Words Are The Biggest Market Movers

It will be welcome relief, or at least a change of scenery, to begin a day without having to consider whatever latest Trumpism banners the morning’s headlines. Alas, that day is a long way off and yielding to the power of the new President’s words is unavoidable for reporting and more importantly, market movements. The extension of his campaign stump speech into the midst of Davos delegates again affects the progress of all investment suites. He had offered, in a Fox interview that there had been conversations with China and while tariffs are all set to be used, it would be preferable to reach accord, which was not countered in his address to the World Economic Forum. This then sent the S&P to another high and China’s bourses surge. However, this seemingly softer approach to tariffs was flipped as the President turned a scornful gaze toward the US’s closest allies in Canada and Europe bemoaning the trade deficits and threatened action.

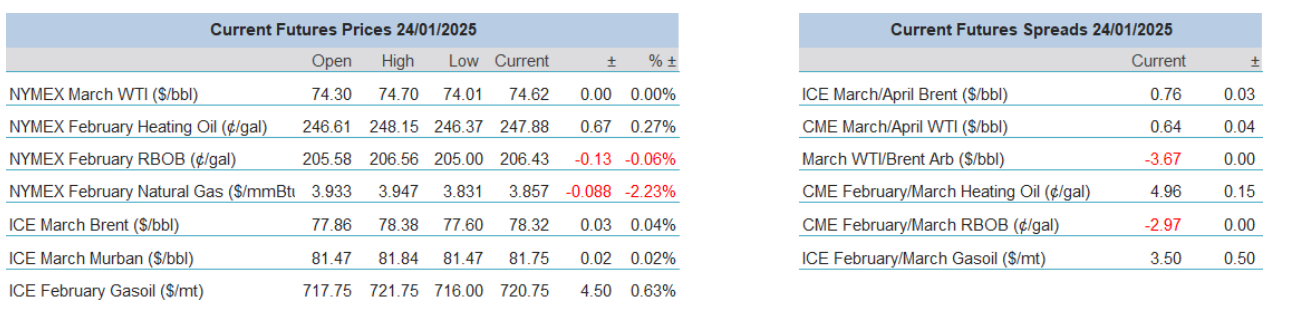

Oil is not spared President Trump’s paradoxical approach. Championing the oil industry of the US is no great surprise as he urges all hands to the pump. However, gushing oil into a softish 2025 market is not what the CEO’s of oil companies are about, it is a matter of profit and shareholder value. Therefore, when he then proceeded to turn his feigned ire on Saudi and OPEC insisting that they pump more oil to bring prices down, one could almost hear the global sighs of consternation emanating from the boardrooms of big oil. Such perception found substance in oil futures as Crude prices slumped 1% and importantly fell below the 200-day moving average which had seen much fanfare when broken above earlier this month.

Markets are in no mood to heed the news such as the rate rise by the BoJ which sees interest rates at their highest for nearly two decades. Or that Crude stocks, as reported in the EIA Inventory Report, in the United States are at the lowest level for nearly three years and inventory at Cushing, the main storage hub, have fallen to just over 20 million barrels and are close to ‘bottoming’. The words of the new President are much more important than market fundamentals at present and likely to stay so for some time.

Tariffs are important, but short-term oil supply is short

As is the case in most circumstance of tariff and sanction there are always many more questions than answers and paths to unforeseen consequence often open. It is odd in a world that cries out for stimulus in some instances of economic basket cases such as Europe and the need to stop China becoming one, the stimuli we actually receive is that of agitation to current geopolitical strife. The tariffs bandied around in Washington in whatever size and guise are currently holding oil in its thrall and the threat to international trade is being very much reflected in the state of oil prices. Attraction to the oil space due to recent sanctions and cold weather is being dulled by future oil trading freedom and while the cold weather will eventually abate further as the year progresses, it is, however, way too early to believe that the bite of fresh sanctions on Russia will not continue to leave tooth marks. Wednesday, on his Truth Social, President Trump prepared his negotiating table with President Putin by threatening higher levels of taxes, tariffs and sanctions on Russia if no Ukraine talks were forthcoming and promised that other countries would join the US lead.

Much is being made of how Russia’s skill in circumventing sanctions will once again be deployed and it will only be a matter of time until the ‘dark fleet’ is either renamed, reflagged or possibly even replaced. The Russian state owned Sovcomflot and other shipping capability has been much practised in this endeavour and there can be little doubt that such actions are right now underway. Many vessels are registered in complicit nations such as Cook Islands, Hong Kong, Gabon, Vietnam, UAE among others and turning ownership is probably only a matter of time. According to a recent insight in Energy Intelligence, ships and their ability to morph identity see relationships with associative trading companies registered in Dubai that also show remarkable phoenix-like abilities as they close and reopen renamed. Disguising ships, transactions and payment facilitation has become second nature then and largely overlooked by the previous US administration when it mattered, not at its end, all in the name of oil price expediency.

