A new beginning?

With less than two weeks to go before the US runs out of cash, optimism is building that both sides of Congress will come together to prevent the unthinkable. Policymakers in Washington hinted yesterday that a bill to raise the US debt ceiling may be put to a vote next week. This encouraging development spurred hopes that the current deadlock will follow the same outcome of previous standoffs, namely that there will ultimately be some kind of agreement.

As traders kept their fingers crossed for a potential US debt ceiling deal, hawkish signals from Fed policymakers put a downer on market sentiment. The message was that inflationary pressures are not cooling fast enough to warrant a pause in the current rate-tightening cycle. In other words, the door remains very much open to another rate increase in June. Meanwhile, data from the US labour department showed the number of Americans filing new claims for jobless benefits fell more than expected last week.

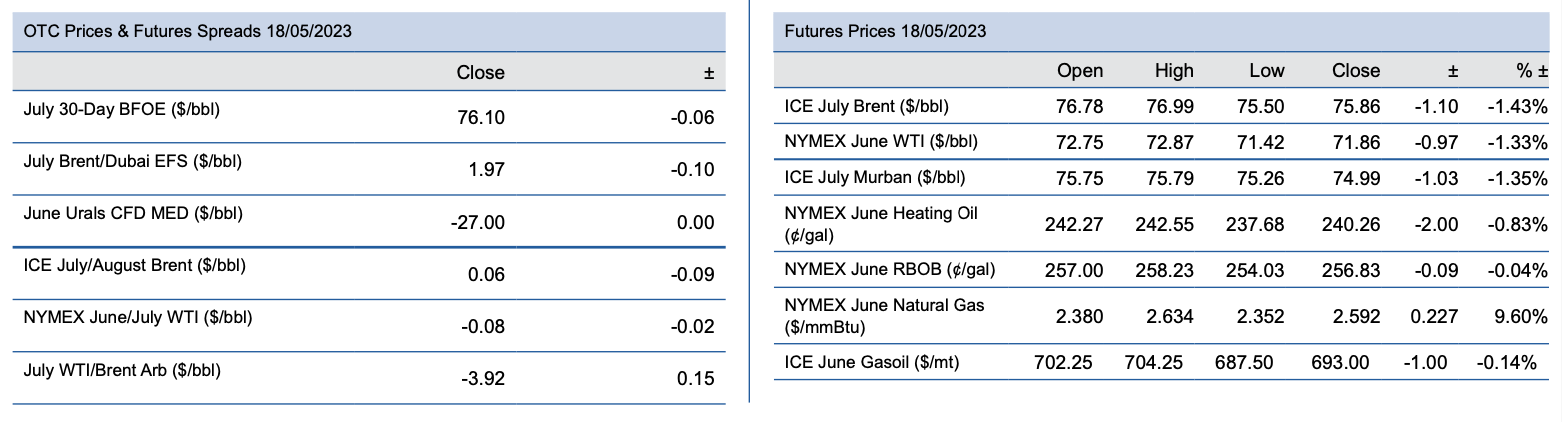

The combination of hawkish Fed comments and strong US data gave the dollar a boost. The US currency gained 0.6% against a basket of major currencies on Thursday and in doing so topped a two-month high. The stronger greenback sealed a negative session for the energy complex. Nevertheless, the Brent and WTI crude oil markers are still on track for their first weekly advance in five, which in turn may signal the start of a sustained price recovery.

Flatlining

US shale output to hit a record high next month. US shale supply to increase in June by the smallest margin so far this year. Two headlines, both accurate but with different connotations. The latest EIA drilling report showed US tight oil supply is expected to continue expanding, albeit at a slower clip. Production from the seven biggest US shale basins is forecast to rise from 9.29 mbpd in May to an all-time high of 9.33 mbpd in June. Yet the 41,000-bpd monthly gain represents the smallest increase seen so far this year. What’s more, back in January, the EIA forecast that tight oil supply would top the 9.3 mbpd level in February. The fact that it is now only expected to be reached next month represents a downward revision from previous forecasts.

And there is more reason for concern. The EIA’s drilling report showed the productivity of wells is flatlining as drillers exhaust prime acreage. New-well production per rig across the US shale patch was static in April. All the while, the report showed that the number of drilling rigs continued to decline through April, with oil sites dropping to a seven-month low of 680. No surprise, then, that well completions outstripped freshly drilled wells for a fourth consecutive month. The upshot is that the number of drilled but uncompleted wells once again dipped. These so-called DUCs fell to a nine-year low of 4,863 in April.

The pullback in drilling activity is echoed by Baker Hughes. Latest data from the oil services provider showed the total US oil rig count has declined by 5.6% in the year-to-date to 586, the lowest since June. While this is slightly up on the year-ago level, it is a far cry from the nearly 900 rigs seen in early 2019 at the zenith of the US shale boom. As drilling hits a plateau, you can be sure that shale oil supply growth will decelerate with increasing vigour.

Red flags for the US shale sector and not only seen in the EIA’s latest drilling report. Earlier this week, the FT carried a report claiming that the lull in shale drilling is forcing some operators to auction off equipment due to a lack of demand. This oversupply of equipment marks a stark change to the shortages in the immediate aftermath of the pandemic. All the while, the anticipated wave of mergers and acquisitions coming to the US shale patch has failed to materialize. Expectations for a flurry of deal-making were spurred by the windfall from last year’s record cash flows. Yet US oil and gas dealmaking fell to a two-year low in the first quarter, according to energy analytics firm Enverus.

On a brighter note, cost inflation across is moderating after running hot for the last two years. Inflation was previously running at 10% to 15% annually but the days of double-digit price increases are a thing of the past. Even so, this alone is unlikely to reinvigorate drilling levels. Accordingly, US shale output levels could flatline a lot sooner than expected. This week, the EIA revealed US crude production dipped to 12.2 mbpd – a level that has remained more-or-less constant since the end of last year.

19 May 2023