Words are as Loud as Action

Recent trends prevailed, expectations were fulfilled and as a result, investors remained upbeat on the US and concerned about Europe. Even though US initial jobless claims retreated more than anticipated the country’s growth remains, if not robust, then stable and solid. Its economy expanded less than hoped in 4Q 2024 but at 2.3% the Biden administration handed over a country to Donald Trump, which is full of confidence. Hence the stubbornness and disobedience of the Fed, which decided to listen to data and not to the new President and kept rates unchanged after three consecutive cuts. In its view inflation is still ‘somewhat elevated’ and the neutral level is slightly lower.

Conversely, the European Central Bank warned of headwinds. The German economy contracted at the end of last year and the Eurozone stagnated. No wonder then that the central bank stuck to the script and lowered borrowing costs by 0.25% to 2.75%. Its president underlined the fragile consumer confidence and contraction in the manufacturing sector. The interest rate gap widened. It is supportive of the dollar, notwithstanding yesterday’s slight weakness, and makes oil more expensive outside the US.

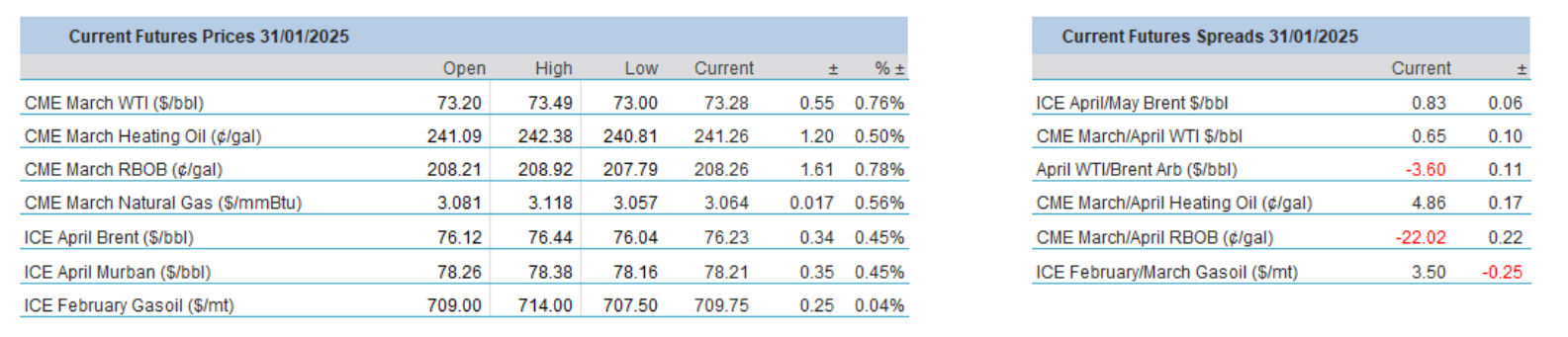

The greenback, however, is only one of the abundance of factors that impact the price of oil. Pre-weekend anxiety level is on the rise as the traffic deadline, discussed below, looms large. Although the President said oil might not be included WTI is strong. In Monday’s OPEC+ get-together, the group’s approach towards Donald Trump will likely be unmasked – another salient element in shaping the mood. Once again, the high level of ambiguity makes it difficult to confidently predict the next $15/bbl move. What is undeniable is that since the inauguration of Donald Trump, oil prices retraced $4/bbl although the latest round of Biden sanctions remained in effect against Russia. It insinuates that something significant must happen on the supply side of the oil equation to see a protracted break over $80/bbl.

It will Backfire

Since January 20 every day seemingly brings a deadline as the new US administration attempts to implement its political and economic agenda. Amongst the many contentious and divisive proposals one of the most pivotal ones is tariff, ‘the most beautiful word in the dictionary’. Tomorrow, February 1, is the day of reckoning for the most vital trading partners of the US - China, Canada and Mexico. The White House said on Tuesday that the President still intends to deliver on his promise to impose punitive measures on imports from the three countries. If he goes ahead, the extent of these policies will have a tangible impact on every asset class, including equities, the dollar exchange rate and oil. The original campaign, however incoherent it was, pledged to hit China with as much as 60% tariffs and the US neighbours with 25%. What is not entirely clear at this stage is whether these threats will be implemented gradually, or at all in the case of Mexico and Canada, as hinted by the incoming Commerce Secretary, Howard Lutnick. What textbooks on macroeconomics and the first Trump term tell us is that tariffs, in their proposed form, are more of an ideological tool with measurable inauspicious consequences.

Before the principle of comparative advantage became prevalent in the 19th century tariffs were a vital source of revenue for the government. In modern times, however, tariffs are used for one of three reasons: on national security grounds, protecting domestic suppliers and creating jobs or supporting infant industries, such as high-tech. It appears that in its own peculiar ways, the Trump administration intends to use import tariffs, a form of excise tax, to increase government revenue, protect domestic industries, reduce trade deficit, create jobs by supporting manufacturers and gain leverage over its trading partners. This view is admittedly open to debate, but it appears, it is as much a political as an economic instrument.

The impact of import tariffs is dubious, on theoretical as well as practical levels. When implementing import tariffs, the price received by domestic producers and paid by domestic consumers increases. The domestic price of the commodity will ascend above the world price. Any price increase will have a tangible effect both on domestic supply and demand: a positive one on the former and the opposite on the latter. Because of the rise in domestic price producers gain, consumers lose, and the government realizes additional revenues. However, the collective gains of producers and the government will be exceeded by the losses consumers suffer resulting in a net reduction in total surplus. Unnecessarily constraining free trade leads to inefficiencies.

The argument to employ import tariffs on national security grounds is sound as the country’s political or economic fabric could be in jeopardy. Domestic suppliers will also be protected but it comes at a cost, which usually outweighs the economic benefits as outlined above – domestic price rise reduces demand. Job creation is an indisputable impact of tariffs. It occurs in the import-competing sector. It is, nonetheless, more than countered by the job losses in industries that use imported inputs and now face higher input costs.

The first Trump administration introduced a 25% tariff on steel imports, which particularly hurt its northern neighbour, Canada. Mr Trump was adamant that exporters and not American consumers will pay these tariffs. Market data deviates from this argument. US steel prices registered a sharp jump as the punitive measure was implemented whilst world prices stagnated. Re-alignment only began when tariffs were removed after a new trade agreement with Canada and Mexico was signed. US steel companies were the main beneficiaries of the measure and by re-opening production facilities jobs were created. Steel users, on the other hand, were forced to close plants and lay off the workforce. Part of the tariffs was passed on to their consumers in the form of higher prices. Curiously, steel workers’ wages did not increase more than those of workers in other parts of the economy.

Economic wisdom and experience suggest that the net impact of tariffs is negative. The incumbent trade policy is designed to exert political pressure on US trading partners, rather than bring prosperity to US consumers. Whether it helps to reduce the trade deficit is also dubious. The cynic would say that tariffs also lay bare the political influence of import-competing producers.

Those who believe that wide-ranging tariffs carry no net benefit can do nothing but conclude that the consequential inflationary pressure, exacerbated by tax cuts and deregulation, will result in a change of sentiment in the stock market, the ultimate arbiter of the performance of any government. As implementing tariffs will entail reciprocal measures it is not just the US markets that will come under strain, but the global economy will follow suit. It is imperative to closely follow the Trump administration’s practical moves on tariffs since the reverberations will be far-reaching.

Overnight Pricing

31 Jan 2025