Whatever the motivations of President Biden, his tightening of Russian oil transportation scrutiny might well have been ducked and avoided by the wily old boxing Russian Bear. However, this assumption precludes a certain Donald Trump who is held in something of global enigmatic awe, even in China. There are very few countries who are willing to upset the new US administration, and with tariffs and diplomatic threats as much a favourite as McDonald’s hamburgers and fries, even nose-thumbing Russian users of oil such as India and China are frankly frightened of getting on the wrong side of US scorn so early on in a new presidency. This is why tankers are idling off the coast of places such as the refinery intensive area of Shandong in China until the largest importer of oil figures a workaround or clarity of how Sino/US relations unfold.

It would appear the situation is more pressing in India, which does not enjoy the massive storage capacity boasted by its Asian competitor. Recent history has seen the biggest country of the sub-continent take full advantage of discounted Russia supplies. This can be highlighted by how, before the new sanctions, India’s intake of Crude from Russia made up a remarkable 40% of its imports which is four-times higher than it was post-pandemic. It has been assumed Indian refiners would await the quick-footed Russian re-jigging of ownership, and despite recent utterances that there remained confidence in supply it now appears as if they are biting the bullet and going to the spot market for differing grades. According to Bloomberg, India is deploying a metaphorical vacuum cleaner approach to availability, but what is telling is how its refiners are now entering negotiations into longer-term deals with Middle East suppliers making a mockery of its recent stance on expectations in Russian Oil. India does not want to upset the US at present, it needs replacement crude to the tune of 1.8mbpd and getting caught in protracted sea-faring contractual hold ups does not fuel its growing economy.

Russia will eventually find ways to regain markets. There is also massive spare capacity in OPEC and the Americas, which given time have the potential to cover the hole currently being left by the absence of Russian oils. Yet, ‘given time’ is important here. Receiving oil from term deals that start to take effect in the second quarter are no use to customers that require supply in the here and now. The reason for the start of year rally is still apposite, sanction busting is also made harder by the intriguing inhabitant of the White House and for any international relationship that might be formed. The collar of tariffs and what might be is more relevant to the future price of oil rather than now, the scamper for alternative crudes across the globe may only be short-term, but it is nowhere near reasonable to dismiss it.

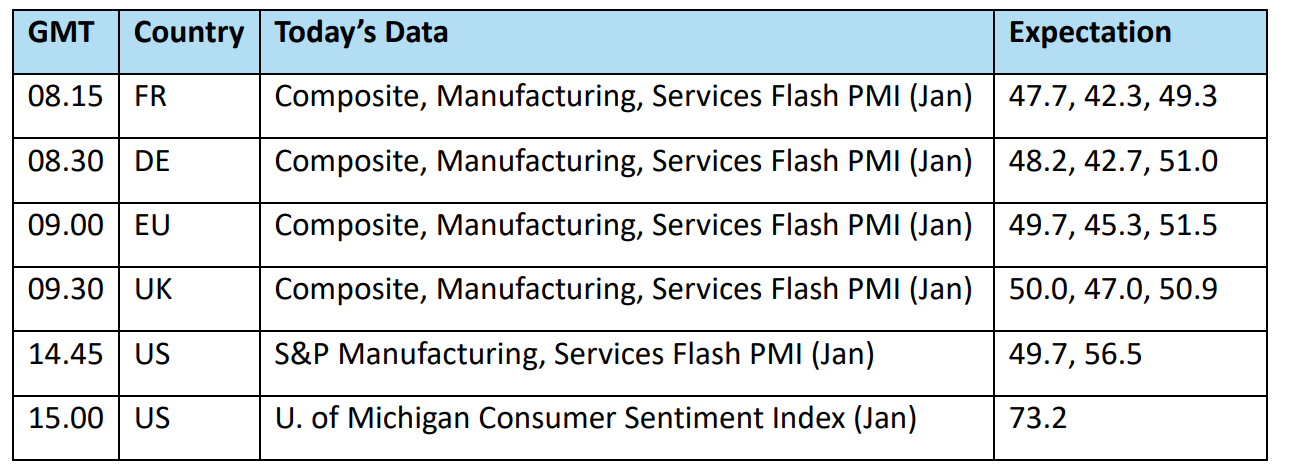

Overnight Pricing

24 Jan 2025