September 2023: Digital Assets Monthly Roundup

September 2023: Digital Assets Monthly Roundup

- Market for BTC and ETH remained relatively stable, dropping on news of FTX liquidations and Fed hawkishness before rallying to close above $27k.

- SEC Chair Gensler’s approach to digital asset regulation is critiqued in congress, with the threat of subpoena levelled.

- Volumes and transactions are growing on the peripheries, as Chainlink rallies off connectivity into institutions and crypto-natives speculate on each other’s value via Friend.tech.

For the world of cryptoassets September has felt like a month of quiet and growing confidence amongst wider noise. On the surface, one could easily take the view that the space is still in a malaise, hamstrung by a high rate environment and the reopening of last cycle’s wounds with the start of Sam Bankman-Fried's trial against the US Department of Justice. However, if you move past the noise and look beneath the surface, there is interest and momentum brewing. Perhaps even early signs of the next bull market beginning to sprout.

Following on from the sell-off at August close, the market continued to tumble through the start of September. Bitcoin hit the sub $25k low that we last touched in June and Ether fared even worse, hitting a 6-month low of $1533 on 11th September*. This drop supposedly came off the back of news that FTX was seeking permission to liquidate billions in holdings of BTC, ETH, SOL and more, for which they received approval just days later. As the month rolled on, negative news continued to garner the most attention toward crypto. Gary Gensler visited Capitol Hill twice, and in his most recent address there stated that tokenised Pokémon cards, amongst other cryptoassets, may be considered securities... In Gensler's opening statement to Congress, he reaffirmed his view that the cryptoasset space is largely uncompliant, and that businesses and protocols launching tokens have every chance to register with the SEC but choose not to.

What followed was some pretty severe scrutiny from Congress on both sides of the aisle. Critiques levelled included the ineffectiveness of Gensler’s regulation by enforcement approach, as well as the validity of him delaying approval for a BTC spot ETF. Matters escalated to such a level that chair McHenry threatened the SEC with a subpoena if Chair Gensler continues to ignore Congress' status as an equal branch of government. While Gensler's approach towards regulation of capital markets and digital assets has been a defining feature of the past two years, with presidential elections approaching next year it remains to be seen whether we shift to a more crypto-friendly SEC.

Despite the general negativity surrounding crypto from the media, the remainder of the month saw both BTC and ETH reverse their trajectories to close off the month in the black; with BTC rallying over 8.5% from the monthly low on the 11th. Despite holding rates at 5.25-5.50 for the time being, the Federal reserve's forward signaling of further hikes on the 21st led Bitcoin to tumble again from the $27k support level, and Ether to fall from $1630 to $1565, before rallying back to reclaim both levels before months close*. While the options market for these assets had been growing steadily in terms of volumes across the quarter, September saw a retrace back to below $1b worth of volume from around $1.5b just the month prior for Bitcoin**. Nonetheless, it’s worth noting, that while monthly exchange spot volumes are down from $4.1T at their peak to just $97.27B now (the second lowest month since September 2016), Bitcoin options open interest has only fallen from $13.8b at its peak to $10b at September close **. Whilst the market for options is significantly smaller than spot, it's comparative resiliency may indicate that it’s becoming an increasingly important influence on the underlying crypto markets, and not just another tool to speculate or hedge one's exposure

Though majors do lead the way generally for cryptoassets, looking only at the BTC and ETH graphs paints a rather dull picture of the space, one that is not representative of the various thriving niches and re-emerging alts in my opinion. For instance, LINK had a mammoth month in September, rallying over 40% from ~$5.7 at the start of month to ~$8.3 at close*. ‘Why’ you may ask? Well, Chainlink's Cross Chain Interoperability Protocol (CCIP), which went live earlier this summer, has continued to see adoption and participation from Crypto natives as well as TradFi institutions like: Swift, BNY Mellon, Citigroup, and BNP Paribas. CCIP aims to become the "TCP/IP of Finance" by creating a standard and secure communication system between blockchains to do away with arguably riskier connectivity vehicles like bridges, which have seen numerous large exploits in the past few years. Infrastructure like CCIP serves a valuable purpose by connecting the private/public blockchain gap, allowing clients of the banks to get access to digital asset ecosystems in a more secure manner as well as allowing tokenised Real World Assets (RWA's) from Banks to move onto public blockchains and into secondary markets.

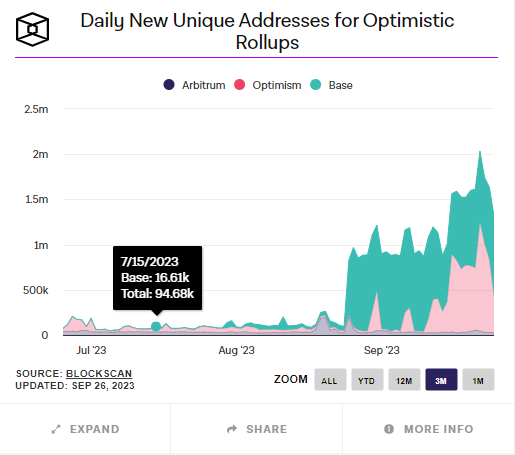

Over the past month, it's been interesting to see that Ethereum has come under some scrutiny for arguably not delivering on its promises of growth, decentralisation and deflationary monetary qualities after the move to Proof-of-Stake last September. JP Morgan recently highlighted in a report that daily transactions, daily active addresses, and total value locked on Ethereum main net, are all down since the upgrade. While one could reference the still bearish conditions to justify this drop, I think there is a better argument to be made. Ethereum is operating as intended: that users are leveraging cheaper and faster compute by migrating to L2's, where there are emerging ecosystems of new DApps that are driving real user growth such as with Friend.tech on BASE (the Coinbase incubated L2). In the last 30 days alone, Friend.Tech, which allows users to buy and sell 'keys' (like NFTs) of friends and influencers in the crypto space, has seen 254.62k unique active wallets interact with their code and over $177.7M in transaction volume, all in a bear market^... Whilst the majors undoubtedly determine wider market moves, activity on the peripheries can often indicate a shift that takes longer to reach the core of the market. As activity continues to flourish on L2s, there is much cause for Optimism...

As always please send any feedback, suggestions, or comments to the Team mailbox.

Best Oliver Wink, on behalf of the Digital Assets team.

*Data sourced from Bloomberg

**Data sourced from The Block

^Data sourced from DApp radar