions on Russian and Iranian oil has also failed to produce a meaningful effect. Instead, the US is now effectively funding Russia’s war effort against Ukraine. Mediterranean Urals crude has jumped from below $50/bbl on February 27 to well above $100/bbl last Friday, with its discount to Brent narrowing from $29/bbl to $8.50/bbl. In an even more bizarre twist, the US, having designated Iran a State Sponsor of Terrorism in 1984 and the Islamic Revolutionary Guard Corps as a foreign terrorist organisation in 2019, is now indirectly supporting these foes by temporarily waiving sanctions on Iranian oil exports whilst simultaneously waging a war against them.

Estimates vary, but even a conservative assumption that 10 mbpd of crude oil and refined products have been stranded due to the conflict implies roughly 300 million barrels over a month, nearly three days of global consumption. This is a substantial volume, and with each passing day of restricted flows, the situation becomes more dire. Even if a truce or peace agreement is reached, normalisation would take months, something that appears unlikely in the near term, particularly as the US deploys additional troops to the region.

Further price increases cannot be ruled out, nor can an escalation of tensions. Neither the US nor Iran is likely to emerge as a clear winner. Prospect theory suggests that in disadvantageous situations, risk aversion diminishes significantly. If the US were to launch a ground invasion of Iran, possibly taking the Kharg Island, or if Tehran were to intensify retaliatory strikes on energy infrastructure or fully close the Strait, projections of $200/bbl oil will not be an otherworldly supposition anymore.

Overnight Pricing

30 Mar 2026