Worrying Escalation is Met with Admirable Calmness

Overnight developments strongly imply that, despite hopes and prevailing narratives, this conflict will not end any time soon. In fact, the escalation is a genuine cause for concern. Iran played the role of the bad actor in the latest twist of this Middle East saga when it downed an American Apache helicopter over the Strait. The response was swift, as the US military struck Iranian targets, leading to an intensifying exchange of fire. The Islamic Republic reportedly hit the US Navy’s Fifth Fleet in Bahrain and an air base in Jordan, and warned Gulf states of further retaliation if they allow the US and Israel to use their territory to launch attacks against Iran.

The region, home to more than 20 mbpd of oil production, remains the most troubling geopolitical hotspot. Yet what we see this morning is that the initial rally triggered by the flare up in tensions is already fizzling out, and oil prices are slightly in the red at the time of writing. The optimism is praiseworthy, especially after last night’s API report, which aligned with the broader trend of global stock draws. Chinese crude oil imports, which dropped by 3.8 mbpd in May compared with last year’s average, are an undeniable mitigating factor, and so is the erratic but very real transit through the Strait.

Nonetheless, it is difficult to reconcile the current lack of anxiety with the perpetual conflict engulfing the world’s most pivotal oil producing region. On the other hand, sentiment is a powerful driving force, and resisting it can only end in considerable disappointment.

Market Ignores Short-Term Deterioration

Simply put, there are two schools of thought regarding the impact of the ongoing crisis on the oil balance. One, apparently the more dominant view, is in spectacular disagreement with the other.

Advocates of the first camp are confident that global oil supply will not fall into an unmanageable deficit relative to demand, and that any shortage that may emerge in the weeks or months ahead can be handled with relative ease. How? By drawing on existing oil inventories to ensure a steady flow of supply. There is little doubt that this group is betting on an imminent resumption of oil traffic through the Strait of Hormuz. This must be the primary rationale behind the considerable decline in oil prices, from $108 less than a month ago to $91.50 at last night's settlement. Put differently, market participants constitute the majority of this camp.

In the opposite corner are those who believe that the now-infamous chokepoint will remain closed for the foreseeable future. Supply, much of which normally passes through it, will remain constrained, and global as well as OECD oil inventories will fall to, or even below, critical operational levels. Judging by its updated Short-Term Energy Outlook, the EIA belongs to this category. And the numbers, as discussed below, are frankly worrying.

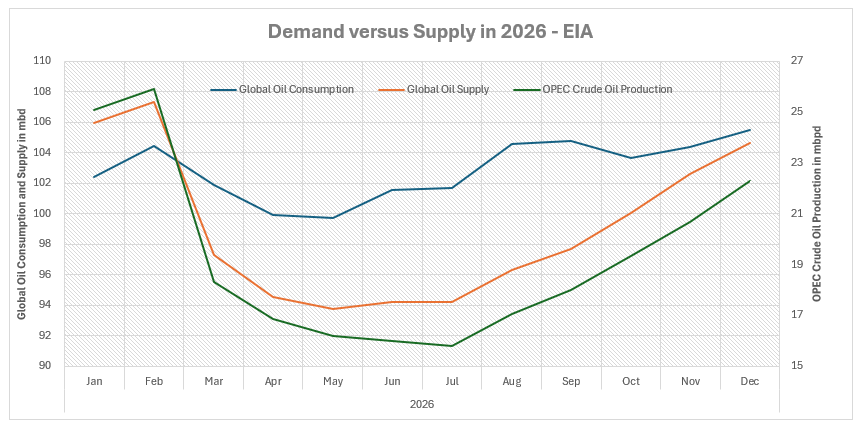

The report begins with a key disclosure: namely, the assumption that the Strait of Hormuz will remain closed in the near term and that oil traffic will take several months to return to pre-conflict levels. Although oil prices fell in May, inventories are expected to continue declining because of the anticipated prolonged closure of the Strait. As a result, Brent prices are projected to average $105/bbl in June and July. The chart below tells the story.

The left axis shows global oil consumption and oil supply. It is evident that while both have trended lower since February, supply has suffered a much more severe blow than the higher oil prices have inflicted on demand. It is also clear that OPEC production, shown on the right axis, is entirely responsible for the sharp combined decline. Naturally, once recovery begins, supply should rebound much faster than demand.

The million-dollar question is when that recovery will occur. Given the capricious nature of geopolitics in 2026, any answer is little more than an educated guess rather than the product of formulas or calculations. What is evident is that forecasts will continue to be revised without hesitation until the waterway reopens, just as they were in the latest report.

The EIA has lowered its estimate of global crude oil production for the third and fourth quarters by 3.17 mbpd compared with its May outlook, while slightly increasing its global oil demand forecast by 710,000 bpd. Consequently, global inventories are now projected to decline by 4.84 mbpd in the second half of the year, compared with a decline of 1.2 mbpd in the May projection.

OECD industrial stockpiles are also expected to draw down more rapidly. They are forecast to stand at 2.359 billion barrels by the end of the third quarter and 2.269 billion barrels by year-end. The latter is a particularly alarming figure, as it implies only 50 days of forward cover.

If one assigns any credibility to the EIA's oil balance, and admittedly, it comes with several significant caveats, one must wonder what catalyst, if there is any, is still missing that would propel oil prices well above $100/bbl once again.

Overnight Pricing

10 Jun 2026