All hail China!

Weak, sluggish and disappointing. That’s what pessimists would have you believe with regard to the current economic outlook. Concerns over the health of the global economy and oil demand prospects have been front and centre of the oil markets of late. We’ve long argued that the bearish price action is unjustified, a sentiment echoed by the IEA in its latest monthly oil report released yesterday. The Paris-based agency expects global oil demand will increase by 221,000 bpd in 2023 to average 102 mbpd, 180,0000 bpd more than its previous estimate. Moreover, global oil consumption is expected to hit an all-time high of 103 mbpd in August.

The improving demand growth outlook hinges on – you guessed it – China. The Asian behemoth is flying the flag for the demand side of the oil equation, with the country’s consumption setting a record high of 16 mbpd in March. China’s demand recovery continues to surpass expectations, so much so that the IEA now assumes annual growth of 1.3 mbpd in 2023, compared to April’s projection of 1.1 mbpd and March’s estimate of 900,000 bpd. Given that China’s rebound is proving stronger than previously anticipated, expectations are running high that gains will gather pace during the rest of the year. In short, the IEA argues that the favourable outlook for China’s oil consumption should dispel any worries about a downward shift in oil demand growth.

On the supply front, the key takeaway was the continued resilience displayed by Russian oil supply. In April, Russian oil exports reached a post-invasion high of 8.3 mbpd, according to the IEA. This compares to an average 7.7 mbpd in 2022 and 7.5 mbpd in 2021. Such lofty shipments will pour fresh doubts over whether Moscow has delivered the pledged 500,000 bpd supply cut in full. Sure enough, the IEA reckons Russian crude oil output was steady at 9.6 mbpd, implying the OPEC+ heavyweight must still cut a further 300,000 bpd to bring itself into line.

Despite stubbornly high Russian production, output from the OPEC+ bloc this month is expected to take a dive on the back of voluntary production cuts. From April through December, OPEC+ oil production is set to drop by 850,000 bpd, as per the IEA’s forecasts. All the while, flows from outside the producer group are predicted to rise by 710,000 bpd. Accordingly, the IEA upped its call on OPEC crude in 2H23 by 100,000 bpd to 30.35 mbpd. The cartel’s production stood just below the 30 mbpd threshold in April and is set to fall further this month as new cuts take effect.

The end result is tightening market balances. The 1Q23 global supply and demand balance shows an 870,000 bpd implied stock increase – the fourth consecutive quarterly stock build. Now, though, substantial stock draws from the current quarter through the end of this year are pencilled in. IEA balances show demand will eclipse supply by almost 2 mbpd in the second half of the year. Simply put, a supply crunch is looming on the horizon. And you can be sure that oil prices will rally once the markets wake up to this fact.

Risk off

The IEA’s bullish forecasts were largely ignored yesterday as economic updates from China and the US undershot expectations. Chinese retail sales and industrial production did not show the pick-up that was expected in April. Meanwhile, US consumer spending was weaker than forecast last month. Retail sales rose by 0.4% in April, missing forecasts of a 0.8% rise, after a 0.7% drop in March. Elsewhere, a gauge of German investor morale fell by more than expected this month, suggesting that Europe’s largest economy could fall into recession this year.

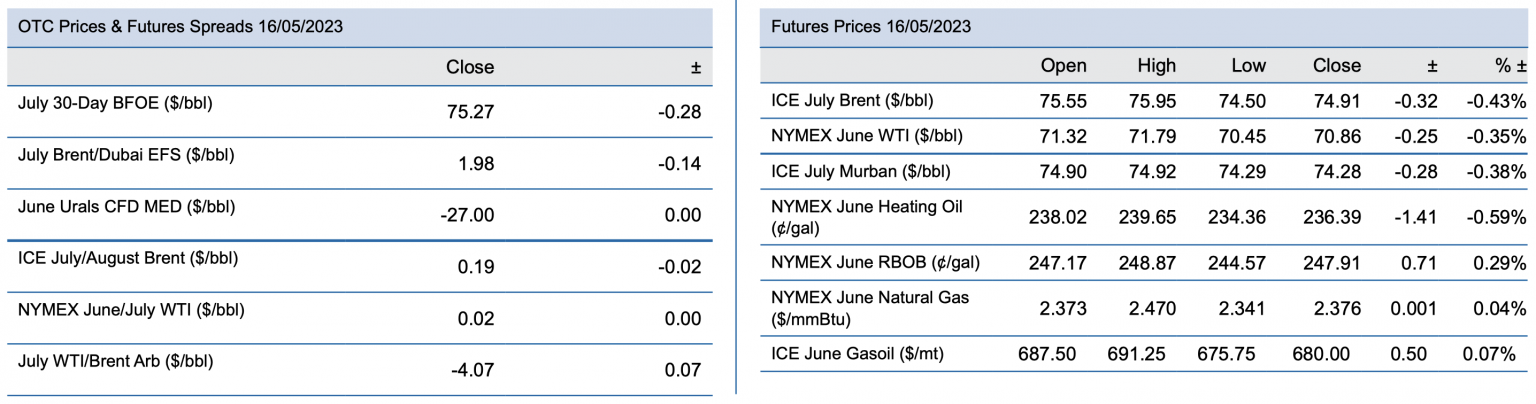

Amid this batch of underwhelming macro updates were ongoing US debt ceiling concerns. Negotiations aimed at raising the debt ceiling are continuing but as of yet have proved fruitless. With only 15 days weeks before June 1, when the US is expected to exhaust its cash on hand, anxiety over a potential default is only going to intensify. Staying in the US, data from the API released overnight showed crude stocks rose by 3.6 million bbls last week. Gasoline and distillate fuel inventories fell by 2.5 million bbls and 886,000 bbls, respectively.

17 May 2023