Will Tomorrow Prove Iranian Judgment Day?

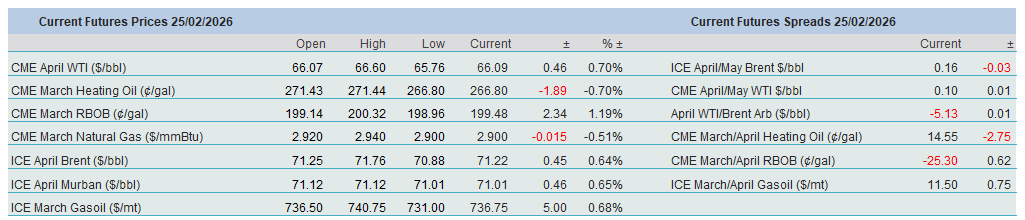

It is notable that, notwithstanding yesterday’s retreat, outright prices are holding up resiliently, with Brent settling above the $70/bbl mark for the fifth consecutive trading session. Attacks on Russian infrastructure, the halt of oil exports to Hungary and Slovakia on the southern leg of the Friendship pipeline, the utter uncertainty surrounding the US plan regarding Iran, the fate of the Strait of Hormuz, and the resultant anxiety over a possible distillate shortage are the main reasons. This morning’s pop higher was helped by drawdowns in US product inventories as reported by the API, although crude stocks recorded a massive build.

Yet the sudden weakness in the Brent and WTI structure, along with the sell-off in Brent CFDs, serves as a timely reminder that once the Iranian crisis abates without major damage to production and transport, expectations of a supply deficit will no longer be justified. For this reason, tomorrow’s talks between the US and Iran appear to be make-or-break. If no consensus is reached on Iran’s nuclear programme, and if the US opts to launch a military operation against the Iranian regime, for which the President made a case in last night’s State of the Union speech, a brief spike towards $80/bbl cannot be ruled out, before oil course corrects.

What Iran means for the perceived and actual oil balance, is as tariffs for the US and the global economy. The 10% global punitive duties, introduced in response to last week’s Supreme Court decision, came into effect yesterday, and whether they will be increased to 15% is anything but clear. The lack of transparency understandably keeps investors nervous, yet Tuesday’s stock market rout was followed by a semi-decent bounce, chiefly because faith in the tech sector was reasserted. In his State of the Union address, the US President remained defiant on tariffs, which, judging by the stock market reaction and as discussed below, will do nothing to brighten sentiment.

Reverting to Norm or Further Deviation?

Last Friday’s US Supreme Court decision did not entirely come out of the blue, although the outrage from the administration suggested that the disobedient Justices had explicitly exceeded their mandate and should, at a minimum, be hanged, drawn, and quartered. It is worth recalling that, during the oral arguments last November, the highest court in the US appeared sceptical of the president’s tariff authority under the International Emergency Economic Powers Act (IEEPA). Yet the ruling that the administration had illegally used executive power to implement these measures came as something of a surprise, pleasant or otherwise, depending on one’s allegiance, and raised several questions that will not be answered imminently.

The first is whether the narrative of national security and emergencies will persist and whether coercive policymaking will continue. The highest court in the land deemed it illegal to impose blank import duties based on national security or emergency grounds. It will be intriguing to see whether there will be a political backlash against the US administration. After all, most of its policies have been carried out in the name of emergency and security, be it ICE deployments in Democratic-led cities, the planned occupation of Greenland, or the capture of the former Venezuelan president, not to mention climate-change denial justified by citing energy security and emergency. Of course, there is no legal basis to rebuke the government’s political views and actions, but those who have been living by Trump’s sword in the administration or in Congress might not be willing to die by Trump’s sword.

Then there is the question of refunds. A usually well-informed political podcast alleges that, well before the Supreme Court’s ruling, there was an active market in tariff refunds, with those close to the government offering 10 cents on the dollar for reimbursements. At stake is around $175 billion, the amount the US Treasury has so far collected. President Trump correctly pointed out that repaying duties already accumulated will be a messy and protracted process. The Court left it to the lower courts to decide the issue. One salient question is whether companies that passed on the extra costs of tariffs to consumers will be eligible to seek remedies.

Thirdly, the reaction of trading partners is also uncertain at this stage. It is not clear whether already agreed trade deals will be honoured. India, for one, decided to reschedule negotiations in light of the Supreme Court’s decision; the talks had been expected to finalise the trade agreement struck earlier this month. The EU is also delaying the ratification of its own trade deal. The UK floated the idea of retaliation if diverging from the original agreement, and Japan warned against imposing higher rates on its exports. The resultant and seemingly capricious new global 10% or 15% tariff (currently it is the lower rate) under Section 112 of the US Trade Act, which is valid for 150 days without congressional approval, overwhelmingly benefits adversaries such as China and Brazil while disproportionately punishing traditional US trading partners, the Financial Times points out, citing analysis from the Global Trade Alert, an independent trade monitoring body.

It is impossible to foresee what the future holds, but it is useful to compare two extremes: the market reaction immediately after the “Liberation Day” announcement on April 2, 2025, and the reaction following the Supreme Court decision last Friday. Equities plunged last year and rallied last week (but plummeted after the announcement of the new 10%-15% punitive measures). The Efficient Market Hypothesis holds that asset prices instantly reflect all available information, and the two strikingly different market reactions clearly lay bare the adverse economic impact of import duties. As rudimentary as this approach is, it suggests that dialling back tariffs and accepting the SCOTUS ruling would go a long way toward mitigating inflationary pressures and thereby economically justify additional long-coveted interest-rate cuts.

Reverting to the norm would calm investors’ nerves, eliminate unpredictability, and greatly aid the Republicans ahead of the midterm elections in November. As reasonable as this sounds, the opposite appears more plausible. The train, which carries the US President on his ego trip, is accelerating, and it is too late to get off. So, what’s now? Any behavioural scientist worth her salt would tell you that “any choice, no matter how bizarre, can be rationalised by constructing a set of assumptions about preferences and constraints under which some odd behaviour is found to be an optimising solution.” (This quote is borrowed from the book The Winner’s Curse.) Since President Trump is no stranger to volatile behaviour or inconsistent decision-making, and given the domestic headwinds precipitated by the Court’s decision declaring tariffs unlawful, along with his reluctance to accept it, his foreign policy may become more erratic in the name of national security, with potentially inauspicious consequences for Iran or Ukraine. Wild swings across asset classes, therefore, appear probable. A reasonable way to take advantage of this elevated impulsiveness is to acquire the right both to buy and to sell one’s preferred financial instruments in months to come at pre-agreed prices.

Overnight Pricing

25 Feb 2026